UnionPay Review

10

Nov 2025

No Comments

UnionPay Review

UnionPay is one of the world’s biggest payment networks, founded in 2002 and headquartered in Shanghai, China. It was born with the idea of building a domestic payment network that could rival Visa and Mastercard. Over time, UnionPay expanded beyond China to become a major player in the global payments space. Today it serves billions of cardholders and millions of merchants across the globe. Lets read more about UnionPay Review.

The company’s journey mirrors China’s growing influence in the global financial system. Initially focused on interbank card transactions within China, UnionPay developed capabilities in cross-border payments, e-commerce and mobile technology. With the establishment of UnionPay International, the brand gained access to overseas markets through partnerships with banks and payment processors.

UnionPay’s value lies in its dual identity; it is both a national infrastructure supporting domestic commerce in China and a competitive international payment brand. Its reach now extends to tourism, retail and online commerce. This review will cover UnionPay’s global footprint, digital payment solutions, business integrations and overall value proposition for merchants and users in 2025.

Global Reach and Market Presence | UnionPay Review

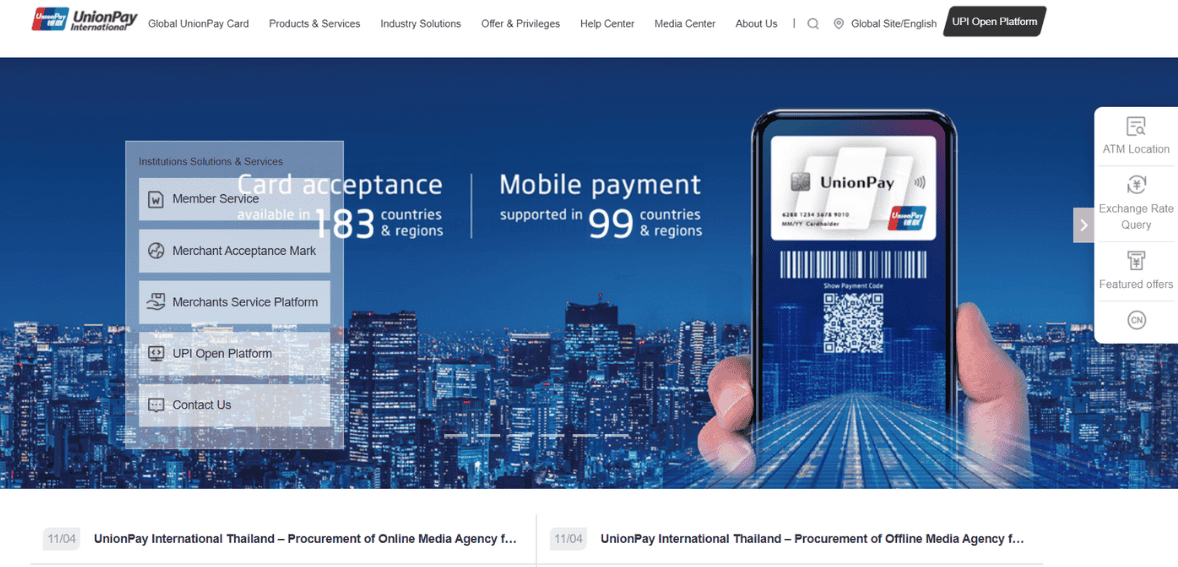

UnionPay’s global expansion has been one of the most impressive in the financial services industry. It’s in over 180 countries and regions, with over 10 billion cards issued worldwide. It’s number one in Asia, especially in China where it’s the default card. In recent years it’s been rapidly expanding in Europe, Africa and the Middle East.

Partnerships with local acquirers and banks have been key to this success. In North America for example, UnionPay cards are accepted at many ATMs and merchants through partnerships with Discover and other networks. In Africa, partnerships with regional banks have enabled UnionPay to grow in markets like Kenya, Nigeria and South Africa. UnionPay International is focusing on building interoperability with global payment systems.

Despite the impressive coverage, UnionPay’s penetration outside of Asia is still limited compared to Visa or Mastercard. Western merchants may not support UnionPay as frequently due to regulatory hurdles or low local demand. But its consistent growth and strategic partnerships show a long term commitment to global inclusion, so it’s definitely one to watch in the international payments space.

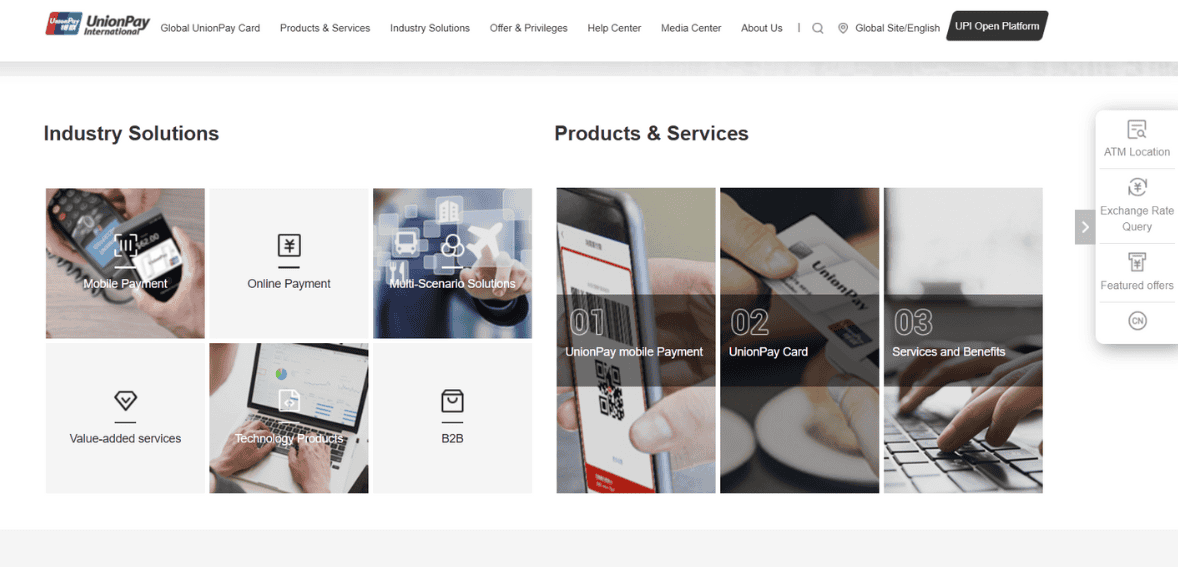

Core Products and Services

UnionPay offers a diverse suite of products designed to serve consumers, merchants, and financial institutions. Its traditional card products; credit, debit, and prepaid; form the foundation of its global network. UnionPay cards can be issued in local currencies or configured for multi-currency use, providing flexibility for international travelers and online shoppers.

In addition to card-based solutions, UnionPay has invested heavily in digital payment technologies. Its QuickPass platform supports contactless payments through NFC-enabled devices, while QR-based payment systems allow users to make purchases directly from smartphones. These innovations make UnionPay accessible to tech-savvy consumers and small businesses that rely on mobile transactions.

It also offers financial institutions white-label solutions for card issuance and transaction management. For merchants, its systems provide secure payment acceptance across in-store, online, and mobile environments. Beyond payments, it supports value-added services like loyalty programs, cross-border settlement, and data analytics. This wide-ranging product ecosystem positions UnionPay as more than a card network; it is an integrated payment infrastructure aiming to meet modern commerce demands.

UnionPay International: Cross-Border Capabilities

UnionPay International is the company’s global business arm and plays a key role in its cross-border strategy. It allows cardholders to pay and withdraw cash in multiple countries with the same card and provides international access. This division also partners with foreign banks, fintech platforms and acquirers to expand UnionPay’s global reach.

One of UnionPay International’s biggest strengths is its cross-currency support. Travelers and online shoppers can pay in local currency and funds will be settled through UnionPay’s secure network. It has become the preferred choice for Chinese tourists and overseas students who want familiarity and cost-effective payment solutions abroad.

To ensure interoperability, UnionPay International complies with international standards such as EMV and ISO protocols. Its partnerships with global payment processors ensure compatibility with existing merchant systems, so it’s easier for merchants to accept UnionPay cards. However in Europe and Americas, brand recognition is still a challenge. But UnionPay International is gaining traction as an alternative to Western networks, offering stability, lower fees and wider coverage.

Mobile and Digital Payment Ecosystem

UnionPay has made significant progress in digital transformation through its QuickPass and mobile QR payment ecosystem. QuickPass enables users to make tap-and-go transactions with smartphones, wearables, or contactless cards. This system mirrors similar technologies from Visa PayWave and Mastercard Contactless but integrates deeply with Asian mobile payment preferences.

In China and other Asian markets, QR code payments have become a cornerstone of everyday commerce. UnionPay’s QR solutions support interoperability with other regional networks, enabling merchants to process payments from multiple wallet providers. The company’s mobile payment infrastructure aligns with the global shift toward cashless and contactless experiences, particularly after the pandemic accelerated digital adoption.

It has also integrated with Apple Pay, Huawei Pay, and Samsung Pay in select regions, allowing seamless tokenized transactions. Its emphasis on real-time authentication and encryption ensures secure digital interactions. While mobile payment adoption remains regionally uneven, UnionPay’s continued investments in fintech collaborations and app integrations show its adaptability to emerging digital commerce trends worldwide.

Security Features and Compliance

UnionPay places a strong emphasis on transaction security, regulatory compliance, and consumer protection. Its systems follow international security frameworks, including PCI DSS and EMV chip technology, ensuring encrypted and tamper-resistant transactions. Every card transaction is monitored through a multilayered risk-control system designed to detect fraud in real time.

The network also implements tokenization for mobile and online payments, which replaces sensitive card data with secure digital tokens. This significantly reduces exposure to potential breaches during digital transactions. Additionally, It collaborates with law enforcement and banking partners to strengthen cybersecurity awareness and prevent card-related crimes.

From a compliance standpoint, UnionPay adheres to global AML and KYC regulations. It maintains close relationships with regulators across markets to meet localized data and privacy requirements. Despite these efforts, regional users occasionally report slower dispute resolutions compared to Western networks. Nonetheless, It’s comprehensive security protocols make it a trusted payment system for both consumers and businesses across multiple jurisdictions.

Merchant and Business Solutions

UnionPay provides merchants with a wide range of tools to accept payments across channels. Its POS systems support chip, magnetic stripe, contactless, and QR transactions, ensuring compatibility with existing retail hardware. Merchants can also integrate UnionPay’s e-commerce gateway for online sales, which supports local currencies and multicountry settlements.

For small and medium-sized enterprises, It offers simplified onboarding and affordable processing fees, helping businesses expand their customer base. Many tourism-dependent markets particularly benefit from UnionPay’s acceptance among Chinese travelers, which drives sales for hotels, retailers, and restaurants.

The company’s business solutions extend beyond payment acceptance. It’s data analytics and customer engagement tools help merchants understand consumer spending patterns. Additionally, loyalty programs and promotional integrations provide marketing value. However, UnionPay’s merchant service availability can vary by country, especially in regions with limited banking partnerships. Even so, as global e-commerce continues to grow, UnionPay’s merchant solutions present a viable path to accessing an increasingly digital, cross-border customer base.

UnionPay Online Payment Platform

UnionPay Online Payment serves as the brand’s digital payment gateway, designed for secure e-commerce and mobile transactions. It allows customers to make purchases using their UnionPay cards without sharing sensitive financial information with merchants. The platform employs advanced encryption and multi-factor authentication to safeguard transactions.

UPOP supports multiple currencies, languages, and settlement models, catering to international merchants and cross-border customers. Its integration capabilities enable developers to embed UnionPay into various websites and apps via APIs and SDKs. This makes it an accessible and flexible solution for businesses looking to expand globally.

From a user perspective, UPOP offers a simple checkout experience similar to other digital wallets, but with a strong emphasis on security and speed. It also supports recurring billing and installment payments, appealing to online retailers and subscription-based businesses. While UPOP may not yet match PayPal or Stripe in terms of global adoption, it represents UnionPay’s strong push into the digital payment ecosystem with reliable infrastructure and continuous enhancements.

Pricing, Fees, and Merchant Costs

UnionPay’s pricing structure varies across regions and merchant categories. In general, the company is known for maintaining competitive interchange rates, particularly in Asian markets. Its lower processing costs make it appealing for merchants targeting travelers from China or other Asia-Pacific countries.

Typical fees include transaction processing charges, cross-border surcharges, and exchange rate margins for currency conversion. Compared to global rivals like Visa or Mastercard, it often provides slightly lower overall costs, especially for domestic transactions within Asia. This advantage has supported its widespread adoption among cost-sensitive merchants and regional acquirers.

However, outside Asia, UnionPay’s fee structures can be influenced by local partners and banking networks. In some regions, setup or maintenance costs may offset its lower interchange benefits. Transparency in pricing also depends on third-party processors. Despite these variations, It’s affordability remains one of its key strengths, particularly for small businesses and global e-commerce platforms looking to diversify payment options without significantly increasing costs.

Customer Experience and Support

UnionPay’s customer experience varies depending on region and service channel. In China and much of Asia, users benefit from localized support centers and 24-hour helplines. The company provides multilingual assistance through phone, email, and online chat options, covering card issues, disputes, and fraud claims.

Feedback on responsiveness is generally positive in core markets, though international users sometimes report slower turnaround times. Dispute resolution processes, especially for cross-border payments, can take longer due to varying intermediary banks and regional policies. UnionPay continues to address this through its expanding network of international offices and customer engagement initiatives.

The overall user experience is enhanced by the brand’s intuitive digital platforms and reliable payment systems. For merchants, it provides onboarding assistance and integration support. While its service quality might not yet equal global leaders, steady improvement in global customer relations reflects UnionPay’s commitment to achieving international service standards that align with its growing footprint.

Integration with Global Fintech and Banking Systems

UnionPay’s success in the international arena is partly due to its collaborations with global fintech firms and financial institutions. By partnering with major acquirers and gateway providers, It ensures that its cards are compatible with most modern POS systems and online platforms. These partnerships simplify merchant onboarding and enhance user accessibility.

The company has also explored synergies with fintechs offering mobile wallets, neobanking services, and cross-border remittances. Integration with digital payment ecosystems like Apple Pay, Huawei Pay, and Samsung Pay demonstrates it’s ability to adapt to global technology trends. Additionally, it invests in blockchain-based experiments to streamline settlement and improve transparency.

In banking, it collaborates with more than 2,500 institutions worldwide for card issuance, transaction processing, and payment innovation. This collaborative model helps maintain flexibility in local markets. While regulatory complexity sometimes slows down deployment in certain countries, UnionPay’s openness to co-innovation positions it well within the rapidly evolving global fintech landscape.

trengths and Competitive Advantages

UnionPay’s greatest strengths lie in its scale, affordability, and technological adaptability. Its unparalleled reach across Asia provides a solid foundation for international expansion. The network’s cost-effective fee structure attracts merchants, while partnerships with local financial institutions ensure regional relevance.

The company’s focus on innovation has kept it competitive in a rapidly evolving payment environment. Its mobile and QR-based payment solutions align with consumer preferences in key markets, and the integration of contactless technology allows it to compete directly with established Western networks. Furthermore, UnionPay’s compliance with international standards enhances trust and credibility.

Another core strength is its government support within China, which ensures financial stability and operational resilience. UnionPay’s continuous investment in global partnerships helps bridge market gaps, creating a sustainable presence outside Asia. Together, these advantages make UnionPay a reliable and forward-looking player in the global payment industry, even as it navigates challenges of market perception and competitive maturity.

Limitations and Areas for Improvement

Despite its impressive growth, It faces several limitations. Its brand recognition remains lower in Western markets, where Visa and Mastercard have long-standing dominance. This restricts consumer demand and merchant prioritization. Some merchants in North America or Europe still view UnionPay as a niche option catering mainly to Chinese travelers.

Technical integration challenges also persist in certain regions where banking systems rely on legacy infrastructure. These barriers can delay onboarding or increase costs for smaller merchants. Moreover, the company’s dispute resolution processes and customer support availability outside Asia could benefit from greater localization and responsiveness.

Another constraint is regulatory compliance in diverse markets, which requires adapting to varying data protection and financial laws. it has made progress here but continues to face scrutiny in specific jurisdictions. Overcoming these challenges will be essential for UnionPay’s goal of achieving parity with Western networks and strengthening its image as a truly global payment brand.

Ideal Users and Final Verdict

UnionPay serves a wide range of users, from individual consumers to multinational merchants. It is particularly advantageous for travelers, international students, and businesses operating in Asia or targeting Chinese customers. Merchants seeking to diversify payment acceptance can benefit from It’s competitive fees and growing global reach. The platform is also suitable for fintech startups and e-commerce ventures that value secure cross-border payments and flexibility in settlement options. For consumers, it offers convenience, reliability, and access to a vast acceptance network.

However, users outside Asia may encounter limited acceptance compared to Visa or Mastercard. In conclusion, It stands as a formidable force in global payments; strong in scale, security, and innovation. Its continued growth beyond Asia depends on sustained investment in merchant expansion, brand awareness, and localized customer support. As the global economy moves further toward digital integration, It’s steady progress positions it as a valuable alternative in the evolving world of electronic payments.

FAQs

Is UnionPay accepted worldwide?

It is accepted in over 180 countries and regions. While coverage in Asia is near universal, availability in North America and Europe continues to expand through partnerships with banks and acquirers.

How does UnionPay compare to Visa or Mastercard in transaction fees?

It generally offers competitive pricing, particularly for domestic and regional transactions in Asia. However, fees can vary depending on acquirers and currency conversion policies in different countries.

Can businesses easily integrate UnionPay into their payment systems?

Yes. it provides APIs and SDKs that allow easy integration for both online and offline merchants. Global payment gateways increasingly include UnionPay as part of their supported methods, simplifying adoption.

Best Product & Services

Recent Posts