FortisPay Review

05

May 2026

No Comments

FortisPay Review

FortisPay is a payment technology company that has traveled a meaningful distance from its origins as a traditional merchant services provider. Founded in 1998 under the name Cambridge Payment Systems and headquartered in Novi, Michigan, the company rebranded as Fortis Payment Systems before settling on the FortisPay identity it operates under today. Under the leadership of CEO Greg Cohen, Fortis has deliberately repositioned itself away from generalist credit card processing toward a more focused mission: delivering embedded payments for software platforms, ISVs, ERP systems, and mid-market to enterprise businesses. Lets read more about FortisPay Review.

That strategic pivot has been accelerated through a series of acquisitions, including Blue Dog Business Services in 2020, Swype at Work and EpicPay in 2021, Change Merchant Solutions in 2021, and Payment Logistics in 2022. Each acquisition has added vertical-specific expertise, technology capabilities, or geographic reach to the Fortis platform. The company now operates as a registered ISO of Wells Fargo Bank and processes billions of dollars annually across industries including healthcare, hospitality, retail, construction, manufacturing, and professional services.

This review takes a grounded, honest look at what FortisPay actually delivers, covering its technology, verticals, developer tools, pricing, contract terms, and the patterns in merchant feedback that are important context for anyone evaluating the platform.

Company Background and Market Position | FortisPay Review

FortisPay’s evolution over more than two decades reflects a company that has repeatedly refined its identity in response to market conditions and strategic opportunity. The Cambridge Payment Systems origins placed the company in the traditional merchant acquiring space, serving small and medium-sized businesses through standard processing relationships. The subsequent rebrand to Fortis and the accelerated acquisition strategy that followed reflects a deliberate shift toward embedded payments and software platform partnerships.

The acquisition of Payment Logistics in 2022 was particularly strategic. Payment Logistics had spent 19 years building payment technology specifically for specialty retail and hospitality markets, with deep expertise in Oracle Hospitality OPERA and Oracle Retail Xstore integrations. Bringing that capability into Fortis gave the company validated Oracle integration expertise, a credential that carries real weight in enterprise hospitality and retail procurement decisions.

Greg Cohen, who leads the company as CEO, is an experienced payments industry executive whose public commentary at industry events like ETA TRANSACT reflects genuine strategic thinking about the direction of embedded payments and commerce. The leadership team also includes EVP Timmy Nafso and SVP of Product and Innovation Kevin Shamoun, who has represented Fortis on AI and payments technology panels at major industry conferences.

From a market positioning standpoint, Fortis competes primarily in the embedded payments and ISV partnership space, where it goes head-to-head with providers like Stripe, Braintree, and NMI rather than with traditional ISO-based processors. The company explicitly targets software companies, ERP providers, and enterprise platforms that want to embed frictionless payment acceptance into their own products.

Core Payment Processing Capabilities

At its foundation, FortisPay provides full-service payment processing covering credit cards, debit cards, ACH, and eCheck payments across in-store, online, and mobile environments. The platform handles standard authorization, clearing, and settlement workflows, with processing infrastructure backed by Wells Fargo Bank as the acquiring bank.

Credit and debit card acceptance spans all major card networks, with support for EMV chip cards, contactless payments, and magnetic stripe transactions. ACH processing supports both one-time and recurring payments, making it suitable for subscription billing, invoicing, and B2B payment flows where the lower transaction cost of ACH is preferable to card interchange. The distinction between eChecks, which are single-transaction bank transfers, and ACH, which supports recurring use, is maintained within the platform to give merchants appropriate flexibility for different payment scenarios.

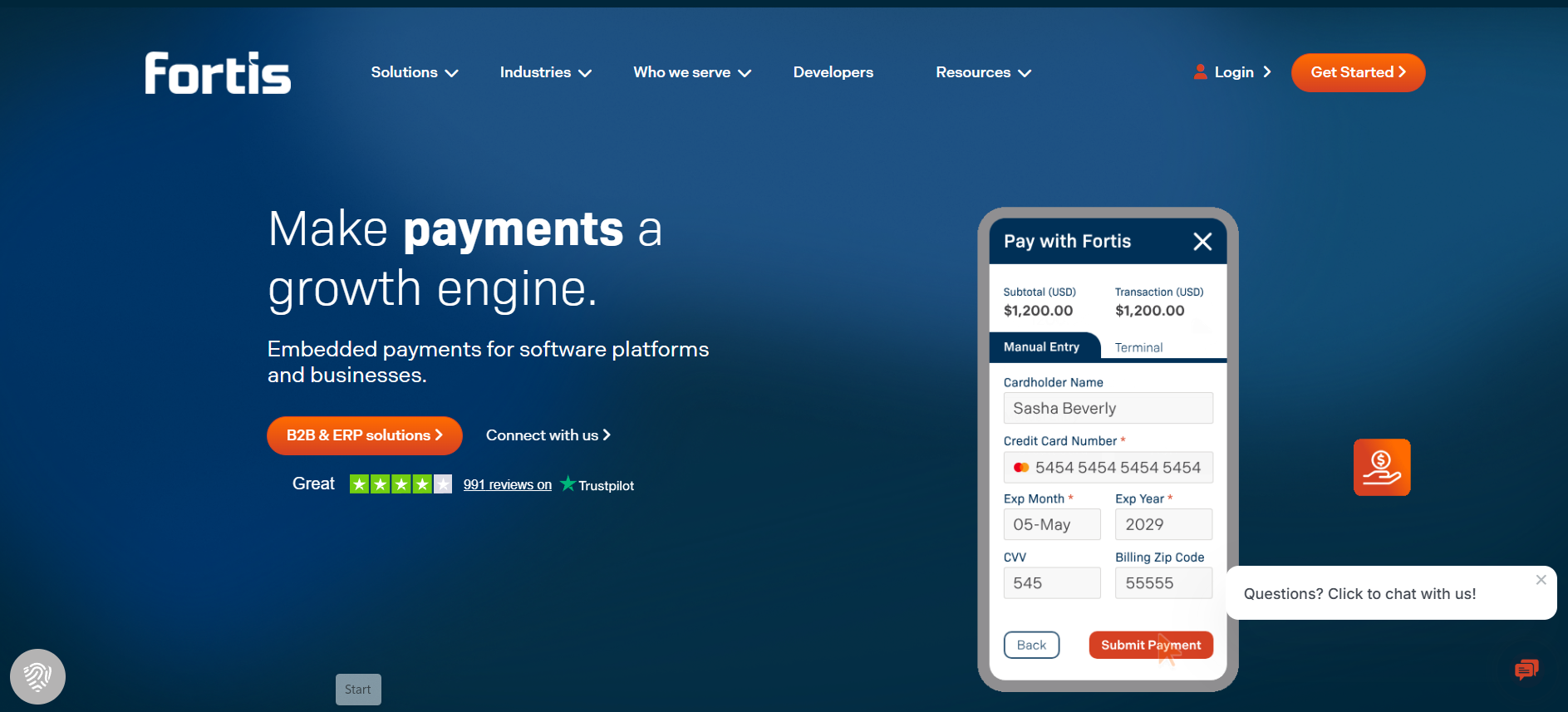

Virtual Terminal is one of the features offered in this product, allowing customers to manually take payments via a computer using no additional devices other than just a computer itself. It is especially important for those organizations that provide phone ordering and professional services or need to enter transaction information on an occasional basis.

ACH functionality of the service was positively commented upon by the customers of the solution, highlighting its transparency regarding anticipated settlements. For instance, one of the G2 reviewers mentioned the benefit of knowing when ACH deposits would be made. On the other hand, one of the limitations associated with this service mentioned by the same group of customers is the existence of holds for transactions over $20,000.

Embedded Payments and the ISV Partner Program

The clearest expression of FortisPay’s current strategic identity is its embedded payments offering for independent software vendors and platform companies. This is where the company has invested most aggressively, and it represents the most differentiated part of its value proposition relative to traditional processor competitors.

The ISV partner program allows software companies to embed payment acceptance directly into their platforms, removing the need for their end-customers to manage separate processor relationships. Fortis handles the acquiring, compliance, and processing infrastructure in the background while the ISV’s customers experience payments as a native feature of the software they already use. The partner model also includes revenue-sharing arrangements, allowing ISVs to earn a share of the transaction revenue generated by their embedded payment deployments.

The revenue-sharing aspect of this product is a considerable factor for software providers considering payment partnerships. Instead of only being able to pay for payment functionality, the ISV is able to leverage its payment integration to create another revenue stream for itself. If the software platform is able to generate enough transactions, then this could prove to be quite an economic shift.

Fortis has made efforts to develop formal integrations between its payments system and other enterprise-level software systems in order to add credibility to its payment solution. One such example of this is the Oracle Validated Integration Expertise Certification for both Oracle Hospitality OPERA and Oracle Retail Xstore. This shows that Fortis’ payment integration has been successfully vetted by Oracle to function properly within their software ecosystem.

eveloper Tools and API Infrastructure

For ISVs and developers evaluating FortisPay, the quality of the API and developer tooling is often the deciding factor. Fortis has invested meaningfully in this area, and the developer experience is one of the platform’s recognized strengths.

The Fortis API has been recognized as a Best of Breed system since 2018 across multiple evaluation cycles, reflecting sustained investment in API quality rather than a one-time effort. The developer portal includes a comprehensive set of resources: step-by-step tutorials, full SDK generation, Postman collections for testing, a request inspector, sample code in multiple languages, real-time code consoles that allow in-browser testing, and a team collaboration dashboard. This is a developer environment built with the expectation that teams will be doing serious integration work, not just basic connection testing.

Availability of the full software development kit is an important differentiator. Using an SDK makes it possible to develop custom integration solutions much faster than if only API was available. With the help of the sandbox environment, developers can test their solutions for integration with Stripe ahead of time and prevent mistakes at the production stage.

The end-to-end API onboarding with e-sign and auto-configuration features make the process of merchant onboarding streamlined for ISVs managing hundreds of sub-merchants simultaneously. Such automated infrastructure is crucial for software platforms since it provides them with the ability to onboard customers automatically without having to manually underwrite each merchant account.

An ability to integrate Tap to Pay on iPhone features announced for 2025 is an important benefit for developers as well as ISVs. It allows them to create a solution for accepting payments directly from the iPhone without the need for extra equipment, making it valuable for mobile business owners and the hospitality industry.

Vertical Market Focus and Industry Solutions

One of FortisPay’s clearest differentiators from generalist processors is its depth of focus across specific vertical markets. Rather than building generic payment tools and applying them broadly, Fortis has developed industry-specific solutions and partnerships for healthcare, hospitality, retail, construction, manufacturing, and professional services.

In healthcare, Fortis targets practices that sit between the hospital-scale EHR deployments and basic standalone processors, including chiropractors, mental health clinics, physiotherapists, and specialty medical practices. The platform supports patient payment portals, text-to-pay, mobile payment notifications, and online billing, reflecting the shift in patient payment behavior away from mail-based billing. Integration with healthcare software systems including the Genesis EHR platform has been specifically mentioned in positive user reviews, which validates the depth of these integrations rather than leaving them as theoretical claims.

In the hospitality sector, the Oracle OPERA implementation and collaboration with platforms such as Visual Matrix and Union POS represent actual enterprise-level implementation knowledge. The firm has actively collaborated with Best Western Hotels & Resorts during regional conferences, which is indicative of its strategic focus on lodging in addition to food service offerings.

Regarding construction and manufacturing industries, Fortis has generated sector-focused content and solutions involving AR automation, rapid invoicing to cash cycle, and ERP integration, with Sage Recommended Solutions certification denoting verified integration with Sage ERP software. Such industry-specific initiatives are significant due to the unique payment issues faced by construction and manufacturing industries, especially with respect to lengthy billing periods and retainage.

Payment Gateway and Omnichannel Capabilities

FortisPay’s gateway infrastructure supports omnichannel payment acceptance across in-store, online, mobile, and text-based channels. This breadth of coverage allows businesses to meet customers wherever they prefer to pay without managing separate gateway relationships for different sales channels.

Web payments functionality allows businesses to collect payments at the point of booking or appointment scheduling, which is particularly useful for healthcare practices that want to capture payment information before a visit rather than chasing receivables after the fact. The ability to integrate payment collection into the patient intake or appointment booking workflow has a direct impact on collections rates and cash flow timing.

Text-to-pay and email invoicing extend payment acceptance into asynchronous channels, allowing merchants to send payment links directly to customers who can complete transactions on their own devices without requiring a dedicated app or a specific browser environment. For service businesses managing distributed billing across a customer base, these channels reduce the friction between invoice and payment.

The platform also supports advanced invoicing workflows, including scheduled payments, recurring billing, and installment plans. These capabilities are particularly relevant for businesses in professional services, healthcare, and B2B environments where single-transaction billing models do not reflect how revenue is actually collected.

Fortis Capital, introduced as part of the platform’s expanded commerce suite, provides short-term financing for small businesses and merchants, covering working capital needs for bills, payroll, and inventory with same-day funding availability. This extends Fortis’s role beyond payment acceptance toward broader financial services, following a pattern seen across several payments platforms that have recognized the adjacent opportunity in merchant financing.

Hospitality and Retail Specialization

Fortis’s acquisition of Payment Logistics and its achieved Oracle Validated Integration status have made hospitality and retail among its strongest vertical capabilities. These are not surface-level integrations. The Oracle OPERA integration for hotel property management systems and the Oracle Retail Xstore integration for POS environments reflect deep technical work validated by Oracle’s own review process.

For hotel operators using OPERA as their property management system, having a payment processor that is natively integrated rather than relying on middleware or workarounds reduces both technical risk and day-to-day operational friction. Payment data flows directly between the POS or PMS and the processor without manual intervention, improving reconciliation accuracy and reducing the administrative overhead associated with managing separate systems.

The partnership with Visual Matrix, a hotel operating system provider, further demonstrates Fortis’s investment in the hospitality sector beyond just Oracle-based environments. Covering multiple hotel technology ecosystems rather than a single vendor gives Fortis broader applicability across the diverse landscape of property management tools used by independent hotels and smaller chains.

For retail environments, the Xstore integration supports enterprise retail POS deployments at the scale where Oracle’s tooling is typically found. Fortis has also supported Tap to Pay on iPhone implementations specifically for hospitality environments, citing reduced transaction times and hardware savings for high-volume venues where every second at POS has direct revenue implications.

Pricing Structure and Fees

Pricing at FortisPay follows the pattern common among embedded payments and B2B-focused processors, rates are customized per merchant and not published publicly. This requires direct engagement with the sales team to obtain a quote, which is a standard friction point for merchants who want to compare providers before entering a sales conversation.

Fortis does offer interchange-plus pricing, marketed under the Select+ product name for higher-volume merchants. Interchange-plus is the more transparent and generally more cost-effective pricing model, passing card network costs through at actual interchange rates and adding a fixed processor markup rather than using the opaque tiered pricing approach that many competitors apply.

Known fee data from independent reviews indicates a $75 application fee and a $25 chargeback fee. Contract terms for standard merchant accounts appear to be structured around one-year commitments with an early termination fee of $99 if canceled before the term ends. This is considerably shorter and less financially punitive than the three-year contracts with $495 termination fees common among some competitors, which is a meaningful practical difference for merchants evaluating commitment risk.

Monthly fees apply, though the specific amounts vary by account type and product selection. Some user reviews have noted billing continuing after account closure as a recurring complaint, which is a pattern merchants should guard against by obtaining written confirmation of cancellation and monitoring their bank accounts after exiting. Merchants should request a complete written fee schedule before activation, covering all monthly charges, per-transaction fees, and any fees specific to the features or integrations they plan to use.

Contract Terms and Merchant Agreements

Contract terms at FortisPay appear to be less onerous than those of some competing processors, particularly with respect to term length and early termination fees. The one-year contract term and $99 early termination fee represent a more manageable commitment structure than the multi-year agreements with several-hundred-dollar exit fees that have generated significant controversy at other providers.

However, the acquisition history of Fortis introduces a specific complication that merchants should be aware of. Several reviews from merchants who were originally with Blue Dog Business Services or other acquired brands were transferred to Fortis’s terms without full clarity about the implications of that transition, including fee changes and the application of early termination provisions under a new contract they did not explicitly sign. One reviewer specifically noted that fees increased after the Blue Dog acquisition and that a PCI compliance fee was applied retroactively, creating a dispute about which entity’s contract terms applied.

This transition-related friction is not unusual when a processor is acquired, but it is worth understanding for any merchant engaging with Fortis today: the company may acquire or integrate additional providers going forward, and the terms of any such integration could affect existing merchant accounts. Merchants should specifically ask whether the agreement they sign contains any provisions addressing what happens to contract terms in the event of future acquisitions or rebranding.

Cancellation process clarity is important to establish upfront. Independent reviews indicate that some merchants experienced continued billing after believing they had successfully canceled, making written confirmation of cancellation and post-cancellation bank monitoring essential steps.

Security and Compliance

FortisPay’s security infrastructure covers the standard requirements for modern payment processing and extends them in ways relevant to its enterprise and healthcare client base. The platform is PCI DSS compliant, which is the baseline requirement for any processor handling cardholder data at scale.

Tokenization and encryption are standard features across the transaction lifecycle, ensuring that sensitive payment data is protected both in transit and at rest. For embedded payments deployments where the ISV or software partner is handling payment flows within their own application environment, the security architecture is designed to limit the scope of PCI compliance requirements that fall on the software developer rather than on Fortis, reducing the compliance burden on partner organizations.

For healthcare clients specifically, the combination of PCI compliance with HIPAA-aware payment workflows is an important consideration. While payment processing and protected health information operate under different regulatory frameworks, the integration of payment collection into clinical or patient-facing software requires careful attention to data handling boundaries. Fortis’s published healthcare content acknowledges this complexity, though merchants in regulated healthcare environments should verify the specific compliance posture of any integrated solution with their own compliance team.

The platform also addresses chargeback management, with published guidance around chargeback prevention, dispute resolution, and fraud reduction across its hospitality and retail verticals. The dedicated chargeback support role mentioned in positive user reviews suggests a structured approach to dispute resolution rather than a generic back-office function.

Reporting and Analytics

FortisPay provides reporting and analytics capabilities through its merchant dashboard, which allows businesses to view transaction history, track settlement activity, and generate customized financial reports. The reporting environment has received generally positive feedback in user reviews, with merchants noting that the dashboard is intuitive to navigate and that transaction notifications are timely and informative.

The platform supports real-time transaction monitoring, which is particularly valuable for businesses managing payment activity across multiple locations or payment channels simultaneously. The ability to see payment status as transactions occur rather than waiting for end-of-day reconciliation gives finance teams and operations managers more immediate visibility into cash flow.

For ISV partners, the reporting infrastructure extends into the embedded payments environment, giving software companies visibility into the transaction activity of their own customer base. This consolidated reporting capability supports the revenue-sharing calculations that underpin the ISV partner program and gives platform operators the data they need to manage their payment portfolio actively.

Advanced reporting features including AR aging reports, invoice-to-cash cycle analysis, and integration with ERP reporting environments have been areas of active product development, particularly as Fortis has deepened its relationships with Sage and other ERP platforms. The goal, as expressed in the company’s published content, is to move reconciliation from a backward-looking accounting exercise to a real-time visibility tool integrated into the broader financial management workflow.

Customer Support

Customer support at FortisPay presents a mixed picture that reflects the company’s dual identity: a growing technology platform with enterprise ambitions, and a merchant services provider navigating the service challenges that come with rapid expansion through acquisition.

On the positive side, Trustpilot reviews from verified users in 2025 and 2026 consistently mention specific support representatives by name and describe interactions characterized by genuine knowledge and responsiveness. A chiropractic practice review praised the simplicity of the system and quality of support. A review from a business using Fortis for ACH processing highlighted a support representative who thoroughly explained fee structures and payment options. These are the kinds of specific, named, positive interactions that suggest genuine service quality at the individual level.

The negative side is also documented. Some Trustpilot reviews describe being transferred between subsidiary companies when calling for technical support, with hold times exceeding 40 minutes before being disconnected. One reviewer noted an issue that required dealing with an older processor entity under the Fortis umbrella, suggesting that the integration of acquired businesses into a unified support experience has not been fully completed. This fragmentation is a predictable consequence of rapid acquisition-led growth and is an area the company will need to continue addressing as its portfolio of acquired entities matures.

Merchants engaging with Fortis should establish clear support escalation paths before they need them, understand which entity is responsible for which components of their service, and confirm that there is a single primary contact point for account management rather than relying on routing through multiple subsidiaries.

Strengths, Limitations, and Who It’s Best For

FortisPay is a genuinely capable platform that has made a credible transition from traditional merchant services toward embedded payments leadership. Its API quality, Oracle Validated Integration credentials, vertical-specific depth in healthcare and hospitality, ISV revenue-sharing model, and developer-first tooling are real differentiators that compare favorably against many competitors in the embedded payments space. The one-year contract term and relatively modest early termination fee are practical advantages over processors that demand three-year commitments with significantly higher exit costs.

The limitations are real and worth acknowledging honestly. Pricing transparency requires a sales conversation, which creates friction for merchants who want to self-serve through the evaluation process. Support quality is uneven, with the fragmentation across acquired entities creating inconsistent experiences for merchants who land in different parts of the organization. Continued billing after cancellation appears as a recurring complaint pattern, suggesting that the account closure process requires clearer management. The iOS-only mobile app limits Android users from accessing full mobile payment functionality, which is a gap that narrows the platform’s reach in certain markets.

The merchant most likely to benefit from FortisPay is a software company, ISV, or ERP provider looking for an embedded payments partner with strong API tooling, enterprise integration credentials, and a revenue-sharing model. Mid-market businesses in healthcare, hospitality, construction, or manufacturing that need a processor with genuine vertical expertise rather than a generic acquiring relationship will also find real value. Smaller merchants with simple, standalone payment processing needs may be better served by providers whose offerings are more directly sized to their operational complexity, though FortisPay’s shorter contract terms make evaluation less risky than with some alternatives.

FAQs

Q1. What makes FortisPay different from a standard payment processor, and is it suitable for businesses that are not software companies?

FortisPay’s primary strategic focus is on embedded payments for software platforms and ISVs, which distinguishes it from processors that primarily serve merchants directly. However, the platform also serves mid-market and enterprise businesses directly, particularly in healthcare, hospitality, retail, construction, and manufacturing.

Non-software businesses can benefit from FortisPay’s vertical-specific features, AR automation tools, and omnichannel payment capabilities without needing to be a software company themselves. The platform is best suited for businesses that have meaningful payment complexity, whether that is recurring billing, B2B invoicing, ERP integration, or high-volume transaction environments, rather than businesses with simple, low-volume card acceptance needs.

Q2. How does FortisPay handle the transition for merchants who were previously with one of its acquired companies, such as Blue Dog Business Services?

Merchants who were originally onboarded through an acquired entity, such as Blue Dog Business Services or EpicPay, have in some cases experienced disruption during the transition to FortisPay’s systems, including fee changes and contract term questions. The company has acknowledged these concerns in public responses to reviews and stated that it reaches out to affected merchants through its support team.

Merchants in this situation should request clear documentation of their current contract terms under the Fortis entity, confirm that the pricing and fee structure matches what they agreed to, and establish a direct contact point within FortisPay’s corporate support team rather than relying on legacy contact information from the acquired brand. If there are discrepancies between the original agreement and current billing, those disputes should be raised in writing with a request for formal resolution.

Q3. Is FortisPay a good fit for healthcare practices, and what specific payment features does it offer for that sector?

FortisPay has invested specifically in healthcare payment capabilities and is a credible option for medical practices, particularly those in non-hospital settings such as chiropractic, mental health, physiotherapy, and specialty medical. The platform supports patient payment portals, web payments collected at the point of appointment booking, text-to-pay, and email payment links, covering the digital payment methods that research indicates patients use most and that are associated with faster payment rates.

Integration with healthcare software systems including the Genesis EHR platform provides the embedded payment experience that reduces manual billing steps for practice staff. The revenue-sharing model available to healthcare ISVs also means that practice management software companies can embed Fortis payments and earn revenue from those transactions. Practices should verify that the specific EHR or practice management software they use is supported through a current Fortis integration before committing to the platform.

Best Product & Services

Recent Posts