Global Payments Review

By 10topmerchantservices June 4, 2025

Global Payments Inc. is a major force in the fintech and merchant services space. Based in Atlanta, Georgia, the company operates in over 100 countries and processes billions of transactions each year. With a history marked by strategic acquisitions and continuous innovation, it has grown into a key provider of both traditional and modern payment solutions. Businesses of all sizes; from local retailers to global enterprises; rely on its systems to accept payments and manage financial workflows. Lets read more about Global Payments Review.

Even with its strong technology and extensive reach, Global Payments has its share of difficulties. Smaller retailers occasionally have trouble with its pricing transparency and contract terms, but big businesses often value its dependability and scalability. Nevertheless, Global Payments maintains a strong position in the rapidly changing field of commerce technology for companies looking for a flexible and forward-thinking payment partner.

Core Payment Processing Features | Global Payments Review

At the heart of Global Payments is its robust payment processing engine. It supports credit and debit card transactions, ACH transfers, contactless payments, and mobile wallets such as Apple Pay and Google Pay. These services are accessible across in-store, online, and mobile channels, allowing businesses to offer a unified customer experience.

The system is designed for high-volume settings and has quick transaction speeds. Its reliability and steady uptime are often advantageous to companies in the retail, hospitality, and service sectors. Support for a variety of payment methods, such as digital wallets and EMV chip cards, is another important advantage. This helps retailers in keeping up with changing customer demands.

However, pricing can be a sticking point. Variable interchange rates, processing fees, and equipment costs can make it difficult for small businesses to estimate total expenses. There are also occasional complaints about hidden charges or inconsistent billing practices. For merchants who prioritize clarity and predictability, this may be a concern.

Merchant Tools and Business Management Solutions

Global Payments extends beyond basic transaction processing by offering a comprehensive suite of business tools. These include customer data platforms, invoicing systems, real-time reporting, and even marketing support. These tools aim to equip merchants with actionable insights, not just payment capabilities.

One of the more useful features is real-time reporting. Businesses can monitor sales activity, refund trends, and transaction volume through an intuitive dashboard. This allows for better planning and resource allocation. Another advantage is the virtual terminal, which enables payments without the need for physical hardware. This is particularly useful for remote or service-based businesses.

Several third-party systems, such as CRMs and accounting programs like Salesforce and QuickBooks, are also integrated with the platform. These links minimize manual labour and streamline financial operations. However, your service tier or region may affect which features are available. Even though the extra tools are useful, they might cost more. Because standard packages do not include all features, merchants must be aware of optional fees. For expanding companies that require more than just a payment processor, the entire suite is still appealing.

POS Systems and Hardware Options

Global Payments offers a wide selection of POS systems designed to fit different business types. Whether you need a single terminal for a boutique or a full system for a multi-location store, the company provides flexible hardware options.

The in-house POS systems include modern interfaces, inventory tracking, and customer engagement features. These are generally easy to use, even for staff with limited technical knowledge. For businesses already using third-party POS providers, the system supports various integrations, making it adaptable to existing setups.

Another standout feature is mobile point-of-sale systems. Mobile readers and app-based solutions provide security and portability for vendors who work on-the-go, such as market stalls, pop-up stores, or delivery services. Usually, installation is simple, particularly when using Global Payments directly. Onboarding through resellers, however, may result in inconsistent setup support. This can be annoying, and in order to guarantee a seamless deployment, the merchant might need to put in more work.

In summary, the POS offerings are strong, with both flexibility and reliability built in. Just be cautious of potential add-on costs for premium hardware and advanced features.

E-commerce and Online Payment Capabilities

For online businesses, Global Payments delivers a feature-rich suite of e-commerce tools. These include payment gateways, hosted checkout pages, and APIs that allow custom integrations across websites, mobile apps, and digital storefronts. The system supports multiple online payment types such as credit cards, e-wallets, and direct bank transfers. Its APIs are well-documented and developer-friendly, making integration feasible for businesses with technical resources. For companies that rely on recurring payments, such as subscription services or SaaS platforms, Global Payments offers automated billing options and secure customer data storage.

The fact that it can facilitate international e-commerce is another advantage. For merchants looking to enter new markets, its multi-currency support and international acquisition features make it a good choice. Cross-border transactions, however, might come with additional fees, which should be considered when making plans. The platform’s versatility is alluring, but companies without specialised IT personnel might encounter a more challenging setup process. A strong basis for digital expansion is provided by the e-commerce environment’s stability and adaptability once set up.

Security and Compliance Features

Security is a critical component of any payment processor, and Global Payments does not fall short. The company is PCI DSS compliant and uses multiple technologies to protect sensitive data. P2PE and tokenization are standard tools in its security suite. These methods ensure that card data is protected from the moment of entry through storage and transmission. This reduces the risk of data breaches and ensures regulatory compliance.

Additional security features include velocity limits, geolocation checks, and real-time monitoring for fraud detection. These tools reduce the likelihood of chargebacks and assist in flagging suspicious transactions. In order to help merchants stay current with industry standards, the platform also provides tools for PCI compliance assistance. Not all merchants may be able to access the full range of features without paying more because advanced fraud protection tools are often associated with higher-tier pricing plans. However, for the majority of retail and service-based businesses, the basic security tools are sufficient.

International Payments and Currency Support

Global Payments is well-equipped for international commerce, offering support for over 140 currencies. Businesses can accept payments in a customer’s local currency and receive settlements on their own. This simplifies cross-border transactions and can improve conversion rates for global customers. Dynamic currency conversion is available as well, allowing shoppers to view prices and complete purchases in their native currency. While convenient, DCC can sometimes result in a higher total cost for the customer due to exchange rates.

The global acquiring network, which eliminates the need for distinct merchant accounts in several nations, is an additional advantage. This lowers administrative overhead and simplifies financial operations for global corporations. Merchants have pointed out that international service fees can be more than they had expected. If not properly budgeted for, currency conversion fees and other processing expenses could reduce margins. Nevertheless, Global Payments’ tools offer a strong and expandable infrastructure for companies looking to grow globally.

Third-Party Integrations

Global Payments integrates well with a wide range of platforms and software solutions. From accounting tools like QuickBooks to e-commerce platforms like Shopify and Magento, the system is built to plug into many commonly used tools.

The platform also offers APIs for businesses that need custom connections. These APIs are developer-friendly and supported by thorough documentation. Integrations with point-of-sale systems like MICROS and Aloha are particularly useful for restaurants, while healthcare providers benefit from compatibility with practice management software.

The quality of integrations can vary depending on whether you work directly with Global Payments or through a third-party vendor. Some configurations may require technical assistance, which can increase implementation time and cost. But for businesses already using multiple systems, the integration capability offers significant value by improving efficiency and reducing redundancy.

Pricing and Contract Considerations

One of the trickier parts of using Global Payments is pricing. Every merchant has a different rate. The type of business, the volume of transactions, the sales channel, and whether the merchant deals directly with the business or through a reseller all affect costs. Monthly service fees, transaction fees, hardware costs, and fees associated with compliance are a few examples of fees. Flat or tiered rate structures may be offered to certain merchants, while interchange-plus pricing may be available to others.

One frequent complaint is the lack of contract transparency. Merchants have reported surprise charges and confusing cancellation policies. Some agreements include early termination fees or automatic renewals, which can catch users off guard. Larger businesses, especially those processing high volumes, often receive more favorable terms, including custom pricing and dedicated support. Smaller merchants should make sure to request a detailed breakdown of costs before signing any agreement.

Customer Service and User Experience

Customer service is a mixed experience depending on how the account is set up. Businesses that sign up directly with Global Payments generally receive more reliable support. Those who come through resellers may encounter delays or less consistent assistance. Support is available via phone, email, and live chat. The company also offers a resource library and self-service portal. These tools provide access to transaction history, downloadable reports, and user guides. The interface is well-organized and mobile-friendly, helping users manage operations on the go.

Even though the system is reliable and effective, new users might find the learning curve a little challenging, particularly in the absence of onboarding assistance. Though they might not be as comprehensive as those offered by more recent, tech-first providers, the training materials are still beneficial. All things considered, Global Payments offers a strong user experience and a high system uptime. It works well for companies that require dependability and continuous support, as long as the onboarding procedure is conducted via a reliable channel.

FAQs

Q1. Is Global Payments suitable for small businesses or only large enterprises?

Global Payments serves both segments. However, small businesses should carefully review contracts and fee structures to avoid hidden costs.

Q2. Can Global Payments handle international transactions efficiently?

Yes. It supports over 140 currencies and offers cross-border payment solutions, although some transactions may incur additional fees.

Q3. Does Global Payments offer flexible contracts or require long-term commitments?

Contract terms can vary widely. Some merchants report long-term agreements with early termination clauses, so always verify the fine print before signing.

Fulton Merchant Card Services Review

By 10topmerchantservices May 31, 2025

Fulton Merchant Card Services is a payment processing offering from Fulton Bank, a longstanding regional bank known for its financial services across business and consumer segments. As businesses increasingly rely on digital transactions, Fulton Bank has extended its core banking capabilities to include merchant services that help companies process payments across various sales channels. Lets read more about Fulton Merchant Card Services Review.

Fulton has a distinct position in the payment processing market because it is a part of a traditional bank. Consolidating banking and payment operations under one roof may be convenient for businesses that currently bank with Fulton. This setup makes financial reconciliation simpler and account management more efficient.

However, companies looking for advanced, highly customisable, or AI-enhanced payment tools are not the target market for Fulton’s services. Small and mid-sized businesses that value consistency and dependable service over quick innovation will find its more grounded and dependable approach appealing. To assist prospective customers in making an informed choice, this review assesses Fulton’s main products in terms of features, security, cost, hardware, and industry suitability.

Core Services and Payment Capabilities | Fulton Merchant Card Services Review

Fulton offers a well-rounded suite of payment processing tools that cater to physical retail, service-based businesses, and online operations. Businesses can accept all major credit and debit cards using countertop terminals, mobile devices, or fully integrated point-of-sale systems. These solutions are well-suited to brick-and-mortar retailers, restaurants, and contractors alike.

Online merchants can integrate Fulton’s services using a secure payment gateway or a virtual terminal. These tools support card-not-present transactions and allow for both one-time and recurring billing. Virtual terminals are especially helpful for businesses handling remote payments or taking orders by phone.

A notable aspect of Fulton’s service is its ability to tailor payment tools to various industries. Whether in retail or hospitality, businesses can access hardware and software options that reflect their operational needs. Although Fulton does not offer deep custom coding or platform-level flexibility, its solutions are broad enough to meet standard business use cases.

Mobile payment support is another advantage. Merchants working in the field can use secure card readers connected to mobile devices to accept payments on the go. From countertop setups to mobile environments, Fulton covers the foundational needs of businesses seeking to process payments securely and efficiently.

Terminal Hardware and Setup Options

Fulton provides a solid range of hardware options to support different business setups. Its offering includes traditional countertop terminals, wireless models for mobile operations, and fully integrated point-of-sale systems. These devices support chip, magnetic stripe, and contactless payments such as Apple Pay and Google Pay.

Retailers often favor countertop terminals at fixed sites because of their ease of use and dependability. Wireless models are more suitable for mobile applications, like delivery services or payments made at tables in restaurants. Though the hardware options are limited in comparison to specialized suppliers, they sufficiently meet the requirements of most small to medium-sized enterprises.

Fulton collaborates with recognized hardware producers to guarantee that the devices are compatible and easy to use. Setup assistance is provided, allowing businesses to have their systems running with little effort. Businesses can opt for either leasing or purchasing, giving them the choice of reduced initial expenses or advantages of long-term ownership.

Although Fulton’s hardware lineup may not include the latest innovations or advanced touchscreen terminals, it performs reliably and fits well within the bank’s service-oriented approach. Businesses looking for tried-and-tested payment tools will find the hardware practical and sufficient for daily operations.

Online Payments and Virtual Terminals

Fulton’s online payment tools revolve around its secure payment gateway and virtual terminal, designed to accommodate businesses that need to process digital or remote payments. These services are essential for online retailers, subscription-based companies, or those accepting orders by phone.

The virtual terminal allows merchants to manually enter card information through a secure web interface. This is particularly helpful for invoicing or phone-based sales, offering flexibility without needing physical hardware. For eCommerce, Fulton’s gateway integrates with common shopping cart systems, allowing real-time transaction processing on a merchant’s website.

Security measures such as SSL encryption and tokenization are built into these tools, helping protect sensitive cardholder data. The system also supports recurring billing setups, which is useful for service providers and subscription-based businesses.

While the virtual terminal and gateway are easy to use, they do not offer some of the more advanced features found in newer fintech platforms. There are limited customization options, and analytics dashboards are basic. Still, for businesses needing a simple, secure online payment solution, Fulton’s tools are adequate and accessible without requiring technical expertise.

Pricing Structure and Transparency

Fulton’s pricing structure includes several components, such as monthly account fees, transaction fees, and charges for additional services like gateways or hardware. However, exact pricing details are not readily available on the website, and businesses typically need to speak with a representative to receive a customized quote. This lack of upfront transparency may be a drawback for businesses that prefer to compare rates online. While personalized quotes can lead to tailored solutions, it introduces a level of unpredictability that some businesses may find inconvenient.

The terms of the contract are also important to note. Fulton may charge early termination fees and demand multi-year commitments. Businesses that expect their service requirements to change or who wish to have the freedom to switch providers may find this to be a sticking point. On the other hand, a lot of the more recent processors provide month-to-month plans that don’t charge cancellation fees.

For companies who already work with Fulton Bank or who value direct assistance, the value might still be high in spite of these factors. Nevertheless, before committing, prospective customers should be sure to inquire in-depth about fees, contract duration, and any additional expenses.

Security and Fraud Protection Measures

Security is a central focus in Fulton’s merchant services. The company complies with PCI-DSS standards, which are designed to protect sensitive cardholder data and ensure secure transaction processing across all channels. Encryption protocols protect data in transit, and tokenization is used to reduce the risks associated with storing card information. These features help shield businesses from data breaches and fraudulent activity, whether payments are made in-store, online, or via mobile devices.

Fulton also equips merchants with fraud prevention tools, including AVS, CVV checks, and the ability to set custom transaction limits. These features help detect unusual activity and add a layer of security to payment processing.

In addition to built-in safeguards, Fulton supports merchants in maintaining compliance. This includes guidance on completing PCI self-assessment questionnaires and understanding ongoing data protection requirements. Although Fulton’s fraud tools are more traditional and lack advanced real-time AI-based detection, they are reliable and user-friendly, especially for businesses with limited technical backgrounds.

Customer Service and Account Support

One of Fulton’s strongest features is its customer service approach. Businesses can access support through phone, email, or by visiting one of Fulton Bank’s branches. This hybrid model is ideal for clients who value direct, human interaction over automated self-service options.

The majority of companies that work with Fulton are given a personal account manager. Onboarding, troubleshooting, and ongoing account management are all supported by these agents. For smaller businesses that might not have specialised in-house IT or finance teams, the individualised service helps ensure continuity and fosters trust.

Support availability, however, might be restricted to regular business hours. Assistance might not be immediately available to businesses that operate on the weekends or after hours. Additionally, because Fulton’s reach is mainly regional, responsiveness and service quality may differ based on the location. The majority of customer feedback is favourable in spite of these restrictions. Local banking assistance and committed agents provide a degree of attention that is often missing from bigger, tech-driven providers.

Reporting Capabilities and Business Insights

Fulton offers basic reporting tools to help merchants keep track of payment activity. The merchant portal provides access to daily summaries, batch settlement data, and monthly statements. These can be downloaded in formats like PDF or CSV for additional processing or recordkeeping. The focus of the reporting suite is primarily on transaction volumes, chargebacks, and payment summaries. While these tools are functional for basic oversight, they do not offer the advanced features seen in more modern platforms, such as visual dashboards, automated insights, or business intelligence tools.

Integration with external accounting software may be possible, but it generally requires manual exporting rather than real-time syncing. This could be a minor inconvenience for businesses that rely heavily on tools like QuickBooks or Xero. Overall, the analytics and reporting capabilities are best suited to businesses that want simple visibility into their financial transactions. For data-driven enterprises seeking deep insights or predictive analysis, Fulton’s tools may feel limited.

Best Fit Industries and Business Use Cases

For companies in the retail, healthcare, hospitality, educational, and professional services sectors, Fulton Merchant Card Services is a solid choice. Its solutions provide sufficient flexibility for a range of business models and can be tailored to both storefront and service-based operations. A small or medium-sized company that values banking relationships, reliable support, and secure payment handling is Fulton’s ideal client. For instance, having banking and payment services under one provider could be convenient for a dental clinic or independent retailer.

However, companies that require advanced payment infrastructure or high-risk industries are not specifically served by Fulton. Additionally, it does not support multicurrency processing or international payments, which could be crucial for international eCommerce operations.

If your business is focused on local markets and does not require advanced customization, Fulton offers a solid and trustworthy solution. Businesses that anticipate rapid growth or global expansion may need to explore alternatives with broader feature sets.

Evaluating the Value: Pros and Cons

Fulton Merchant Card Services delivers value through reliability, relationship-driven service, and seamless banking integration. It’s particularly beneficial for current Fulton Bank customers or businesses that operate within the bank’s regional footprint. The availability of in-person support and dedicated account managers adds to its appeal for companies that prefer personalized service. On the other hand, the platform lacks transparency in pricing, does not support real-time innovations like AI-based analytics, and offers limited scalability for global operations. The absence of advanced customization tools and integration options may be limiting for tech-driven businesses.

Still, for those looking for a grounded and well-supported solution with essential payment features, Fulton is a dependable partner. It’s best suited for businesses that want consistency and care over high-speed innovation or deep technical flexibility.

Frequently Asked Questions

Is Fulton Merchant Card Services suitable for high-risk businesses?

No, Fulton primarily serves low to moderate-risk industries. High-risk sectors like CBD, gambling, or adult services should consider processors specializing in those areas.

Can existing POS hardware be used with Fulton’s system?

It depends on the hardware’s compatibility. Some terminals may be supported, but it’s best to confirm with Fulton before integrating existing equipment.

How fast are payouts processed?

Standard payouts typically take one to two business days. Same-day funding may be available but could involve additional fees or account setup requirements.

Forte Payment Systems Review

By 10topmerchantservices May 27, 2025

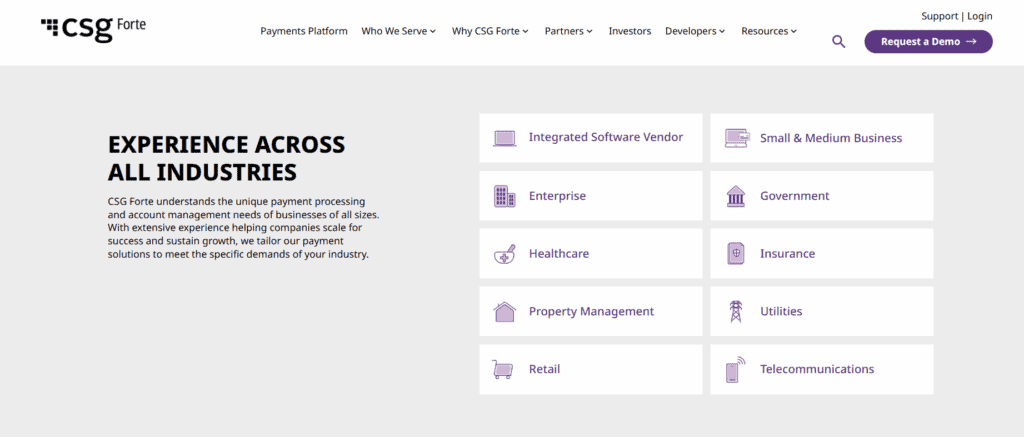

Forte Payment Systems is a United States-based payment processor that serves sectors like government, utilities, healthcare, and professional services. It was founded in 1998 and became part of CSG in 2018. Over time, Forte has positioned itself as a secure, cloud-based platform focused on compliance and recurring billing. Its services are not tailored for traditional retail or fast-moving e-commerce. Instead, they support more structured billing environments that demand accuracy, security, and reliability. Lets read more about Forte Payment Systems Review.

Web portals, mobile applications, call centres, and in-person setups are among the various payment environments that the platform supports. Because of its scalable infrastructure, medium-sized to large businesses can use it. Forte provides digital invoicing, tokenisation, integration-ready APIs, and payment processing for both ACH and card-based transactions. Businesses can incorporate payment features into their own systems with the help of these tools. Forte’s model is still a strong option for companies with complex compliance and integration requirements, even though it might not be appropriate for smaller businesses seeking quick setups.

Core Features and Payment Capabilities | Forte Payment Systems Review

Forte provides a unified platform capable of processing ACH, credit card, debit card, eCheck, and contactless payments. A key benefit is the ability to manage both one-time and recurring payments across multiple channels, including web, mobile, and in-person systems. This flexibility supports various business models and operational workflows.

ACH transactions are a foundational feature, making Forte ideal for sectors like healthcare, education, and utilities. These transfers are often less expensive than card payments and work well for businesses managing high volumes of scheduled transactions. Forte’s platform also supports real-time card processing with tools for refunds, chargebacks, and reconciliation.

The system includes digital wallet compatibility with Apple Pay and Google Pay. Tokenization ensures customer payment information is stored securely, reducing the risk associated with repeat transactions. Automatic invoice generation and payment reminders add to the convenience, helping businesses streamline receivables. Fraud prevention and account verification tools can be added to further secure the payment cycle, making Forte a well-rounded solution for complex payment environments.

Virtual Terminal and Mobile Functionality

Forte offers a browser-based virtual terminal that eliminates the need for traditional point-of-sale hardware. This tool is well-suited for service-based businesses, remote teams, and call centers. Payment details can be entered manually, refunds issued, and recurring payments scheduled within a centralized interface. Customer information can also be stored securely for future use.

The terminal integrates with Forte’s vault and billing features and accepts both card and ACH payments. Although the interface works, new users might need some initial assistance to properly utilise its features. Once configured, the terminal offers a simple method of handling transactions without the need for additional equipment.

Regarding mobile devices, Forte facilitates payment processing via specialised apps for tablets and smartphones. These applications, which are compatible with card readers, offer functions like customer lookup, transaction history access, and receipt issuance. The mobile tools are suitable for field service providers and professionals who are constantly on the go, even though they are not made for retail-style point-of-sale setups. Forte’s ability to provide a single payment environment is strengthened by the uniformity across web, terminal, and mobile channels.

Developer Tools and API Integration

Forte stands out for its developer-friendly approach, offering well-documented RESTful APIs for businesses that want deep integration. These APIs allow payments to be embedded into websites, mobile apps, or custom software platforms. This capability is especially useful for software vendors and businesses aiming to provide a branded, end-to-end payment experience.

The documentation is detailed and includes examples for common tasks such as initiating transactions, handling refunds, setting up recurring billing, and managing webhook notifications. Developers also gain access to a sandbox environment for testing and refinement before going live. This reduces deployment risks and shortens the go-to-market timeline.

Security is built in through client-side encryption and tokenization, allowing safe data transmission. Forte also offers SDKs in multiple programming languages, including JavaScript, .NET, and PHP. The modular API structure lets businesses use only the services they need. For companies with limited technical expertise, the virtual terminal or hosted checkout pages may serve as more accessible options. But for businesses that prioritize custom workflows, Forte’s API toolkit is a major asset.

Security and Compliance Capabilities

Security and regulatory compliance are key elements of Forte’s design. The platform is PCI-DSS Level 1 certified, ensuring that payment processing meets the highest security benchmarks in the industry. Sensitive cardholder data is replaced with secure tokens, allowing repeat transactions without exposing raw data. This protects customers while enabling seamless billing.

Advanced fraud detection tools from Forte can notify companies of suspicious activity. Businesses in industries with a lot of regulatory oversight, like public administration and healthcare, need these tools. Along with tools like OFAC screening to satisfy legal requirements, the system also supports NACHA compliance for ACH payments.

AVS, CVV checks, and velocity controls are examples of optional security features. The platform helps businesses keep compliance records and transparency by recording every transaction activity for audit and reporting purposes. Although casual merchants may not need this level of security, it is essential for businesses where data protection and legal compliance are top priorities.

Pricing Approach and Cost Considerations

Forte does not publish a standard pricing list. Its costs are generally customized depending on industry, transaction volume, feature selection, and risk profile. While this allows tailored pricing for large enterprises, it creates uncertainty for smaller businesses that prefer flat-rate, transparent costs.

Fees may include per-transaction charges for ACH and card payments, along with monthly gateway or statement fees. Services like account validation, fraud detection, or expedited funding may carry additional charges. ACH pricing tends to be cost-efficient and predictable, especially for businesses with steady recurring billing needs.

Sales representatives typically prepare quotes after reviewing a prospective client’s operations. This consultative approach helps match features with budget, but it may delay the onboarding process for companies looking to make fast decisions. Some users have noted unexpected fees tied to support or configuration changes, though many of these can be negotiated at the outset. For businesses that prioritize customized payment setups, the flexible pricing may be worth the initial effort.

Industry Applications and Fit

Serving sectors that demand strict adherence to regulations and enduring billing partnerships is where Forte excels. Governmental organisations that manage taxes and permits, healthcare organisations that handle patient payments, and utilities that handle recurring bills are examples of common use cases. Forte’s tools for tuition, donations, and membership dues are also advantageous to nonprofit organisations and educational institutions.

Forte is an excellent choice for any industry where automation and security are crucial due to its ACH capabilities and billing tools. The platform facilitates the smooth transfer of data between payment processing and essential business applications by allowing integration with third-party systems. Errors and administrative burden are decreased as a result.

Businesses that rely on real-time consumer transactions, such as retail or restaurants, may find Forte less suitable. The platform does not emphasize visual interfaces or modern point-of-sale hardware. However, service-based companies, software vendors, and B2B providers may appreciate Forte’s flexible backend and developer options. The platform’s true value lies in environments where compliance, repeat billing, and security take precedence over simplicity.

Reporting and Analytics Capabilities

Forte offers robust reporting and analytics tools designed to support financial transparency and operational decision-making. The platform’s dashboard provides real-time visibility into transaction activity, allowing users to filter results by payment type, status, or customer profile. These tools are especially useful for organizations managing complex accounts or regulatory reporting.

Reports can be customized and scheduled for automatic delivery. They are exportable in multiple formats, including CSV and PDF, making them easy to integrate with accounting systems or enterprise software. Batch summaries, settlement reports, and historical logs help teams reconcile accounts efficiently and catch discrepancies early.

Forte’s analytics focus more on transaction clarity than consumer insights. While it lacks marketing data features, it excels at providing dependable financial records. This is a plus for finance teams, auditors, and business leaders who need detailed visibility into revenue and reconciliation. Though the interface may not have the polish of newer platforms, its depth and reliability make it a practical choice for financial oversight.

Customer Support and User Onboarding

Forte offers multi-channel support via phone, email, and an online portal. Support responsiveness is generally favorable, particularly for clients with custom setups or advanced integration needs. Onboarding usually includes assistance with configuration, API keys, and optional user training. New users also get access to a comprehensive documentation hub.

A dedicated account manager may be assigned to larger clients to assist with strategy, execution, and expansion. When companies have continuous operational updates or technical enquiries, this point of contact becomes crucial. For specialised issues, however, businesses without designated representatives might have to wait longer for responses.

Forte could do better in the area of after-hours support, for example. For businesses that are open 24/7, the standard service window may be restrictive. Nonetheless, Forte offers a reliable experience for businesses that value methodical onboarding and technical assistance based on procedures and documentation. Its support system fits in nicely with the type of customers it draws in; those who appreciate accuracy and dependability.

Final Verdict: Strengths and Suitability

For businesses with recurring billing requirements and a focus on compliance, Forte Payment Systems is a robust payment processor. It offers flexible API-based integrations, secure architecture, and robust ACH processing. Forte’s capabilities are probably most useful to government organisations, utilities, nonprofits, and healthcare providers.

The platform is perfect for medium-sized to large businesses with internal IT resources because of its modular design, robust security posture, and advanced reporting. For small businesses or those seeking public pricing and quick setup, it might be too complicated. For businesses that prioritise visual interfaces, its emphasis on functionality over aesthetics could also be a disadvantage.

In summary, Forte excels in environments where control, customization, and compliance are essential. It is not built for plug-and-play simplicity but rather for businesses seeking a long-term, scalable payment solution with room to adapt and grow.

FAQs

Q1: Is Forte Payment Systems suitable for small businesses?

Forte can support small businesses, but its complexity and feature depth are better suited to mid-sized and large organizations with specific compliance or recurring billing needs.

Q2: Does Forte offer recurring billing and invoicing tools?

Yes, Forte has strong capabilities for recurring payments, digital invoicing, and subscription billing. These features are commonly used by service-based and membership-driven organizations.

Q3: How secure is Forte for handling payments?

Forte is PCI-DSS Level 1 compliant and includes tokenization, encryption, and fraud monitoring. It is a secure solution for businesses managing sensitive or regulated financial data.

First Hawaiian Bank Review

By 10topmerchantservices May 23, 2025

Having been established in 1858, First Hawaiian Bank (FHB) is the oldest and most reputable financial institution in Hawaii. With branches in Guam and the Northern Mariana Islands, FHB, which has its headquarters in Honolulu, has gradually expanded its presence throughout the Pacific. Its enduring presence is a testament to its dependability and strong ties to the communities it serves. Lets read more about First Hawaiian Bank Review.

FHB has developed into a full-service banking provider over the years. Services for individuals, families, small businesses, and corporate clients are all included in its portfolio. Despite being a regional bank, FHB has continued to invest in digital infrastructure to meet the demands of modern banking.

Customer relationships are a core strength. The bank regularly receives high satisfaction ratings in its operating regions, which speaks to its ability to blend traditional service values with contemporary banking. While its market reach is smaller compared to national institutions, FHB’s reputation for personal attention and stability remains a cornerstone of its appeal.

Personal Banking Products and Services | First Hawaiian Bank Review

FHB provides a well-rounded range of personal banking products suitable for varying customer needs and life stages. These include checking and savings accounts, money market options, and certificates of deposit. Checking accounts are tiered to serve different customer segments. Students, seniors, and basic users can access low-fee or no-fee options, while interest-bearing accounts are available for those maintaining higher balances. Most checking options include mobile and online banking, debit cards, and ATM access. However, some accounts carry monthly maintenance fees unless balance or activity criteria are met.

Savings products follow a standard tiered interest model. CDs are available with fixed returns over set periods but offer more modest rates compared to online-only competitors. Money market accounts provide better yields for higher balances but come with limited withdrawal flexibility. While the bank’s local ATM and branch access is strong within Hawaii and nearby territories, customers outside these regions may find accessibility limited. For Hawaii-based individuals who value community engagement and local service, FHB remains a practical and trustworthy banking choice.

Business Banking Solutions

FHB offers a diverse suite of business banking services tailored to Hawaii’s unique economic environment. Its offerings serve small businesses, mid-sized enterprises, and larger commercial operations.

Business checking and savings accounts are available in multiple formats to suit varying transaction volumes and cash management needs. These accounts come with digital banking tools like mobile check deposits, account alerts, and online bill payments. Fee structures are competitive, with waivers offered based on maintaining specific balance thresholds.

The bank offers term loans, equipment loans, business credit lines, and financing for commercial real estate. One clear benefit is that these products are run by teams that understand the island economy, which helps businesses deal with issues unique to the area.

Retail and service-based businesses can access merchant services like card processing and point-of-sale systems. FHB offers dependable payroll and treasury services, despite the fact that some digital tools might not be as advanced as fintech rivals. The bank’s relationship banking model is where it really shines. Working with experts who have firsthand knowledge of the local economy is often advantageous to local business owners. In an area where national providers might be lacking in context or adaptability, this individualised approach offers value.

Mortgage and Loan Offerings

FHB provides a comprehensive set of lending options, including home loans, personal loans, auto loans, and personal lines of credit. These products are structured to reflect Hawaii’s unique real estate dynamics and consumer needs. Mortgage offerings include fixed and adjustable-rate options, along with government-backed FHA and VA loans. Refinance and home equity lines of credit are also available. Rates are competitive locally, though they may not always align with those from online lenders operating at scale.

The mortgage application process is supported by both online tools and in-person guidance, which benefits first-time homebuyers or customers seeking clarity. Prequalification can be done digitally, but the bank continues to prioritize face-to-face service. Auto loans are available for both new and used vehicles, with flexible repayment terms and reasonable interest rates. While competitive in the local market, customers may want to compare national offers for the best possible deal.

Personal loans and lines of credit are designed for flexible use cases like debt consolidation or emergency expenses. These generally come with fixed or variable rates and do not always require collateral. Overall, FHB’s lending suite is practical, community-focused, and suited to those who prioritize service and support over chasing the absolute lowest rate.

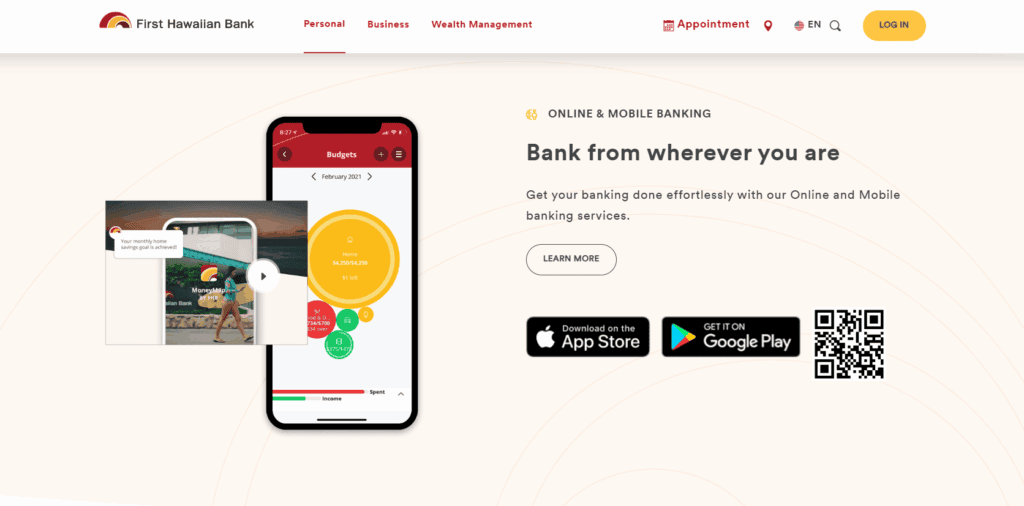

Digital Banking and Mobile App Experience

Significant progress has been made by First Hawaiian Bank in developing its digital capabilities. Although it doesn’t have as many features as major national banks and fintech startups, its mobile app and online banking platform do a good job of covering the essentials. Users of the FHB mobile app can pay bills, view balances, deposit checks, send peer-to-peer payments through Zelle, and transfer money. Additionally, customers can review statements and set up account alerts. Despite the interface’s ease of use, some users have complained about sluggish performance or trouble logging in during updates.

In addition to adding basic tools for managing accounts and tracking expenses, the online banking platform reflects the majority of app functionalities. The system lacks advanced budgeting tools and AI-driven financial insights, despite using encryption and contemporary security protocols. The app supports biometric login and two-factor authentication, contributing to overall account safety. Reviews on app stores are generally positive but indicate occasional reliability concerns.

For everyday banking needs, FHB’s digital tools are sufficient. However, users looking for robust financial management capabilities or tech innovation may find the experience a bit underwhelming.

Investment and Wealth Management Services

Through its subsidiary First Hawaiian Advisors, the bank offers investment and wealth management services tailored to individuals with varying financial goals. This includes options like mutual funds, IRAs, stocks, bonds, and annuities. Advisors at FHB provide personalized financial strategies, including retirement planning, estate services, and trust management. High-net-worth clients can access more comprehensive planning services, including multi- generational wealth transfer.

One of the firm’s key differentiators is its relationship-oriented model. Advisors tend to maintain long-term connections with clients and offer localized expertise in tax strategies and investment planning. This approach suits clients who value personalized attention over digital automation. However, the range of investment options is narrower compared to large national brokerage firms. Fees may also be higher for smaller accounts, and the platform lacks the cost-efficiency of self-managed online tools.

Still, for customers who prefer face-to-face interactions and customized advice rooted in local economic understanding, First Hawaiian Advisors offers a dependable and professional service experience.

Customer Service and Support

First Hawaiian Bank excels at providing excellent customer service, particularly in Hawaii. The bank’s branch-level service and community involvement reflect its strong emphasis on interpersonal relationships. Staff members who take the time to explain banking products, help with complicated problems, and establish a rapport with loyal customers are generally praised for their in-branch service. Customers who are older or less accustomed to using digital tools will particularly benefit from this.

For basic questions, live chat is available, and phone support is available during extended business hours. Even though representatives are usually polite and helpful, more complicated problems might need to be escalated or followed up on. The bank also provides secure messaging through its online platform and a helpful FAQ section. While functional, these digital support tools lack the immediacy of 24/7 assistance offered by some national players.

One standout feature is FHB’s multilingual support and accessible services for customers with disabilities, including large-print materials and accessible branches. Overall, FHB delivers solid customer support rooted in local understanding and cultural sensitivity, even if it doesn’t offer the speed or scale of larger competitors.

Fees, Charges, and Transparency

Like many regional banks, First Hawaiian Bank charges fees on certain account types and services, though there are ways to minimize them through balance thresholds or account activity. Personal checking and savings accounts may incur monthly maintenance fees ranging from $3 to $15. These fees can typically be waived by maintaining a minimum balance or setting up direct deposits. While this is standard among traditional banks, it may feel outdated compared to the no-fee structures of many digital banks.

Other common charges include out-of-network ATM fees, overdraft fees, and wire transfer charges. The bank provides overdraft protection, but it requires customer enrollment and understanding of the terms. FHB publishes its fee schedules online, and the disclosures are clear, though not always easy to find. Transparency could be improved by making pricing information more accessible upfront.

Business accounts also come with activity-based fees that can vary depending on transaction volume. In some cases, customers have noted the need to actively request fee waivers. In summary, FHB’s fees are on par with regional bank standards. Customers should review terms carefully to avoid unexpected charges, especially when comparing options with online or national banks.

Security, Fraud Protection, and Compliance

In its banking operations, FHB places a strong emphasis on compliance and safety. Depositors are protected up to $250,000 per eligible account category by this FDIC-insured institution. For digital security, the bank uses a variety of industry-standard techniques. These consist of session timeouts, fraud monitoring systems, encrypted sessions, and two-factor authentication. Mobile devices can support biometric logins, and users can use the app to immediately freeze their cards.

FHB has a spotless compliance history and hasn’t had any significant regulatory problems recently. Its cautious approach helps to build a reputation for reliability and caution. Its website also offers educational materials on cybersecurity, identity theft, and phishing. Clients who are unfamiliar with online banking or who require reassurance regarding digital threats may find this advice especially helpful.

While not known for leading-edge security innovations, FHB offers a robust, traditional model that prioritizes safety and compliance, particularly suited to customers seeking stability over experimentation.

Pros, Cons, and Final Verdict

First Hawaiian Bank delivers a strong regional banking experience, characterized by deep community engagement, solid financial products, and reliable customer service. Its key strengths include:

A wide range of personal and business services

Strong in-person support

Deep understanding of the local economy

Personalized wealth management and advisory

However, the bank also faces a few challenges:

Limited geographic footprint

Modest digital capabilities

Standard fees that may be higher than online-only banks

FHB is an excellent choice for residents of Hawaii, Guam, or CNMI who prioritize trust, community connection, and personalized service. It may be less ideal for digital-first users or those seeking the lowest-cost options nationwide. For what it is; a regionally focused institution with a long-standing presence; FHB stands out as a dependable and community-oriented bank.

FAQs

Q1: Does First Hawaiian Bank offer nationwide banking services?

No, FHB operates branches in Hawaii, Guam, and the Northern Mariana Islands. However, digital banking access is available nationwide.

Q2: Is First Hawaiian Bank FDIC insured?

Yes, FHB is FDIC insured. Eligible deposits are protected up to $250,000 per depositor, per account type.

Q3: How does FHB compare to larger national banks?

FHB provides stronger regional service and customer relationships but may not match national banks in technology or geographic coverage.

Fattmerchant Review: Transparent Payments with a Modern Edge

By 10topmerchantservices May 20, 2025

Fattmerchant, now rebranded as Stax, entered the payments industry in 2014 with a mission to challenge the norm. Its approach was simple yet disruptive: replace confusing percentage-based markups with flat-rate subscription pricing. This pricing shift helped bring clarity to how businesses manage transaction costs and brought renewed attention to interchange-plus models. Lets read more about Fattmerchant Review.

Reducing transaction fee unpredictability was central to the company’s vision. Fattmerchant made it possible for expanding companies to better predict costs by providing direct access to wholesale interchange rates and imposing a fixed monthly fee. Higher processing volume businesses were especially drawn to this model.

Many users still refer to it as Fattmerchant because of its early industry impact, even though it is now officially Stax. ACH transfers, analytics, invoicing, mobile payments, and real-time reporting are just a few of the comprehensive payment features that the platform has added over time. To assist you in deciding whether Fattmerchant’s offering is appropriate for your company, this review delves deeply into each of its features.

Core Features and Capabilities | Fattmerchant Review

Fattmerchant provides a complete range of tools to handle various payment types. At its foundation, it supports credit and debit card processing, mobile transactions, ACH transfers, and e-commerce payments; all within a unified software interface. This all-in-one setup streamlines operations for businesses managing payments across several touchpoints.

Its virtual terminal stands out as a practical feature, allowing users to accept payments through any browser. This is especially useful for businesses that operate remotely or provide services off-site. Invoicing tools are also included, with options for recurring billing and automatic reminders that are ideal for subscription-based models.

The dashboard provides real-time insight into transactions, customer activity, and cash flow trends. Users can generate reports and monitor business performance without relying on external analytics software. It also integrates with accounting tools like QuickBooks to automate data syncing and simplify reconciliation.

For mobile needs, the app and Bluetooth-enabled card readers help businesses accept payments on-the-go. Altogether, the platform supports omnichannel sales while keeping everything accessible through a single dashboard.

Subscription-Based Pricing Structure

Fattmerchant’s flat-fee subscription pricing is what makes it unique. It passes interchange costs straight from card networks and charges a fixed monthly rate rather than adding extra fees to each transaction. The unexpected costs associated with traditional processors are eliminated with this configuration. For example, a business pays a flat monthly subscription and only the direct interchange fees, rather than a per-transaction rate such as 2.9 percent plus 30 cents. Because monthly fees remain the same regardless of processing activity, the cost savings can be substantial for companies with high transaction volumes.

There are several price tiers according to business type and volume. Enterprise solutions serve high-volume operations, while entry-level plans are available to smaller businesses. It’s important to remember that this model benefits those who process regularly and at scale. For lower-volume businesses, the monthly cost might outweigh the savings from reduced transaction fees.

Other potential costs may include hardware rentals, premium features, or gateway access, which should be factored in when evaluating total value.

Omnichannel Payment Functionality

Fattmerchant supports multiple payment environments, making it a good option for businesses selling across channels. Whether accepting payments in-store, online, or via mobile, the platform ensures consistent user experiences and unified reporting. For physical retail, Fattmerchant works with terminals that are EMV and contactless payment enabled. These devices provide a secure way to accept chip cards and mobile wallets. Businesses can also deploy full POS systems for added functionality like inventory and staff management.

Online, users can create hosted payment pages, send payment links via email or SMS, and integrate with popular e-commerce platforms. An API is available for businesses building custom payment solutions. These capabilities support digital-first operations, service-based businesses, and remote sales alike. Mobile acceptance is equally strong. The Bluetooth reader and app combination enables payments from anywhere, helping tradespeople, delivery services, or pop-up stores stay flexible.

All transaction data from each channel feeds into one dashboard, making reconciliation easier and performance tracking more accurate.

Backend Software and Integrations

Fattmerchant provides cloud-based software that combines reporting, analytics, invoicing, and payments under the Stax brand. Users can access their data from any internet-connected device, and no installation is required. Users can quickly access transaction summaries, customer behaviour patterns, and sales trends thanks to the dashboard’s ease of use. Businesses can use this data to make well-informed decisions without having to buy additional analytics software.

One major advantage is integration with QuickBooks. By automatically syncing payment data with the accounting system, it minimises the need for manual entry and the possibility of reconciliation errors. This is especially useful for businesses that handle a lot of transactions. Additionally, Fattmerchant integrates payment tools with CRMs, inventory management systems, and custom applications through APIs and third-party platforms. While the integrations cover essential business needs, advanced users may need technical support for custom workflows or less common platforms.

Hardware and Point-of-Sale Equipment

Fattmerchant provides hardware options to meet a range of operational needs. This includes traditional countertop terminals, wireless devices, and mobile card readers that support contactless and chip card transactions. Retail locations can opt for familiar brands like Verifone or Clover, which pair with Fattmerchant’s backend to create a seamless checkout experience. These terminals typically include touchscreen functionality, receipt printers, and PIN pads.

For businesses on the move, the mobile card reader and app combo make accepting payments from a smartphone or tablet straightforward. It supports major mobile wallets and meets current security standards. More advanced POS systems are also available for businesses that require inventory tracking, employee management, or detailed customer records. These setups work well in retail, hospitality, or healthcare settings.

Hardware can be purchased or leased, offering flexibility based on budget. Businesses should check for additional fees, as hardware costs are not included in the base subscription.

Customer Service and Onboarding

An important factor in Fattmerchant’s appeal is customer service. During business hours, the company provides assistance by phone, chat, and email. The support staff is often praised by users for being responsive and helpful, especially during onboarding. Usually, a representative is assigned to new customers to help them with setup. The onboarding procedure is made to minimise hiccups and guarantee a seamless transition, from setting up terminals to connecting accounting software.

Additionally, the dashboard interface is easy to use. It organises features into sections with clear labels, which makes managing transactions, producing reports, and creating invoices simple. The learning curve is lowered by this simplicity, particularly for small teams or entrepreneurs without technical know-how. Some users have noted longer response times during peak hours and limited support over weekends, depending on the service plan. Even so, overall feedback on user experience remains positive.

Compliance and Data Security

Fattmerchant complies with PCI standards to protect customer payment data. Its systems use encryption and tokenization to ensure transactions are processed securely, whether online, in-store, or through mobile devices. Security protocols protect data in transit and at rest, helping reduce the risk of data breaches. Fattmerchant also offers compliance assistance, including self-assessment guides and resources to help merchants stay up to date with regulations.

Fraud prevention tools like AVS support and transaction velocity checks are built into the platform. While these basic tools are effective for most businesses, those operating in high-risk categories may require more advanced fraud detection systems, potentially through third-party solutions. Merchants should routinely monitor their security practices and update their compliance documentation to stay protected.

Who Benefits Most from Fattmerchant?

For small to medium-sized businesses that handle a lot of transactions or a regular volume, Fattmerchant is perfect. For businesses that want to lower transaction fees without compromising tool access, the flat monthly fee makes the most sense. The platform’s integrated features will be beneficial to companies in the retail, healthcare, legal, home services, and digital product sectors. Those who use omnichannel sales tactics or recurring billing will find it especially useful.

However, the fixed subscription model might not be as advantageous for seasonal or low-volume businesses. The potential savings from lower transaction fees might be outweighed by the upfront monthly cost. A pay-as-you-go processor might be more suitable in these situations. Tech-oriented businesses may unlock more value through Fattmerchant’s APIs, while non-technical users can still enjoy its straightforward design and usability.

Key Pros and Cons

Fattmerchant delivers a strong mix of transparent pricing and integrated features. It’s designed for businesses that want control, clarity, and a unified platform.

Advantages:

Flat monthly pricing with direct access to interchange rates

Support for in-person, online, and mobile payments in one system

QuickBooks integration and real-time reporting tools

Responsive customer service and personalized onboarding

Easy-to-use software with minimal learning curve

Considerations:

Not cost-effective for businesses with low monthly sales

Some advanced features or integrations may require extra setup or fees

Limited weekend support for some plans

For businesses that meet the right criteria, Fattmerchant offers meaningful savings and operational efficiency.

FAQs

Is Fattmerchant now Stax?

Yes. Fattmerchant rebranded as Stax, but many users still use the original name. The platform, pricing model, and features remain consistent.

Are there long-term contracts with Fattmerchant?

No. Most plans are month-to-month, allowing businesses to cancel at any time without early termination fees.

Can businesses save money using Fattmerchant?

Yes. Companies with high processing volumes often see significant savings compared to traditional per-transaction pricing models.

Epicor Software Review

By 10topmerchantservices May 17, 2025

Epicor Software is a well-established name in the Enterprise Resource Planning space, with its roots going back to 1972. Based in Austin, Texas, the company has built a reputation for delivering ERP solutions that cater specifically to the needs of industries like manufacturing, distribution, retail, and professional services. Over the years, Epicor has evolved from offering legacy systems to launching cloud-ready, modern platforms, with Epicor Kinetic currently at the forefront. Lets read more about Epicor Software Review.

What distinguishes Epicor is its emphasis on depth rather than breadth. Instead of providing a generic platform, Epicor incorporates customized features into its ERP solutions for specific industries. This focused method assists companies in intricate industries like discrete manufacturing and supply chain management in overseeing compliance, resources, and workflows more efficiently.

Epicor has a worldwide presence, catering to over 20,000 clients across more than 150 nations. Its ERP solutions come in both cloud and on-premise formats, offering flexibility according to infrastructure requirements and regulatory conditions. The cloud deployment of Epicor Kinetic is becoming increasingly popular because of reduced initial IT expenses, simpler upgrades, and improved scalability.

Despite its strengths, Epicor’s industry focus sometimes requires expert consulting for setup and configuration, which may increase implementation time. Legacy users might also face challenges transitioning to Kinetic’s modern interface. Still, Epicor remains a reliable choice for organizations seeking ERP software that aligns closely with their operational complexity.

User Interface and Experience | Epicor Software Review

Epicor has made noticeable progress in improving its user interface, particularly with the launch of Epicor Kinetic. This web-based platform offers a more intuitive and responsive experience than previous versions. Its interface is clean and user-friendly, with customizable dashboards and widgets that users can adapt based on their roles and daily tasks.

Navigation is largely seamless, though users familiar with older versions may need some time to adjust to the updated layout. The simplified menu system reduces clutter, and most core functions can be accessed with just a few clicks. Role-based dashboards allow departments to focus on relevant workflows, improving productivity and reducing distractions.

Epicor supports mobile access for teams that need real-time updates outside the office, such as field service staff or warehouse managers. However, the mobile experience still trails behind CRM or sales platforms that prioritize mobile-first design.

Customization is another strong point. Users can adjust KPIs, tweak workflows, and even create apps using low-code tools built into the platform. This gives tech-savvy teams the flexibility to tailor the system to their specific needs.

That said, some older modules within the system still retain a dated look and feel, leading to inconsistencies in the overall user experience. While the interface is moving in the right direction, full modernization is still in progress.

Core ERP Capabilities

Epicor’s ERP suite includes all the standard modules businesses expect; finance, procurement, inventory, production planning, and customer relationship management. Its standout features lie in manufacturing and supply chain management, where Epicor offers tools designed to handle complex operations with precision.

The finance module covers general ledger, accounts payable and receivable, budgeting, and multi-currency capabilities. These tools are tightly integrated with other business processes to ensure seamless financial reporting. Inventory management includes real-time tracking, barcoding, lot control, and location-based inventory views.

In production management, Epicor stands out with its assistance in job scheduling, capacity planning, and material requirements planning. This makes it perfect for producers overseeing intricate product assemblies and floor operations.

Customer and supplier modules provide complete insight into pricing, performance metrics, and communication records. The field service management module assists companies that offer maintenance or support, featuring tools intended to handle service requests and equipment documentation.

Another major strength is the consistency of data across modules. Changes implemented in one section are immediately visible in other areas, reducing mistakes and redundancies. Nevertheless, fully utilizing the potential of these tools often demands considerable training and setup. Organizations lacking internal ERP expertise may find it challenging to harness the platform’s complete capabilities.

Industry-Specific Solutions

Epicor’s deep commitment to industry-specific ERP is a major differentiator. Instead of forcing businesses to adapt to generic systems, Epicor delivers pre-configured solutions tailored to the operational needs of industries like manufacturing, distribution, retail, automotive, and building supply.

In manufacturing, Epicor supports both discrete and process production, along with hybrid operations. Features such as advanced scheduling, quality control, and compliance tracking are built into the system. For distributors, the ERP focuses on warehouse coordination, logistics, and inventory forecasting.

Retailers benefit from centralized pricing, POS integration, and real-time inventory synchronization across locations. Automotive businesses get features like part tracking, warranty management, and supplier portal integration. These configurations use industry-specific language and processes, reducing the need for heavy customization.

Industry-specific compliance tools also add value. For instance, manufacturers in regulated industries can manage traceability and documentation requirements more efficiently. These built-in capabilities help businesses avoid relying on third-party systems or workarounds.

However, this vertical focus can also lead to feature silos. Capabilities developed for one industry might not work well in another, which could limit flexibility for businesses with operations in multiple sectors. Still, for companies operating within Epicor’s targeted verticals, the benefits of a purpose-built ERP are significant.

Deployment Options and Cloud Strategy

Epicor offers a range of deployment models, including on-premise, cloud, and hybrid environments. This flexibility accommodates a wide variety of business needs, from companies with legacy infrastructure to those prioritizing digital transformation.

Epicor Kinetic is at the heart of its cloud strategy. Developed on Microsoft Azure, Kinetic offers browser-based accessibility, automated updates, and lowered IT costs. Companies gain advantages from scalability, robust infrastructure, and the capability to access the system remotely.

Epicor still provides the option for organizations that choose or need on-premise systems. Such implementations are typical in industries that have stringent data governance regulations or prior IT expenditures. Hybrid models are also offered, allowing a gradual transition to the cloud.

A key benefit of the platform is its modular nature. Businesses can begin with a handful of features and grow as required, facilitating gradual rollout and reducing upfront costs. The cloud model further encompasses uptime assurances and performance enhancement via service level agreements.

While cloud deployment simplifies maintenance, migrating from legacy systems requires careful planning. Businesses must consider data transfer, employee training, and process adjustments. Despite these challenges, Epicor’s flexible deployment strategy makes it adaptable for a broad range of operational environments.

Integration and Compatibility

Integration is a critical component of ERP success, and Epicor provides strong tools in this area. The platform supports RESTful APIs that enable real-time data sharing with third-party applications, including CRM, HR, e-commerce, and business intelligence tools.

Epicor Kinetic has been designed with open architecture in mind. Its Integration Cloud platform supports both out-of-the-box and custom connectors, allowing businesses to link with tools such as Salesforce, Microsoft Power BI, and Shopify.

Legacy system compatibility is another area of focus. Epicor includes middleware and transformation tools to support data migration and dual-system operations, which is helpful for businesses gradually phasing in new modules.

Internally, all core modules are fully integrated. This ensures consistent data across departments, enhancing reporting accuracy and operational coordination. For example, updates in finance automatically reflect in inventory or procurement modules.

However, integrating Epicor with highly customized software may require technical assistance. The APIs are capable but not always easy for non-technical users to manage. Small businesses without IT resources may need to rely on external consultants for more complex integrations.

Overall, Epicor’s integration capabilities are robust, especially within the Kinetic ecosystem. Its architecture supports both flexibility and structure, enabling businesses to create cohesive software environments.

Reporting, Analytics, and BI Tools

Epicor prioritizes analytics and reporting, acknowledging that immediate data is crucial for making strategic decisions. The system features a diverse array of pre-designed reports covering areas such as finance, inventory, and production.

Epicor Kinetic enhances reporting through interactive dashboards that showcase essential metrics in real time. These dashboards are tailored to specific roles and are user-friendly, allowing individuals to examine data without needing extensive technical expertise. Reports can be tailored and set up for routine distribution.

The platform additionally allows integration with Microsoft Power BI, providing enhanced visualization and data modeling features. Companies can utilize these tools for predicting outcomes, analyzing performance, and planning finances.

For businesses with specific inventory or supply chain needs, Epicor’s Smart Inventory Planning and Optimization suite provides enhanced forecasting tools. Users can create ad hoc reports with drag-and-drop tools, though some training is recommended to maximize this feature.

Initial setup can be time-consuming, especially for organizations unfamiliar with Epicor’s data structure. However, once configured, the analytics tools are powerful and adaptable, supporting a wide range of business intelligence objectives.

Security, Compliance, and Data Management

Epicor incorporates a comprehensive set of features designed to meet modern security and compliance standards. Whether deployed in the cloud or on-premise, Epicor uses role-based access controls to limit system access based on user roles and responsibilities.

The Kinetic platform benefits from Microsoft Azure’s security infrastructure, which includes encryption, firewalls, and continuous monitoring. All data is encrypted in transit and at rest, ensuring strong protection against cyber threats.

Audit trails are built into the platform, making it easier for businesses to track system changes and maintain accountability. Epicor also includes support for global compliance standards, such as GDPR, HIPAA, and SOX. Built-in tools help manage document control, data retention, and user authentication.

Cloud deployments include daily backups and failover protocols, with options for region-specific data hosting. On-premise users can configure backup policies according to their internal protocols.

While Epicor provides the foundation for secure operations, each business must implement additional controls based on its unique risk profile. The tools are available, but proactive governance is essential to maintaining security and compliance.

Customer Support and Training

Epicor provides a multi-layered support system that includes a self-service portal, technical assistance, and structured training programs. Customers can access help through a centralized portal that offers ticket submission, knowledge base resources, and resolution tracking.

Phone and email support are also available, with service quality depending on the level of support purchased. Epicor offers onboarding help, including training sessions, webinars, and access to the Epicor Learning Center, where users can take tutorials and earn certifications.

Community forums and user groups provide an additional level of assistance. Users are able to exchange insights, resolve problems, and explore best practices. These peer networks are often useful for addressing specific challenges or enhancing configurations.

Nonetheless, response durations and problem-solving may differ. Although important issues tend to be addressed first, minor or intricate problems might require more time to resolve. In certain situations, premium support levels are necessary for quicker assistance or expert guidance. In general, Epicor’s support system is robust, particularly for businesses that prioritize education and utilize all accessible resources. The quality of support might still differ based on the type of issue and the availability of consultants.

Pricing and Licensing Structure

Epicor’s pricing is based on several factors, including deployment type, modules selected, user count, and customization requirements. Although the company does not list fixed pricing publicly, it typically uses a modular structure, allowing customers to pay for only the features they need.

For cloud deployments, pricing operates on a subscription model and generally covers updates, support, and hosting. On-premise users adhere to a perpetual licensing model, which includes initial software payments and yearly maintenance expenses.

Companies ought to take into account the total cost of ownership, which encompasses implementation, training, integration, and continuous support. Extensive configuration can greatly raise expenses. Even though Epicor is less expensive than certain Tier 1 ERP systems such as SAP, it might still be inaccessible for smaller companies.

In specific areas or sectors, Epicor partners provide pre-set bundles that can simplify implementation and lower expenses. Nonetheless, a comprehensive ROI analysis is advisable before moving forward, especially for companies with intricate requirements or constrained IT capabilities.

Frequently Asked Questions

Q1: Is Epicor suitable for small and mid-sized businesses, or just enterprises?

Epicor is mainly geared toward mid-sized businesses but is scalable enough to serve both smaller firms and large enterprises. Its modular and cloud-based options offer flexibility for growing organizations.

Q2: How long does it take to implement Epicor ERP?

Implementation timelines vary widely, from a few months to over a year. Factors include deployment type, customization scope, and internal readiness. Cloud implementations tend to be faster.

Q3: What makes Epicor different from other ERP systems like SAP or NetSuite?

Epicor’s industry-specific focus, deep manufacturing functionality, and flexible deployment options set it apart. It prioritizes operational alignment over general applicability, which benefits companies with complex processes.

Elavon Payment Processing: A Comprehensive Review

By 10topmerchantservices May 15, 2025