National Bankcard Review

By 10topmerchantservices October 8, 2025

National Bankcard is a well-established name in the U.S. payments industry, known for providing merchant services to small businesses, e-commerce sellers, and larger enterprises seeking secure payment processing. With so many providers competing for attention, merchants often find it difficult to distinguish one from another. National Bankcard has carved out a space for itself by offering a broad portfolio of services that aim to simplify transactions and give businesses the infrastructure needed to accept payments quickly and securely. Lets read more about National Bankcard Review.

This review takes a deeper look at what National Bankcard brings to the table. Instead of focusing on marketing claims, it examines the company’s history, services, pricing, hardware, integrations, and customer support. By weighing strengths and weaknesses, businesses can better understand how National Bankcard compares to other providers and whether its features justify the cost. Transparency, reliability, and flexibility often matter just as much as competitive rates, and this review explores where National Bankcard succeeds and where it leaves room for caution.

Company Overview and Background | National Bankcard Review

National Bankcard has been in the merchant services industry for many years, offering businesses an entry point into the complex world of payment acceptance. The company positions itself as a one-stop provider, helping merchants navigate banking networks and technology without relying on multiple vendors. Its client base includes traditional storefront retailers, restaurants, service-based businesses, and e-commerce companies, demonstrating flexibility across multiple industries.

The payments landscape has changed rapidly over the last decade. Consumers now expect digital wallets, mobile payments, and online checkout options alongside traditional cards. National Bankcard has adapted by expanding beyond countertop terminals into e-commerce gateways and mobile readers. This evolution allows businesses of varying sizes to find a suitable solution, whether they need a reliable terminal for in-store use, a shopping cart integration for online sales, or a mobile reader for payments on the go.

One of the company’s strengths lies in its attempt to bridge traditional reliability with modern demands. While some providers target either startups or large enterprises exclusively, National Bankcard markets itself to a broad spectrum. That wide positioning can be beneficial for businesses seeking flexibility, but it may also mean that highly specialized industries will not find the same level of tailored support as they might with niche providers. Understanding this broad market focus helps frame the evaluation of their specific offerings.

Core Services Offered

At the center of National Bankcard’s business is credit and debit card processing, covering Visa, Mastercard, American Express, and Discover. Alongside this core function, the company provides merchants with check processing, gift card programs, and loyalty solutions. These additional tools are designed to expand revenue streams and improve customer retention.

For physical retailers and restaurants, National Bankcard supplies POS systems and countertop terminals that support high-volume, fast-paced environments. E-commerce businesses gain access to an online gateway with fraud detection, recurring billing, and integrations with popular shopping cart platforms. Meanwhile, mobile service providers and event-based sellers can use portable readers connected to smartphones or tablets.

The company also emphasizes reporting and analytics, offering merchants the ability to track transactions, monitor chargebacks, and identify sales patterns. This breadth of service demonstrates an effort to cover multiple channels rather than specialize in one. While this flexibility is valuable, it can also mean that some tools are functional but not as advanced as those from specialized providers.

Payment Gateway and Online Solutions

E-commerce continues to dominate retail growth, and National Bankcard provides a gateway that connects online merchants to secure processing networks. Features include recurring billing, tokenization for securely storing customer data, and compatibility with major shopping carts. For businesses selling subscriptions, these functions reduce the need for manual invoicing and ensure consistent revenue collection.

Fraud detection measures are also bundled into the gateway. Suspicious transactions can be flagged before final approval, helping merchants minimize chargebacks and losses. Although these tools are standard across the industry, their inclusion ensures that National Bankcard meets basic merchant expectations.

Compatibility with popular platforms such as Shopify, WooCommerce, and Magento is another advantage. While integration may require technical setup or developer assistance in some cases, businesses without in-house IT support may find the process manageable with external help.

The gateway provides solid functionality but does not stand out as a groundbreaking innovation. For businesses with moderate e-commerce needs, it is sufficient. However, enterprises that rely heavily on advanced fraud prevention or specialized subscription tools may find greater value in dedicated e-commerce processors.

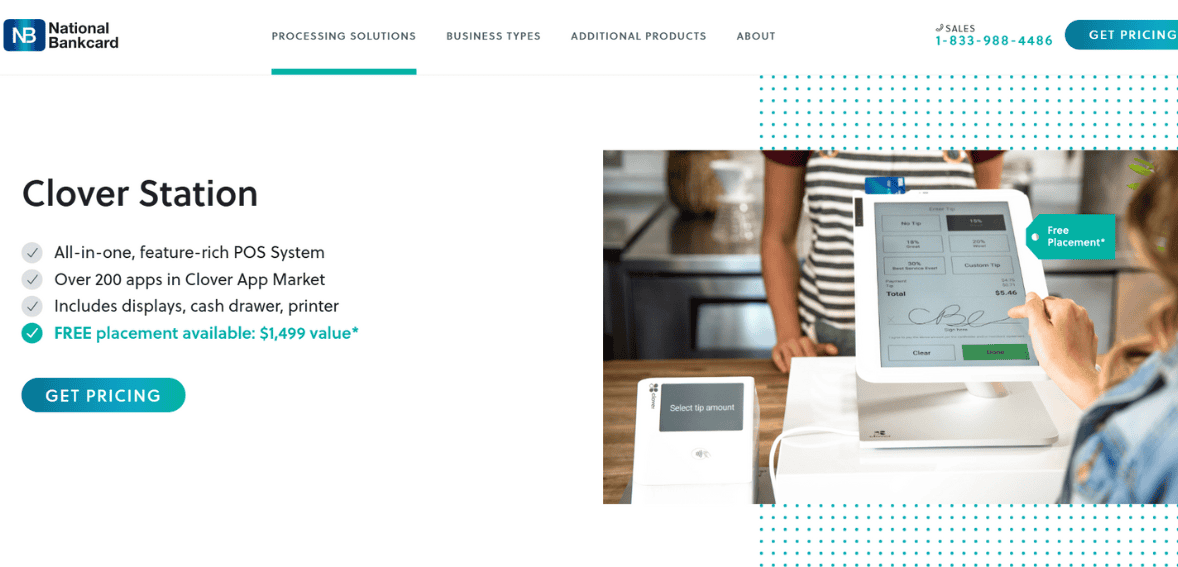

POS Systems and Hardware Options

Point-of-sale systems remain critical for brick-and-mortar businesses, and National Bankcard offers a range of hardware options. Countertop terminals that support magnetic swipe, chip, and contactless payments provide familiar reliability. For more advanced needs, integrated POS systems include inventory management, employee tracking, and sales reporting.

Restaurants can access POS systems designed for order management, table tracking, and tip adjustment. Retailers may prefer systems with barcode scanning and receipt printing. For mobile businesses, wireless terminals and portable readers allow payments to be processed outside of fixed locations.

Hardware reliability is crucial since downtime directly affects revenue. National Bankcard partners with well-known manufacturers, reducing the risk of equipment failure. Still, merchants should clarify warranty policies, replacement terms, and any fees tied to leasing or renting equipment.

While the equipment catalog is comprehensive, competitors increasingly highlight touchscreen smart terminals with advanced features. National Bankcard leans toward proven reliability over innovation, appealing to businesses that prioritize stability over experimentation.

Mobile and Contactless Payments

The rise of mobile wallets and touch-free transactions has changed consumer behavior. National Bankcard provides card readers compatible with smartphones and tablets that accept EMV chips and NFC-based payments such as Apple Pay and Google Pay. These tools are particularly useful for delivery services, repair providers, and vendors at temporary locations.

Merchants also gain access to an app that connects mobile devices to the processing network. Through the app, users can process payments, view basic reports, and issue refunds. While the functionality does not rival advanced mobile POS systems, it covers the essentials for small businesses.

The emphasis on contactless payments reflects shifting consumer expectations. Many customers prefer touch-free checkout for speed and safety, and businesses without NFC capability risk falling behind. National Bankcard’s support in this area ensures merchants can remain competitive, even if the mobile ecosystem does not yet rival the advanced offerings of fintech-driven platforms.

Pricing and Fees Structure

Pricing remains one of the most important and contentious aspects of any payment processor. National Bankcard, like many traditional providers, does not list standardized rates publicly. Instead, fees often depend on business type, volume, and perceived risk. Merchants may encounter tiered pricing or, in some cases, interchange-plus models depending on negotiations.

Common charges include transaction fees, monthly account fees, PCI compliance costs, and gateway fees for online processing. Some merchants have reported contracts with early termination penalties, a factor that can complicate switching providers if dissatisfaction arises. This lack of transparency can frustrate smaller merchants who prefer predictable costs.

On the positive side, larger businesses that process higher volumes may be able to negotiate significantly lower transaction rates. Equipment placement programs sometimes reduce upfront hardware costs, though they may involve recurring leasing expenses.

The main takeaway is that pricing is highly variable. Merchants should request detailed contract terms, confirm whether interchange-plus pricing is available, and clarify early termination policies before signing. Evaluating total costs over the length of a contract is essential to avoid unexpected expenses.

Security and Compliance

Protecting customer data is a non-negotiable requirement in payment processing. National Bankcard aligns with PCI DSS standards, ensuring merchants follow the rules established by the Payment Card Industry Security Standards Council. Encryption and tokenization tools secure sensitive data and reduce risks of breaches.

Fraud prevention measures include filters, alerts, and chargeback management tools that allow businesses to dispute transactions effectively. For online sellers, support for AVS (address verification) and CVV checks adds another safeguard against unauthorized card use.

While these features meet industry expectations, they do not necessarily distinguish National Bankcard from competitors. Still, the company provides the baseline protections merchants should expect, ensuring compliance and risk reduction. Businesses with higher risk profiles may still need specialized fraud solutions layered on top of what National Bankcard offers.

Integrations and API Support

Smooth integrations are crucial for businesses that rely on multiple software systems. National Bankcard provides APIs for connecting payment processing to third-party platforms such as shopping carts, accounting software, and CRM systems. Automating these data flows reduces manual bookkeeping, improves accuracy, and enhances customer management.

For example, linking sales data directly into accounting software eliminates time-consuming reconciliations. Integration with CRM systems allows customer loyalty and purchase history to be tracked seamlessly. National Bankcard’s plug-and-play compatibility with Shopify and WooCommerce is useful for e-commerce merchants who want straightforward setups.

However, businesses with highly technical needs or custom workflows may find the available integrations limited. While the documentation supports flexibility, developer assistance may be required for advanced implementations. For most small-to-medium-sized merchants, the integration support is adequate, but it may not satisfy enterprise-level requirements.

Customer Support and Reliability

Customer support quality often determines whether a payment processor becomes a long-term partner or a short-term experiment. National Bankcard provides phone, email, and in some cases live chat support. Availability is marketed as round-the-clock, though merchant experiences vary. Some report quick, helpful responses, while others describe delays in issue resolution, particularly around billing disputes.

Larger clients often benefit from dedicated account representatives, giving them faster access to assistance. Smaller businesses may rely on general support lines, which can create inconsistent experiences depending on account size.

Reliability of the processing network itself is generally solid, with minimal downtime reported. Since the company leverages established banking infrastructure, most merchants experience steady service. However, as with any provider, occasional outages are possible, and businesses should evaluate whether backup plans are in place.

Pros of Using National Bankcard

National Bankcard’s advantages stem from its breadth of service. Businesses can manage in-store, online, and mobile transactions under one provider. The availability of POS systems, mobile readers, and online gateways provides flexibility for diverse models. Security compliance is strong, ensuring basic protections for sensitive data.

Merchants processing high volumes can negotiate competitive rates, making the service cost-effective in certain scenarios. Integration with common platforms also reduces administrative burdens. Finally, the company’s longevity in the industry gives it credibility, offering reassurance to merchants who prefer working with established providers.

Cons and Limitations

The biggest drawback reported by many merchants is pricing transparency. Without standardized interchange-plus offerings advertised upfront, contracts may involve tiered pricing and hidden fees. Long-term contracts with early termination penalties can also lock businesses into arrangements that are difficult to exit.

Customer support quality is inconsistent, particularly for smaller businesses. While larger accounts may receive dedicated attention, smaller merchants may struggle to get quick resolution. Equipment leasing programs may reduce upfront costs but can accumulate into long-term expenses that outweigh ownership.

Innovation is another area where the company lags. While it provides the basics across mobile and online payments, competitors in the fintech sector often deliver more advanced tools with clearer pricing models. Businesses seeking cutting-edge solutions may find National Bankcard more conservative than expected.

Ideal Business Types for National Bankcard

National Bankcard is versatile, serving retailers, restaurants, service providers, and e-commerce merchants. Restaurants benefit from tipping and order management functions, while retailers value inventory tracking and barcode support. Mobile businesses gain from portable readers that allow payments at client sites or events.

E-commerce sellers find recurring billing and fraud detection useful, particularly for subscription models. Professional service providers may appreciate reporting features that simplify billing and chargeback management.

The company is best suited for small to mid-sized businesses that need a balance of in-store and online acceptance without deep customization. Larger enterprises with complex technical needs may require more specialized providers.

Competitor Comparison

Against competitors, National Bankcard’s strengths lie in its longevity and service breadth. Unlike newer fintech entrants that focus heavily on one channel, National Bankcard provides a multi-channel solution. However, transparency and innovation are areas where rivals often hold an edge.

Flat-rate processors like Square or Stripe appeal to merchants who prefer simplicity, while other traditional providers may offer more advanced POS ecosystems. Businesses must decide whether stability and experience outweigh the appeal of transparent rates and modernized platforms.

Final Verdict

National Bankcard delivers a comprehensive suite of merchant services covering card processing, POS systems, mobile acceptance, and online gateways. It performs reliably, meets compliance requirements, and integrates with common platforms. Larger merchants can benefit from negotiated rates, while smaller merchants gain flexible hardware and multi-channel options.

However, the company’s lack of pricing transparency, potential for restrictive contracts, and mixed support quality are significant considerations. It may not be the most innovative provider, but it remains a credible choice for businesses seeking established reliability. Merchants considering National Bankcard should review contracts closely, clarify fees, and evaluate support responsiveness before committing.

FAQs

Q1. Is National Bankcard suitable for small businesses just starting out?

Yes, National Bankcard offers entry-level tools that help small businesses accept payments. However, new merchants should carefully review contracts and confirm pricing terms to avoid hidden fees.

Q2. Does National Bankcard support e-commerce integrations with popular platforms?

Yes, National Bankcard’s gateway integrates with Shopify, WooCommerce, Magento, and other platforms. These integrations make it easier for online sellers to process transactions.

Q3. Are there cancellation fees with National Bankcard?

Yes, depending on the contract, early termination fees may apply. Merchants are advised to confirm cancellation policies in writing before signing an agreement.

Merchant One Review

By 10topmerchantservices October 3, 2025

Merchant One is a well-established credit card processing company that provides businesses with a range of tools to manage transactions efficiently. Over the years, it has positioned itself as a payment solutions provider catering primarily to small and medium-sized enterprises, though it also works with larger organizations. Its value proposition lies in making electronic payments more accessible, whether through point-of-sale systems, ecommerce gateways, or mobile readers. Lets read more about Merchant One Review.

The payments industry has undergone tremendous change in the last two decades, with consumer preferences shifting from cash to card, and more recently, toward digital wallets. Companies like Merchant One have grown alongside this shift, offering technology and service bundles that simplify complex aspects of accepting payments. Instead of focusing exclusively on hardware or software, Merchant One combines both, creating an ecosystem that supports modern businesses.

While the company highlights flexibility and customer service as its strengths, it also operates in a crowded market where transparency and reliability are key decision-making factors for merchants.

Company Background and History | Merchant One Review

Founded in 2002, Merchant One is headquartered in Miami, Florida, and has grown steadily to become a recognizable name in the payment processing industry. The company started with a goal to simplify how small businesses accept card payments at a time when setting up merchant accounts was often complicated and expensive. Over time, its client base expanded to include retailers, restaurants, service providers, and ecommerce businesses.

One of the reasons Merchant One has been able to maintain a presence in a highly competitive sector is its ability to adapt to new technologies and industry standards. From the introduction of EMV chip cards to the rise of mobile payments and contactless transactions, the company has consistently updated its offerings. By doing so, it has aligned itself with the expectations of both merchants and their customers.

Today, Merchant One claims to serve more than 350,000 businesses across different industries. This reach demonstrates not just longevity but also the ability to scale its operations. For many merchants, particularly those without large budgets, the appeal of a provider that understands the needs of smaller enterprises has been central to Merchant One’s growth. Its continued investment in partnerships and technology reinforces its role as a stable, mid-tier player in the U.S. payment ecosystem.

Partnership with Fiserv and Clover Systems

One of Merchant One’s biggest strengths is its partnership with Fiserv, a global leader in financial services technology. Fiserv provides the backbone infrastructure that enables secure and reliable transactions. For merchants, this partnership translates into confidence that their provider is backed by one of the most established names in the industry.

Through this relationship, Merchant One is able to offer Clover POS systems, which are among the most popular in the U.S. Clover hardware includes countertop terminals, mobile devices, and full POS stations that support everything from payment acceptance to inventory management. The availability of these systems gives Merchant One a competitive edge because it can provide tools that scale with a business’s growth.

Having access to Fiserv’s technology also ensures compliance with security regulations and the ability to handle large transaction volumes. This makes Merchant One suitable not just for small shops but also for mid-sized businesses with higher processing demands. While many independent sales organizations (ISOs) in the payment space struggle with credibility, Merchant One benefits from being tied to a trusted global processor. This affiliation reinforces reliability and helps mitigate concerns about operational risks.

Products and Services Overview

Merchant One’s portfolio covers a broad spectrum of payment solutions designed to serve different business models. At the core, it offers merchant accounts that allow businesses to accept credit and debit card payments. Beyond that, its services include:

Point-of-Sale Systems: A range of Clover terminals and stations for in-store payments.

Mobile Payment Tools: Card readers and mobile apps for accepting payments on the go.

Ecommerce Solutions: Secure payment gateways and virtual terminals for online businesses.

Recurring Billing: Options for subscription-based businesses to automate payments.

Gift Cards and Loyalty Programs: Tools that help merchants engage and retain customers.

The diversity of services shows that Merchant One is not restricted to traditional brick-and-mortar retail. It has made efforts to ensure ecommerce merchants and mobile service providers have access to the same infrastructure as physical stores. This breadth of offerings is a selling point for businesses that may evolve over time — for instance, a retailer adding an online store can expand within Merchant One’s ecosystem instead of switching providers.

Merchant One Pricing Structure

Pricing in the payment processing industry is often one of the most challenging areas for businesses to evaluate, and Merchant One is no exception. The company advertises competitive rates, though exact fees depend on business type, volume, and risk profile. Typical charges include interchange fees, per-transaction fees, and monthly service costs.

Merchant One has been noted for offering customized quotes, which means pricing is not always transparent upfront. For some businesses, this flexibility can be an advantage, as rates may be tailored to their specific processing needs. For others, the lack of standard pricing may feel opaque compared to flat-rate processors. Additionally, there have been reports of early termination fees and equipment lease agreements, which are important to clarify before signing a contract.

While Merchant One positions itself as an affordable option for small and medium-sized businesses, it is essential for merchants to read contracts carefully. Understanding monthly minimums, PCI compliance fees, and potential cancellation penalties is crucial. Like many traditional merchant service providers, its pricing model is more complex than newer fintech competitors, but it can be cost-effective for businesses processing significant volumes.

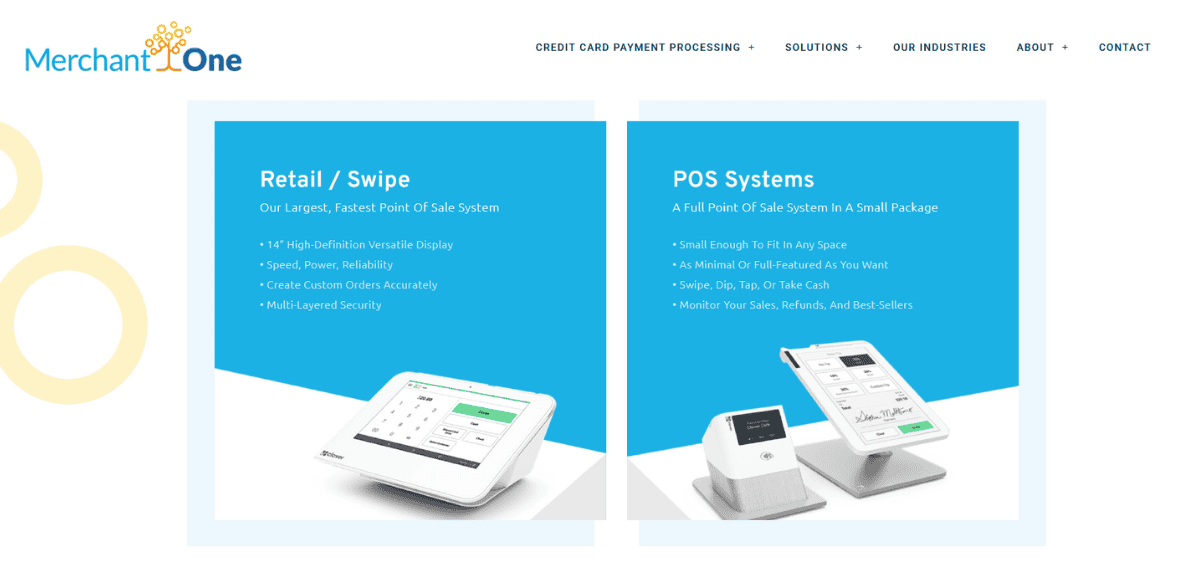

Hardware and Technology Options

A significant component of Merchant One’s value comes from its hardware offerings. By reselling Clover devices, it provides merchants with access to one of the most widely used POS ecosystems. Clover devices are known for their sleek design, reliability, and ability to integrate business management tools beyond payment acceptance.

Options include handheld readers like Clover Flex, countertop solutions like Clover Station, and simple mobile readers for businesses on the move. These devices are designed to handle a variety of payment types, including chip cards, contactless payments, and mobile wallets like Apple Pay and Google Pay.

The integration of technology extends to reporting and analytics. Many Clover devices come with built-in apps that help track sales, manage employees, and oversee inventory. This means that for businesses looking for more than just payment acceptance, Merchant One offers solutions that contribute to operational efficiency. While the hardware is an attractive feature, merchants should evaluate costs carefully, as device leases can add to long-term expenses.

Security and Compliance Standards

Security is a non-negotiable factor in payment processing, and Merchant One emphasizes compliance with industry standards. The company ensures that all accounts meet PCI DSS (Payment Card Industry Data Security Standard) requirements, which are designed to protect cardholder data.

Fraud prevention tools are also part of its services, offering merchants safeguards against chargebacks and suspicious transactions. Through its partnership with Fiserv, Merchant One can rely on advanced encryption and tokenization technologies that minimize risks during payment transmission.

However, compliance does come with associated costs. Merchants should confirm whether PCI compliance fees are part of their monthly charges. Failure to maintain compliance can result in penalties, so it is important that businesses understand their responsibilities. Overall, Merchant One delivers the level of security expected from a reputable provider, but merchants must stay proactive in ensuring ongoing compliance to avoid unexpected fees.

Onboarding and Application Process

Merchant One’s onboarding process is designed to be straightforward, though as with most merchant service providers, approval depends on business type and risk level. The application requires basic information such as business details, estimated transaction volumes, and processing history.

One of the company’s selling points is fast approvals. In many cases, accounts can be set up within 24 hours, allowing businesses to begin accepting payments quickly. This is particularly beneficial for new merchants who need to start operations without delays.

That said, some merchants have reported that the contract terms can be confusing at the outset. Clarity around pricing, equipment leases, and cancellation fees is essential before finalizing the application. Businesses should also be prepared for underwriting checks, which may take longer if the business falls into a higher-risk category. Overall, the process is competitive compared to other traditional providers but requires attention to detail from applicants.

User Experience and Ease of Use

Day-to-day usability is where Merchant One delivers tangible value for merchants. The systems provided, especially Clover POS, are known for intuitive interfaces that simplify training for employees. Features such as touchscreen navigation, integrated reporting, and digital receipts contribute to a smoother checkout process for customers.

For ecommerce merchants, the virtual terminal and gateway solutions are also designed with ease of use in mind. Businesses can process transactions online securely and manage them through centralized dashboards. Having consolidated reporting tools helps businesses monitor sales trends and customer behaviors, aiding better decision-making.

That said, some of the more advanced features may require additional apps or software, which can add to costs. While the base experience is user-friendly, merchants should evaluate whether they need premium add-ons or integrations. Overall, Merchant One provides a balance between functionality and simplicity, making it suitable for businesses without extensive technical expertise.

Customer Support and Service Quality

Customer support is a critical factor when choosing a payment processor, and Merchant One emphasizes its 24/7 availability. Merchants can access support via phone, email, and live chat, ensuring that technical issues or service interruptions are addressed quickly.

Many customers appreciate the responsiveness of Merchant One’s support team, especially during onboarding. However, reviews are mixed, with some merchants reporting difficulties in resolving billing disputes or contract-related concerns. This suggests that while the company has invested in accessible support channels, the quality of resolutions may vary depending on the issue.

For businesses that rely on uninterrupted payment processing, the assurance of around-the-clock support is a positive. Still, prospective merchants should research user experiences to understand potential challenges in areas like contract cancellations or fee disputes.

Reputation and Market Presence

Merchant One has built a sizable presence, serving over 350,000 businesses nationwide. Its affiliation with Fiserv adds credibility, while its longevity in the market signals stability. On platforms such as the Better Business Bureau (BBB), Merchant One holds accreditation, though ratings reflect a mix of positive and critical feedback.

Satisfied customers often highlight the reliability of payment systems and responsive onboarding support. On the other hand, complaints commonly revolve around contract terms, unexpected fees, or challenges with cancellation. These are not uncommon in the payment industry but are important considerations for merchants making a choice.

Market presence alone indicates that Merchant One is a trusted provider for many businesses. However, prospective clients should balance this reputation with a clear understanding of contractual obligations. Transparency remains a recurring theme when assessing the company’s overall image.

Advantages of Using Merchant One

Merchant One offers several benefits that appeal to a wide range of merchants. Its partnership with Fiserv provides access to secure, scalable infrastructure, while Clover POS systems offer modern hardware and business management tools. The ability to serve both in-store and online merchants makes it versatile.

Another advantage is the speed of account setup, which can be completed in as little as 24 hours. This is attractive for businesses needing to launch quickly. The company also provides 24/7 support, which is reassuring for merchants who cannot afford downtime.

Flexibility in services, such as recurring billing and loyalty programs, further enhances its appeal. For businesses that want more than basic payment acceptance, these add-ons provide opportunities to improve customer engagement. Ultimately, Merchant One’s strengths lie in its adaptability, industry credibility, and ability to provide a comprehensive package of solutions.

Limitations and Criticisms

Like many traditional payment processors, Merchant One has its drawbacks. One of the most common criticisms is the lack of transparent pricing. Customized quotes can make it difficult for businesses to compare rates upfront, and unexpected fees have been reported by some merchants.

Contract terms are another area of concern. Early termination fees and equipment lease agreements can lock businesses into longer commitments than anticipated. This may be challenging for newer businesses that need flexibility.

Customer service, while accessible, has received mixed reviews. Some merchants report excellent experiences, while others note difficulties in resolving disputes. The inconsistency highlights the need for businesses to carefully evaluate support quality.

Overall, Merchant One provides strong services but requires merchants to exercise diligence. Reading contracts thoroughly and asking detailed questions before signing can help mitigate many of the common complaints.

Who Should Consider Merchant One?

Merchant One is best suited for small to medium-sized businesses that need flexible payment options and reliable hardware. Retailers, restaurants, and service providers that value Clover POS systems may find Merchant One an attractive choice. Ecommerce businesses can also benefit from its secure gateways and virtual terminals.

However, businesses that prioritize flat-rate pricing and complete transparency may find newer fintech providers more appealing. Merchant One’s model is more traditional, which works well for merchants processing higher volumes but may feel restrictive for startups or businesses with uncertain cash flow.

In summary, Merchant One is a strong option for businesses seeking a balance between established infrastructure and versatile services. Those willing to navigate its contracts and pricing structures may find it to be a long-term partner in payment processing.

Conclusion and Final Thoughts

Merchant One has established itself as a reputable provider in the competitive payment processing market. Its partnership with Fiserv and use of Clover POS systems ensure that merchants receive reliable, modern tools. The breadth of services, from in-store payments to ecommerce and mobile processing, highlights its versatility.

At the same time, the company’s limitations in transparency and contract flexibility are important considerations. Businesses must weigh the benefits of secure, scalable infrastructure against the potential challenges of fees and long-term agreements.

For many merchants, Merchant One provides a dependable way to accept payments and manage business operations. With careful evaluation of terms, it can serve as a valuable partner in navigating today’s complex payment landscape.

FAQs

Q1. Does Merchant One require a long-term contract?

Yes, Merchant One typically requires a contract that may include early termination fees. While some merchants report flexibility, it is essential to review terms carefully to understand the commitment involved.

Q2. What types of businesses benefit most from Merchant One?

Merchant One is well suited for retailers, restaurants, service providers, and ecommerce businesses. It is particularly useful for small to medium-sized companies that need a mix of in-store and online payment tools.

Q3. How does Merchant One compare with newer fintech providers?

Compared to fintech companies offering flat-rate pricing, Merchant One provides more traditional, customized pricing. This can be cost-effective for higher-volume businesses but may lack transparency for smaller merchants. Its advantage lies in its established infrastructure and partnership with Fiserv.

Electronic Payment Systems Review

By 10topmerchantservices September 29, 2025

Electronic Payment Systems is a merchant services provider that allows businesses to accept payments across multiple channels. In an era where electronic transactions are the norm, businesses can no longer view payments as a back office process. Customers expect seamless, secure and instant checkouts whether they are paying in person, through mobile wallets or online. EPS positions itself as a partner for businesses that want to meet this expectation by offering a range of services from traditional point of sale terminals to online payment gateways. Lets read more about Electronic Payment Systems Review.

The payments landscape is changing fast with contactless technology, digital wallets and recurring subscription billing. Merchants have to comply with industry standards, manage transaction costs and integrate flexible systems into their existing operations. It tries to balance reliability and flexibility by providing stable infrastructure, security support and scalable solutions. Like any provider, its effectiveness depends on the specific needs and priorities of the business using it.

This review looks at EPS across multiple areas including company background, core solutions, hardware support, e-commerce functionality, security, pricing, customer support and overall market relevance.

Company Background and Industry Position | Electronic Payment Systems Review

EPS has been in the payments industry for decades, building a reputation mainly among small to mid-sized businesses. Unlike newer fintech companies that operate on a flat rate, app based model, it is a traditional merchant account structure. This means formal underwriting, merchant agreements and service contracts which has been the norm in payment processing. Its longevity has helped it build industry relationships and a stable base of merchants that value predictability over innovation.

The payments industry is crowded and competitive. It competes with global giants like Fiserv, Elavon and Global Payments as well as disruptive fintech platforms like Square, PayPal and Stripe. While the big names get more attention with their technology driven tools, EPS appeals to businesses that value established processes, infrastructure and hands on support. For merchants that view payment acceptance as a critical function rather than a playground for experimentation, EPS provides a solid foundation.

The flip side of this is visibility. Compared to newer, more marketed platforms, EPS doesn’t have brand recognition among startups and digital native companies. In fast paced industries where recognition and innovation matters this can be a problem. But for industries like healthcare, hospitality and traditional retail that value compliance, regulatory stability and consistent service, EPS has credibility that only comes with being in the market for decades. Its challenge today is to stay relevant in a world that demands both traditional reliability and modern flexibility.

Core Payment Processing Solutions

At its core EPS allows merchants to accept payments through all major card networks including Visa, Mastercard, American Express and Discover. It also supports ACH processing for direct bank transfers so merchants can accept a variety of payment types in-store and online. The backbone of its processing infrastructure is stability which is critical for businesses that can’t afford downtime or transactional inconsistencies.

For physical store environments EPS offers countertop terminals, mobile readers and support for contactless payments like Apple Pay and Google Pay. These options cater to changing consumer expectations around speed and convenience. For digital businesses it provides an online gateway with features like recurring billing, tokenization and hosted payment pages. Together these tools cover the basics of modern payment acceptance.

Where EPS falls short is on value added features. Competitors like Stripe or Square highlight analytics dashboards, customer insights and advanced integrations that help businesses go beyond accepting payments to using transaction data for growth strategies. EPS delivers on core processing but stops short of positioning payments as a business intelligence tool. For many merchants this isn’t a problem as reliability trumps the bells and whistles. But for digitally ambitious businesses EPS may feel limited in scope.

Merchant Account Setup and Onboarding

Setting up an account with EPS follows the traditional underwriting model. Merchants must go through a credit review, provide financial history and submit documentation for risk assessment. This can take several days to weeks depending on the complexity of the business and whether it’s a high risk industry. For startups or unconventional industries the process can feel demanding compared to the instant approvals offered by fintech platforms.

The advantage of EPS’s model is long term stability. Businesses that pass underwriting are far less likely to encounter account holds or unexpected closures which are common complaints with instant approval processors. It ensures risk is managed upfront so there’s less chance of downstream disruption. For businesses that value consistency this structured approach is reassuring.

However the onboarding process doesn’t suit every merchant. Businesses that need to start processing within 24 hours often find EPS’s process too slow. While the onboarding team helps with paperwork and compliance the perception of slowness compared to fast moving competitors can deter time sensitive merchants. This is the ongoing trade off between thorough vetting and immediate convenience.

POS Systems and Hardware Support

EPS supports a range of point-of-sale solutions designed for various business settings. From traditional countertop terminals to mobile readers, it ensures compatibility with EMV chip cards, magnetic stripes, and contactless payments. For merchants operating in brick-and-mortar locations, this provides flexibility to meet customer expectations across payment formats.

EPS also offers integrated POS systems that connect payments with sales management and inventory tracking. These full-featured systems help retailers and restaurants manage transactions holistically, although their design leans more toward reliability than innovation. Equipment can be leased or purchased outright, depending on business preference and budget.

While EPS provides a strong foundation for physical payments, its systems appear conservative compared to modern cloud-based POS solutions. Businesses looking for built-in loyalty programs, customer engagement tools, or seamless integration with third-party apps may find EPS lacking. For merchants that only need stable, compliant, and efficient hardware, EPS’s offering works well. Those seeking advanced, all-in-one business ecosystems may prefer newer POS innovators.

Online Payment Gateway and E-Commerce Features

As digital commerce continues to grow, EPS’s online gateway provides essential support for businesses selling products and services online. Its gateway integrates with shopping carts, enables hosted payment pages, and supports recurring billing for subscription models. Tokenization features ensure sensitive cardholder data is protected during online transactions.

It offers a degree of customization, allowing merchants to embed its gateway into existing websites or rely on hosted solutions for easier deployment. This flexibility appeals to both small businesses looking for simplicity and larger companies with unique system requirements. Security is a core strength here, as merchants can process online payments with confidence in compliance standards.

That said, EPS faces stiff competition in the e-commerce space. Providers like Shopify Payments or Stripe are deeply integrated into the digital economy, offering developer-friendly APIs and plug-ins that streamline the process for online merchants. EPS provides the necessary infrastructure but lacks the developer-first approach that digitally native companies often demand. For traditional businesses expanding into e-commerce, EPS’s solutions are adequate. For tech-forward businesses, however, it can feel limiting.

Security, Compliance, and Fraud Protection

Security is non-negotiable in payment processing, and EPS maintains compliance with PCI DSS standards. The company employs encryption and tokenization to safeguard customer data during transactions. These measures ensure sensitive information is protected against interception and unauthorized use.

Fraud protection tools are available, including velocity checks, filters, and monitoring systems that flag suspicious transactions. While effective, these tools are not as sophisticated as the AI-driven fraud systems offered by some fintech competitors. They provide a reliable baseline but may not cover the most complex fraud patterns seen in high-risk industries.

One of EPS’s advantages is its support for PCI compliance guidance. Many businesses struggle with the complexity of meeting industry requirements, and EPS provides resources to assist merchants in maintaining compliance. While feedback on support quality varies, the overall framework ensures businesses can operate securely within established guidelines. EPS’s emphasis on compliance reflects its traditional model of prioritizing trust and stability over experimental innovation.

Pricing Structure and Fees

Pricing is often the deciding factor when selecting a merchant services provider. EPS employs traditional pricing models such as interchange-plus or tiered rates depending on merchant type and volume. This means fees vary depending on the card type, transaction method, and risk profile of the business. In addition to per-transaction fees, EPS merchants may encounter monthly account charges, statement fees, PCI compliance fees, and gateway costs.

Compared to flat-rate providers like Square, this structure can feel more complex. However, for larger merchants processing significant volumes, interchange-plus pricing can result in lower effective rates. The challenge lies in transparency. Some merchants report unexpected fees or confusing contract terms, while others praise EPS for delivering competitive costs once terms are clearly understood.

Contracts typically involve multi-year commitments with early termination penalties, which may discourage businesses seeking flexibility. For small businesses or startups, these agreements may feel restrictive, particularly when compared to the month-to-month structures offered by newer players. Overall, EPS’s pricing can be advantageous for established merchants with consistent volume but less appealing to businesses prioritizing simplicity and flexibility.

Customer Support and Service Quality

Customer support is one of the most crucial elements of a payment processing relationship. It offers support via phone, email, and online resources. Its model emphasizes direct communication with representatives rather than relying entirely on automated channels. This appeals to merchants who value the reassurance of speaking to knowledgeable staff when issues arise.

Feedback on service quality, however, is mixed. Some merchants highlight the responsiveness of EPS’s support team and appreciate the personalized assistance. Others report frustration with long wait times or inconsistent problem resolution. Documentation and training resources exist but are less extensive compared to the robust self-service knowledge bases offered by larger competitors.

For businesses that prioritize personal relationships and one-on-one support, EPS provides value. For those that prefer fast, self-service solutions, its resources may feel limited. This reflects the company’s broader identity as a traditional provider focused on human support rather than automated efficiency.

Integrations and Compatibility

Modern businesses often require their payment systems to integrate with accounting software, ERP platforms, and e-commerce tools. It supports a range of integrations that help streamline financial management and reduce manual reconciliation. Its solutions are designed to be compatible with many legacy systems, which is beneficial for businesses that rely on established infrastructure.

However, EPS does not offer the same level of developer-friendly APIs and plug-and-play integrations found in fintech platforms like Stripe. This makes it less appealing to companies that prioritize automation, customization, and technology-driven workflows. For businesses that prefer stability and compatibility with older systems, EPS is more than sufficient. For digital-first businesses seeking advanced integrations, it may fall short.

Strengths of EPS

EPS’s strengths lie in its reliability, long-standing industry experience, and broad range of payment solutions. Its infrastructure emphasizes stability, ensuring merchants experience consistent uptime and secure transaction handling. The structured underwriting process reduces the likelihood of account freezes, providing reassurance to merchants that prioritize consistency.

EPS also serves a wide range of industries including retail, hospitality, healthcare, and e-commerce. Its flexibility across physical and digital environments adds to its appeal. Personalized customer support remains a distinguishing feature, especially for merchants that prefer human interaction over automated systems. Overall, it succeeds in offering solid, dependable service for businesses that value traditional reliability.

Limitations and Potential Drawbacks

EPS also presents several limitations. Its pricing structure, while potentially cost-effective for large merchants, can be confusing for smaller businesses. The presence of multiple fees, combined with multi-year contracts, reduces flexibility and may discourage businesses that want straightforward arrangements.

Technology is another challenge. EPS’s tools do not always match the innovation and advanced features offered by fintech competitors. Merchants seeking detailed analytics, advanced mobile capabilities, or developer-friendly environments may find EPS restrictive. While it meets core processing needs, it does not position itself as a technology leader in the payments space.

These drawbacks do not make EPS unsuitable, but they highlight its best-fit scenarios. It works well for businesses that value compliance, stability, and structured support. It is less appealing to businesses seeking cutting-edge innovation or contract flexibility.

EPS for Different Business Sizes

EPS’s suitability varies depending on business scale. For small businesses, onboarding and contract requirements may feel burdensome compared to instant-approval fintech alternatives. However, once approved, small merchants benefit from EPS’s stability and reliable hardware support.

Mid-sized businesses often find EPS most advantageous. They have the volume to justify interchange-plus pricing and the operational need for integration with accounting and ERP systems. For these merchants, EPS strikes a balance between traditional reliability and manageable costs.

Large enterprises may use EPS as part of a broader payment strategy but often prefer providers with more advanced global capabilities. EPS’s offerings are best suited as supplementary support rather than primary solutions for global corporations. Overall, EPS fits best with businesses that prioritize consistency and compliance rather than innovation.

Final Verdict on EPS

Electronic Payment Systems represents a traditional yet dependable option in the crowded merchant services market. It offers reliable processing infrastructure, wide hardware support, compliance guidance, and personalized customer service. Its long-standing presence in the industry highlights stability and trustworthiness, appealing to merchants that value consistency.

At the same time, EPS faces competition from fintech firms that emphasize transparency, quick onboarding, and advanced technology. While EPS may not always provide the most innovative or cost-effective solution, it excels in delivering payment fundamentals. For businesses that prioritize compliance, structured support, and proven reliability over cutting-edge features, it remains a strong and dependable choice.

FAQs

Q1. What types of businesses benefit most from EPS?

It caters to industries such as retail, hospitality, healthcare, and e-commerce. It works best for businesses that value stability, structured onboarding, and traditional merchant account models rather than instant-approval fintech systems.

Q2. Does EPS provide PCI compliance support for merchants?

Yes, it assists merchants in maintaining PCI DSS compliance. It uses features like encryption and tokenization to protect customer data and offers resources to help businesses navigate compliance requirements.

Q3. How does EPS compare with newer payment processors in terms of pricing?

It employs traditional interchange-plus and tiered pricing models. For high-volume businesses, this can result in competitive rates. However, for smaller businesses, the complexity and additional fees may feel less predictable compared to the flat-rate pricing favored by newer fintech providers.

Charge.com Review

By 10topmerchantservices September 26, 2025

Charge.com has been a merchant services provider for nearly three decades. Founded in 1995, the company bills itself as a simple and affordable payment solution for businesses of all sizes. It offers in-person, online and mobile transactions to give merchants cost effective tools without big upfront investments. Over the years Charge.com has gotten attention for its low advertised rates and easy setup but has also gotten flak for hidden fees, outdated systems and mixed customer support. Lets read more about Charge.com Review.

Company Background | Charge.com Review

Charge.com entered the payment processing industry in the mid 1990s when small businesses were struggling to get affordable merchant accounts. The company’s initial strategy was to fill that gap by offering simple and inexpensive solutions that would allow entrepreneurs to accept credit cards without going through banks’ restrictive and expensive merchant programs. This gave Charge.com an early advantage especially among small businesses that needed low barriers to entry.

Through mergers and acquisitions Charge.com’s corporate structure has changed several times. It was acquired by Pipeline Data, then merged with Cynergy Data and eventually absorbed into Priority Payment Systems. These changes have given the company access to stronger financial backing and corporate oversight but also raises questions about consistency of service. Some merchants see the corporate backing as a stabilizing force while others worry about the complexity that comes with multiple ownership changes.

Despite being around for nearly thirty years, Charge.com’s online presence has not kept up with modern competitors. Its branding, website and user portal looks outdated which may give prospective merchants the impression that the company is behind the times. But for many cost conscious businesses branding is less important than reliability and affordability. Charge.com’s ability to stay relevant for almost thirty years is a testament to its ability to adapt as the payment industry gets more competitive and innovative.

Services Offered

Charge.com markets itself as a provider of versatile merchant services capable of serving both small operations and growing enterprises. Its offerings span key areas of payment acceptance and security.

Merchant Accounts and Processing Solutions

The cornerstone of Charge.com’s services lies in its ability to process credit and debit card payments. Merchants can accept transactions from Visa, Mastercard, American Express, and Discover, ensuring compatibility with the most widely used card brands. Additionally, the company supports electronic checks, which broadens its utility for businesses that serve customers who prefer direct bank payments. The ability to process high transaction volumes efficiently makes Charge.com a fit for both small and medium-sized merchants with steady sales activity.

Online Payment Gateways

Charge.com provides a secure payment gateway for businesses running e-commerce operations. This gateway allows website owners to embed checkout functionality directly into their sites through hosted forms or shopping cart integrations. While these features may seem basic compared to modern gateways with advanced customization, they remain useful for businesses that want a dependable way to handle online sales. Charge.com also emphasizes customization, giving merchants the flexibility to align the checkout page with their brand identity, which is essential for maintaining consumer trust.

Mobile Payment Options

Mobile solutions have become increasingly vital in an economy that favors flexibility. Charge.com offers mobile payment processing through smartphones and tablets, allowing merchants to accept payments on the go. This feature is particularly relevant for food trucks, trade show vendors, service professionals, and temporary pop-up shops. The mobile app includes features such as issuing digital receipts and tracking inventory, making it more than just a card-swiping tool. By providing this service, Charge.com positions itself as a partner for entrepreneurs who operate outside traditional storefronts.

Virtual Terminals and Recurring Billing

The virtual terminal is another useful feature, enabling merchants to process payments manually by entering customer card details through a secure online portal. For businesses that accept orders over the phone or by mail, this functionality is particularly valuable. Charge.com also supports recurring billing, an increasingly important feature for subscription-based businesses such as gyms, online services, and membership organizations. Its recurring billing tools allow merchants to automatically charge customers at set intervals, reducing administrative effort and improving cash flow reliability.

POS Solutions

For brick-and-mortar businesses, Charge.com provides POS systems. These include card readers and compatible software that allow retailers to process payments in physical stores. The POS systems integrate with basic inventory management, though they are not as advanced as systems offered by specialized providers. For businesses that need comprehensive retail management tools with analytics and hardware variety, Charge.com’s solutions may feel limited. However, for merchants who only require essential POS functionality, these systems remain useful and budget-friendly.

Payment Security Features

Charge.com emphasizes security across its services. Fraud-prevention tools include tokenization, encryption, AVS, and CVV checks. These measures protect sensitive data and reduce the risk of fraudulent transactions. By maintaining compliance with industry standards, Charge.com ensures that businesses meet the requirements necessary to handle cardholder information responsibly.

Industry-Specific Solutions

The company adapts its services for various industries, including retail, hospitality, and e-commerce. For example, high-volume retailers benefit from its scalable processing systems, while subscription-based businesses gain from recurring billing options. This tailored approach helps Charge.com remain competitive by demonstrating that its solutions are not one-size-fits-all but adaptable to sector-specific needs.

Pricing and Fees

Charge.com advertises itself as a low-cost option, but a closer look reveals complexities that businesses should evaluate carefully.

Breakdown of Costs

The company promotes transaction rates as low as 0.25%. However, this rate usually applies only to qualified transactions that meet certain requirements, such as being swiped in person with a standard consumer credit card. Non-qualified transactions; such as those keyed in manually, made with rewards cards, or processed online; may incur higher fees. Additional costs, such as monthly statement fees, gateway access charges, and PCI compliance fees, can increase the overall expense for merchants.

Hidden Fees and Transparency Issues

Some merchants have reported surprise fees, including setup costs, early termination penalties, or additional surcharges for specific transaction types. While Charge.com emphasizes transparency, these reports suggest that the clarity of its contracts may not always meet expectations. Businesses should carefully review terms and ask direct questions during the sales process to avoid unexpected expenses.

Comparison with Competitors

Against competitors like Square and PayPal, Charge.com’s model can be more attractive for high-volume merchants who benefit from low per-transaction rates. However, small businesses with inconsistent or seasonal sales may find the monthly charges disadvantageous. In such cases, providers that charge only per transaction without monthly fees may present a better deal. The choice largely depends on a business’s sales volume and transaction patterns.

Integration and Compatibility

Charge.com has integrations with various platforms and systems so it’s pretty flexible for different business models. It’s compatible with major e-commerce platforms like Shopify, WooCommerce and Magento so online retailers can embed payment solutions into their stores without much hassle. Charge.com also has APIs that developers can use to create custom integrations. While the APIs work, the documentation is not as comprehensive as the bigger competitors. Improving their developer resources could help them attract more tech-savvy businesses.

On the hardware side, Charge.com supports standard card readers and traditional terminals. This means businesses don’t have to upgrade their hardware. But it also means they don’t have advanced or specialized hardware options for merchants who want modern POS features like contactless payments, integrated loyalty programs or advanced analytics.

User Experience

User experience is important for payment processing platforms and Charge.com’s is a mixed bag. The account setup process is straightforward, application and approval process is quick and sales reps often provide direct onboarding support so merchants can start accepting payments right away. But businesses that want a self-service onboarding process might find Charge.com less efficient than competitors that offer fully digital signups.

The website and merchant portal is functional but outdated. Many modern payment processors emphasize sleek dashboards, intuitive navigation and visually appealing designs. Charge.com’s older design might deter businesses that value a nice user experience.

Customer support is 24/7 via phone and email. While the 24/7 availability is a big plus, feedback is inconsistent. Some users say responsive and knowledgeable support while others report delays or limited help. Adding live chat and comprehensive online resources could make a big difference in the support experience.

Pros and Cons

Charge.com’s appeal lies in its affordability and versatility, but merchants must also weigh its drawbacks.

Pros include:

Attractive rates for high-volume merchants

Support for multiple payment methods, including e-checks

Range of options across online, mobile, and in-store payments

24/7 customer support availability

Cons include:

Hidden or unclear fees in certain cases

Outdated design and branding

Limited advanced hardware options

Mixed reviews about support responsiveness

Security and Compliance

Charge.com takes payment security seriously, offering features that safeguard customer data and maintain compliance. The company adheres to PCI DSS standards, ensuring sensitive information is encrypted and securely transmitted. Fraud prevention measures include AVS checks, CVV verification, and chargeback support. Although effective, these tools are basic compared to more advanced systems offered by specialized fraud-prevention providers. Encryption is applied end-to-end, reducing the risk of interception during transactions. This focus on data security gives merchants confidence that their customers’ information is being handled responsibly.

Customer Feedback

Customer reviews of Charge.com reflect a blend of satisfaction and criticism. On the positive side, merchants appreciate the affordability and flexibility of its payment options. Many cite the ability to accept diverse payment methods, including e-checks, as a major advantage.

On the negative side, merchants often complain about hidden fees, outdated user interfaces, and inconsistent customer support. These recurring themes indicate areas where Charge.com could significantly improve its reputation. Transparency and investment in modern technology would go a long way in addressing these concerns.

Contract Terms and Policies

Charge.com typically requires merchants to commit to contracts lasting one to three years. These contracts often include automatic renewal clauses, which can catch businesses off guard if they are not aware of the terms. Early termination fees are a common frustration, sometimes running into hundreds of dollars. Businesses that attempt to switch providers before the contract ends may find themselves facing steep penalties. This highlights the need for merchants to carefully review all contract details, including cancellation policies, before signing an agreement.

Scalability for Growing Businesses

Charge.com has the infrastructure to support businesses that scale, offering high-volume transaction processing and integration with enterprise-level tools. This makes it a potentially viable option for companies planning to expand operations.

However, its limited reporting and analytics tools may hinder growing businesses that rely on data-driven decision-making. While basic reports provide visibility into sales and transactions, the lack of advanced analytics means businesses may need to invest in third-party solutions to gain deeper insights. Expanding its reporting capabilities would make Charge.com more competitive for scaling enterprises.

Reporting and Analytics

Reporting is a critical component for businesses monitoring financial performance. Charge.com provides fundamental tools that allow merchants to view sales summaries, transaction histories, and account activity. These reports are functional but not advanced.

For example, merchants looking for customer behavior insights, predictive analytics, or customizable dashboards may find Charge.com lacking. Competitors increasingly provide such features as standard, which highlights an area where Charge.com could enhance its value proposition. While the existing tools suffice for basic tracking, data-driven companies will likely need to supplement them with external analytics software.

Chargeback Management

Chargebacks can be costly and disruptive, so businesses need robust management tools. Charge.com offers fraud prevention measures, automated alerts for disputes, and support for responding to chargeback claims. These tools help merchants build a defense against chargebacks but are not as comprehensive as the solutions provided by specialized providers.

Merchants handling high volumes of transactions, especially in industries prone to disputes, may find Charge.com’s chargeback management insufficient for their needs. While it provides a basic framework, businesses that require detailed chargeback analytics or dedicated prevention programs may need to look elsewhere.

Customer Support Accessibility

Charge.com emphasizes accessibility by providing 24/7 support via phone and email. This is a major benefit for businesses that operate outside standard business hours or encounter urgent issues. However, the absence of live chat and a limited online knowledge base reduces convenience for users who prefer immediate, self-service solutions. Competitors are increasingly adopting these support channels to improve resolution times and empower customers. Expanding support resources could greatly improve the overall customer experience.

Final Verdict

Charge.com has remained a reliable presence in the merchant services industry for nearly three decades, largely due to its affordability and comprehensive basic services. It is a strong option for businesses seeking straightforward payment processing without unnecessary extras. However, its drawbacks; including outdated branding, inconsistent support, and hidden fees; make it less attractive for merchants who prioritize transparency and advanced technology. For small businesses focused primarily on low-cost solutions, Charge.com remains a viable option. But for enterprises or tech-driven companies, newer competitors may offer more sophisticated features and a better overall experience.

FAQs

Is Charge.com suitable for small businesses?

Yes. Its affordable pricing and variety of payment options make it a good choice for small businesses, though contract terms should be reviewed carefully to avoid surprises.

Does Charge.com require long-term contracts?

Yes. Most agreements span one to three years and may include early termination penalties. Merchants are advised to clarify terms before committing.

What industries does Charge.com serve?

Charge.com supports a wide range of industries, including retail, hospitality, e-commerce, and service-based businesses, tailoring its solutions to sector-specific requirements.

BluePay Review

By 10topmerchantservices September 23, 2025

BluePay is a long established payment processing company that has served businesses of all sizes across North America. Known for its secure and flexible transaction solutions, the company built a reputation for balancing innovation with reliability. Before being acquired by First Data and then integrated into Fiserv, BluePay was an independent provider that offered robust services to both brick-and-mortar merchants and online businesses. Its focus on compliance, security and multi-channel payment support made it a player in a crowded market. Lets read more about BluePay Review.

The appeal of BluePay was that it was more than just a processor. It bundled gateway services, ACH transactions, recurring billing and fraud protection, so businesses had one stop shop for payments. For e-commerce businesses the flexibility of the platform was a big plus, for traditional retailers the POS compatibility was a bonus. BluePay also emphasized security features like tokenization and PCI DSS compliance which reassured merchants worried about fraud and compliance risks.

But some users complained about pricing transparency and contract terms. Like many traditional processors BluePay required merchants to sign agreements that sometimes had early termination fees or unclear cost structures.

Company Background and History | BluePay Review

BluePay was founded in 2003 to deliver flexible, secure and comprehensive payment processing solutions to U.S. and Canadian businesses. From the start the company focused on helping merchants streamline transactions across multiple channels, whether through traditional POS terminals, online stores or recurring billing systems. Based in Naperville, Illinois BluePay quickly expanded its reach and became a reputable player in the payment industry.

Its growth was driven by the increasing demand for secure and efficient payment solutions in the mid 2000s. It became known for serving small and medium sized businesses as well as larger businesses with more complex processing needs. Over time the company added features like API integrations, hosted payment pages and tokenization as e-commerce and mobile commerce became more important.

In 2017 BluePay was acquired by First Data, one of the largest payment processors in the world. This allowed BluePay to leverage First Data’s infrastructure and resources while continuing to offer its services under its own brand for a period.

After First Data merged with Fiserv, BluePay’s operations were further integrated into Fiserv’s ecosystem so it could support merchants at scale.BluePay is no longer a standalone brand but still has an impact as part of Fiserv’s payment portfolio. Its heritage is in its focus on secure transactions and ability to deliver custom solutions to merchants as they evolved. Knowing this history helps you understand BluePay today.

Core Services and Solutions Offered

It has always been a full service payment processor with solutions for businesses across industries. At the heart of their offerings are credit and debit card processing services that allow merchants to accept payments online, in person and mobile. These are backed by robust security so they are PCI DSS compliant.

Beyond standard card acceptance BluePay offered ACH and eCheck processing which was great for businesses that do high volume or recurring payments. Nonprofits and subscription based businesses loved this feature as it was cheaper than card transactions. Another key part of BluePay’s service offering was recurring billing which allowed businesses to automate subscription payments and cash flow.

The payment gateway was the foundation of their e-commerce support, real time processing, fraud tools and customizable integration. Merchants could link BluePay’s gateway to popular shopping carts and business software so transactions would flow smoothly. They also offered virtual terminals, hosted payment forms and tokenization services to make it more user friendly and secure.

Omnichannel was also a big selling point. BluePay supported transactions in physical stores, websites and mobile apps so merchants could unify their payment operations. This was great for businesses with multiple payment environments. Overall BluePay’s services were comprehensive but you had to read the fine print on the contract and pricing. Businesses looking for end to end solutions loved their offerings especially those looking for scalability and flexibility in their payment operations.

Payment Gateway Capabilities

It’s payment gateway was a centerpiece of its offerings, designed to facilitate secure, real-time online transactions. The gateway enabled merchants to accept payments directly through their websites, mobile apps, or custom platforms. One of its strongest features was flexibility; it supported major credit and debit cards, ACH payments, and even recurring transactions, making it suitable for subscription-based businesses.

Integration was another key advantage. BluePay’s gateway was compatible with popular e-commerce platforms and shopping carts, reducing the technical barriers for businesses setting up online stores. For companies with custom requirements, BluePay provided APIs that developers could use to build tailored solutions. This adaptability appealed to merchants who needed more than a one-size-fits-all payment gateway.

Security was embedded into the gateway’s design. With tokenization, card data was replaced with secure identifiers, minimizing the risk of sensitive information being compromised. Coupled with encryption and PCI DSS compliance, this gave merchants confidence in handling online payments. The gateway also included fraud detection tools, such as address verification and CVV validation, to reduce chargebacks and fraudulent activity.

Merchants also benefited from reporting tools integrated into the gateway. These provided insights into transactions, settlements, and trends, helping businesses make informed decisions. However, some users noted that the interface could feel less intuitive compared to newer, tech-driven competitors like Stripe. In summary, BluePay’s gateway capabilities were strong and reliable, particularly for businesses that valued integration and security. While not always the most user-friendly option, it delivered robust functionality for merchants prioritizing safety and adaptability.

Security and Compliance Standards

Security has always been a cornerstone of BluePay’s services. The company emphasized compliance with the PCI DSS, which sets the benchmark for secure handling of cardholder data. By adhering to these standards, It helped merchants reduce liability and meet industry requirements without having to manage the complexities alone.

Tokenization was one of the standout security measures. Instead of storing sensitive card details, BluePay replaced them with secure tokens that could not be used outside the system. This drastically minimized the risk of data breaches and reassured merchants about their customers’ safety. In addition, end-to-end encryption ensured that transaction data remained secure from the point of entry to authorization.

Fraud prevention tools added another layer of protection. BluePay’s system supported AVS, CVV checks, and velocity filters to flag unusual transaction patterns. These measures reduced the likelihood of fraudulent charges and chargebacks. For industries with higher risks, BluePay offered advanced fraud detection tools to further safeguard payments.

Compliance extended beyond PCI DSS. BluePay also worked to meet industry-specific requirements, making it a trusted option for sectors like healthcare, which demand strict adherence to data protection laws. By offering features tailored to regulatory environments, the company positioned itself as a partner for businesses with sensitive customer data.

Although merchants appreciated these protections, some criticized the added costs or complexity associated with implementing advanced features. Overall, BluePay’s focus on security and compliance was a defining characteristic that helped it remain competitive in a payment landscape increasingly concerned with data safety.

Integrations and Compatibility

One of BluePay’s notable strengths was its wide range of integrations with third-party platforms. For e-commerce businesses, the ability to connect seamlessly with shopping carts like Magento, WooCommerce, and Shopify simplified the payment setup process. This eliminated the need for costly development work and allowed merchants to start accepting payments more quickly.

Beyond e-commerce, BluePay integrated with accounting software such as QuickBooks and enterprise resource planning systems. These integrations helped businesses unify their payment data with financial records, improving accuracy and reducing manual reconciliation. For organizations with custom needs, BluePay’s APIs offered flexibility to build tailored solutions, making it appealing to developers and IT teams.

POS compatibility was another valuable aspect. It supported integration with major POS hardware and software providers, enabling retailers to unify their online and in-store payment systems. This omnichannel approach was especially useful for businesses expanding across physical and digital channels. Nonprofits and service providers benefited from BluePay’s support for hosted payment forms, which could be easily embedded into websites for donations or invoice payments. These forms were customizable, secure, and easy to deploy.

Despite these strengths, some users reported that integrations could feel more complex than with newer, developer-friendly processors. Competing platforms like Stripe or Square offered more plug-and-play options, while BluePay sometimes required additional technical expertise. Nevertheless, for businesses seeking comprehensive integration with both mainstream and specialized systems, BluePay delivered solid compatibility. Its flexibility made it a practical choice for organizations with diverse payment and reporting needs.

Pricing Structure and Fees