Worldline Review

By 10topmerchantservices November 12, 2025

Worldline is a big player in the payments universe. This review will give a balanced view of the company: who they are, how they work, what are their strengths and weaknesses, what’s to come. Not to promote the company but to dissect their model, performance, strategy and risks so you can make your own judgement. In an age of digital payments, e-commerce and financial infrastructure, companies like Worldline are at the crossroads of technology, regulation and commerce; so their story is relevant. This review will cover the company’s history and evolution, business model, market position, financials, technology and innovation, geographical presence, regulatory environment, reputation and controversies, SWOT analysis, strategic outlook, stakeholder impact and conclusion. Lets read more about Worldline Review.

Company Background & Evolution | Worldline Review

Worldline has its roots in the early 1970s and has gone through several phases of growth, consolidation and strategic repositioning. Founded in 1972 as part of a French payments and transaction processing company, it became part of Atos SE and was later spun out as an independent company. Key milestones include the acquisition of European payment services companies such as SIX Payment Services in 2018 to strengthen its presence in merchant acquiring and payments infrastructure. As of mid 2020s, Worldline is present in dozens of countries and serves merchants, financial institutions, governments and corporations. The company has been through heavy acquisition, technology integration, global expansion and service diversification. But this rapid growth also brought integration complexity and exposure to many markets and regulatory environments. Understanding this history is key to understanding the business model and strategy.

Business Model & Core Services

Worldline’s business model is based on providing payments and transaction-processing services across multiple segments. The company has three main service lines: Merchant Services, Financial Services and Mobility & e-Transactional Services. In Merchant Services, Worldline supports merchants (in-store and online) by acquiring transactions, providing terminals or online payment platforms and servicing the acceptance process. The Financial Services segment serves banks and issuers with card issuing, processing, ATM networks and outsourcing of financial transaction services. The Mobility & e-Transactional segment supports non-payment digital transactions such as e-ticketing, mobility solutions, identity services or e-documents. By offering end-to-end payments infrastructure, Worldline captures value from multiple points in the transaction chain. Revenue comes from transaction volumes, platform subscriptions, hardware (terminals) sales or leases and outsourcing services. The model benefits from network effects, fixed cost efficiencies through scale and diversification across geographies and services. But global networks, fintech disruptors and local acquirers put pressure on the model and evolving regulatory costs for compliance and data protection.

Strategic Growth & Acquisition Strategy

Growth for Worldline has been driven largely by acquisitions and partnerships. The company’s expansion strategy involved acquiring complementary capabilities and integrating them to achieve scale. This approach allowed Worldline to rapidly gain market share, broaden its product offering, and strengthen its competitive position. Notable deals such as the acquisition of SIX Payment Services and Ingenico have been pivotal. However, acquisition-driven growth carries inherent risks: integration of different corporate cultures, legacy systems, and operational frameworks can be challenging. Worldline’s success depends not only on acquiring but on successfully assimilating these businesses while maintaining profitability and service quality. In the payments industry, scale provides both defensive and offensive advantages; helping the company defend against competitors and strengthen its market share. Partnerships and joint ventures also play a key role, especially in emerging markets, enabling access to local networks and regulatory licenses. As of recent years, the company has shifted focus toward organic growth, efficiency improvements, and cost optimization, recognizing that synergy realization and disciplined integration are essential for sustainable success.

Market Position & Competitive Landscape

Worldline operates in a highly competitive sector where global processors, card networks, fintechs, and regional players constantly compete. Among the key competitors are FIS, Fiserv, Global Payments, Adyen, and Stripe, all of whom offer overlapping or adjacent services. Within Europe, Worldline has carved out a leadership position, particularly in merchant acquiring and payment infrastructure. Its extensive merchant base, partnerships with major banks, and end-to-end services give it a strong foundation. Yet, competition remains intense. Margin pressure continues to rise as digital-first players leverage software efficiency, while merchants increasingly expect omnichannel, data-rich payment solutions. Moreover, the emergence of embedded payments and open banking threatens to disrupt traditional acquirer economics. To maintain its edge, Worldline must continuously innovate, improve customer experience, and reduce operational costs. Its position as a European payments champion provides scale and credibility, but maintaining that leadership amid global digital transformation will require agility, investment in new technology, and proactive risk management.

Financial Performance & Key Metrics

Worldline reported FY 2024 revenue of approximately €4.63 billion, a modest organic growth of about 0.5%. Adjusted EBITDA stood at €1.07 billion, representing a margin of roughly 23%, while free cash flow reached €201 million, or 19% of adjusted EBITDA. However, the company also reported a net loss of nearly €297 million in 2024, reflecting restructuring and impairment costs. In Q1 2025, revenue fell to €1.07 billion, a 2.3% decline compared with Q1 2024, largely due to flat performance in Merchant Services and weakness in Financial Services. These figures illustrate a company with strong scale and positive cash generation but struggling with profitability and growth momentum. Analysts have pointed to factors like slower hardware shipments, integration costs, and macroeconomic headwinds as constraints. The company’s near-term financial outlook remains cautious as it works to restore profitability, strengthen liquidity, and maintain investor confidence. Its success will hinge on operational efficiency, disciplined spending, and recovery in merchant transaction volumes.

Technology, Innovation & Product Portfolio

Worldline’s strength lies in its technological backbone and comprehensive product ecosystem. The company offers a blend of hardware and software products, including POS terminals, online gateways, and secure transaction platforms. Its systems are built for reliability, compliance, and scalability, catering to millions of daily transactions across sectors. Innovation efforts have centered on expanding e-commerce capabilities, integrating new payment methods such as digital wallets and instant transfers, and providing merchants with analytics, reconciliation, and fraud detection tools. The company’s investments in cybersecurity, real-time analytics, and modular architecture reflect a move toward more agile, API-driven systems. Furthermore, its Mobility & e-Transactional Services unit extends beyond payments into digital identity and ticketing, demonstrating diversification potential. However, maintaining technology leadership demands continuous investment and modernization of legacy platforms. The competition’s faster innovation cycles, especially among fintechs and neobanks, underscore the need for agility. Overall, Worldline’s technology ecosystem remains robust, but modernization speed and service innovation will determine its future relevance.

Global Presence & Geographic Strategy

Worldline’s operations span over 50 countries, but its strongest foothold remains in Europe, particularly France, Germany, Switzerland, and the Benelux region. The acquisitions of SIX Payment Services and Ingenico expanded its presence across Northern and Eastern Europe, making it one of the continent’s largest payment processors. Beyond Europe, Worldline has been cautiously entering Asia-Pacific, Latin America, and parts of Africa through partnerships and local subsidiaries. Its global expansion strategy balances scale with prudence; focusing on markets with regulatory openness, strong digital adoption, and sustainable growth potential. Nevertheless, global diversification brings challenges such as compliance variation, FX exposure, and the need for region-specific customization. Worldline’s ability to adapt to local consumer behavior and integrate with regional payment systems determines its success outside Europe. The company’s global reach enhances revenue stability and positions it as a bridge between mature and emerging markets, though maintaining operational consistency across regions remains an ongoing test of execution.

Regulatory, Risk & Compliance Considerations

Operating in a regulated industry, Worldline faces constant scrutiny from financial authorities across its markets. Compliance with frameworks such as GDPR, PCI-DSS, PSD2, AMLD, and various national banking laws is essential for maintaining licenses and trust. The company employs rigorous risk management systems to monitor transaction integrity, detect fraud, and ensure anti-money-laundering compliance. However, the broad geographic scope exposes it to varying regulatory standards, requiring significant investment in compliance infrastructure. Regulators continue to tighten oversight on payment processors, especially around merchant onboarding and cross-border fund flows. Non-compliance could lead to penalties, reputational damage, or restrictions on business activities. Recent events have underscored the importance of risk governance for Worldline, pushing management to strengthen its frameworks and internal audits. While the company’s size allows it to absorb regulatory costs, its long-term stability will depend on transparent practices, effective supervision, and continuous improvement in risk management.

Reputation, Challenges & Controversies

Worldline has recently faced serious reputational challenges that have shaken investor confidence. Reports surfaced in 2025 alleging lapses in oversight related to certain high-risk merchants and potential deficiencies in anti-money-laundering processes. These controversies led to a significant stock decline and regulatory investigations, particularly within its Belgian subsidiary. The company also faced internal restructuring pressures as it attempted to stabilize margins and control costs. In response, Worldline has emphasized governance reforms, compliance investments, and a renewed focus on transparency. Despite these corrective steps, the reputational damage has been significant, compounded by broader industry skepticism following several high-profile fintech failures. The firm’s future credibility will depend on how effectively it addresses compliance concerns, communicates with regulators, and rebuilds trust with clients. While its core operations remain intact, such incidents highlight the delicate balance between growth and risk control in financial services, where oversight missteps can quickly overshadow technical and commercial strengths.

SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

Worldline’s primary strengths include its vast European scale, integrated services, and proven ability to handle high transaction volumes with reliability. Its diversified business model; spanning merchants, financial institutions, and mobility services, creates resilience and cross-sector synergies. However, weaknesses persist in the form of integration complexity, reputational risk, and uneven profitability. The company’s reliance on hardware and legacy infrastructure also slows innovation relative to younger fintechs. Opportunities lie in expanding real-time payments, open banking, subscription billing, and analytics-driven value-added services. As global digital commerce grows, Worldline can leverage its infrastructure to capture new transaction flows. Yet, threats are significant: increased regulation, aggressive competition, cybersecurity vulnerabilities, and the lingering impact of reputational issues. The balance between capital discipline and innovation investment will shape the company’s ability to convert opportunities into long-term gains.

Strategic Outlook & Future Directions

Worldline’s management has signaled a strategic reset focused on cost efficiency, asset divestment, and disciplined growth. The company plans to simplify its structure, divest non-core assets, and focus on improving profitability through operational efficiency. Simultaneously, it seeks to regain market confidence through governance reforms and stronger compliance oversight. Growth opportunities will come from expanding in digital payments, contactless solutions, and B2B e-commerce. The company also plans to enhance automation and data analytics capabilities across operations. However, the next few years will be critical for rebuilding margins and investor trust. Success will depend on clear execution, transparent communication, and measurable progress in cash flow generation. In essence, Worldline stands at a crossroads: either transform its operational efficiency into a sustainable competitive edge or risk losing ground to faster, more agile payment innovators. The direction it takes will determine whether it remains a European leader or becomes a consolidation target.

Implications for Stakeholders

For merchants, Worldline’s comprehensive services offer convenience, scalability, and integration across online and offline channels. However, clients must assess factors like service quality, fee structures, and compliance reliability before committing to long-term relationships. For investors, Worldline presents both potential and caution. Its scale and infrastructure are assets in a growing digital payments market, but reputational challenges and execution risks remain major concerns. Investors will watch for improved profitability, steady cash flows, and leadership accountability. For regulators and partners, the company’s evolution will be an indicator of how large payment firms adapt to tightening oversight while maintaining innovation. A successful turnaround could re-establish confidence in Europe’s payment infrastructure landscape, whereas continued missteps could reinforce calls for stricter regulation. Across all stakeholder groups, trust, transparency, and consistency will define how effectively Worldline sustains its role in the payments value chain.

Conclusion

Worldline remains a cornerstone of Europe’s payments infrastructure, with deep technological capabilities and a broad service portfolio. Yet, its journey in recent years reflects the complexity of scaling a global financial technology enterprise. The combination of modest growth, regulatory scrutiny, and reputational headwinds has challenged its long-held leadership position. Still, the fundamentals; a vast merchant network, stable cash generation, and experience in managing critical payments infrastructure; provide a strong foundation for recovery. The company’s success will depend on its ability to strengthen governance, modernize technology, and deliver consistent value to clients and shareholders. In the coming years, execution and transparency will define whether Worldline emerges stronger from its current turbulence or remains burdened by legacy issues. The payments industry rewards innovation and accountability, and Worldline’s future will hinge on how well it balances both.

FAQs

Q1. What differentiates Worldline from other payment processors?

Worldline’s differentiation comes from its broad service scope; merchant acquiring, issuing services, and e-transactional solutions; combined with a dominant European presence and robust infrastructure. Its ability to offer end-to-end solutions across physical and digital channels makes it distinct, though maintaining agility amid fintech disruption is key to preserving that advantage.

Q2. What are the biggest risks facing Worldline right now?

The company’s major risks include regulatory and reputational exposure, ongoing integration challenges from acquisitions, margin pressures, and increased competition. Additionally, macroeconomic slowdown and potential compliance missteps could further strain profitability and investor sentiment.

Q3. How is Worldline planning to grow over the next 3–5 years?

Worldline aims to focus on organic growth, divest non-core assets, strengthen compliance frameworks, and expand its digital payment and data-driven service offerings. Its medium-term plan emphasizes operational efficiency, modernization of technology, and restoration of profitability through disciplined execution and transparent communication.

UnionPay Review

By 10topmerchantservices November 10, 2025

UnionPay is one of the world’s biggest payment networks, founded in 2002 and headquartered in Shanghai, China. It was born with the idea of building a domestic payment network that could rival Visa and Mastercard. Over time, UnionPay expanded beyond China to become a major player in the global payments space. Today it serves billions of cardholders and millions of merchants across the globe. Lets read more about UnionPay Review.

The company’s journey mirrors China’s growing influence in the global financial system. Initially focused on interbank card transactions within China, UnionPay developed capabilities in cross-border payments, e-commerce and mobile technology. With the establishment of UnionPay International, the brand gained access to overseas markets through partnerships with banks and payment processors.

UnionPay’s value lies in its dual identity; it is both a national infrastructure supporting domestic commerce in China and a competitive international payment brand. Its reach now extends to tourism, retail and online commerce. This review will cover UnionPay’s global footprint, digital payment solutions, business integrations and overall value proposition for merchants and users in 2025.

Global Reach and Market Presence | UnionPay Review

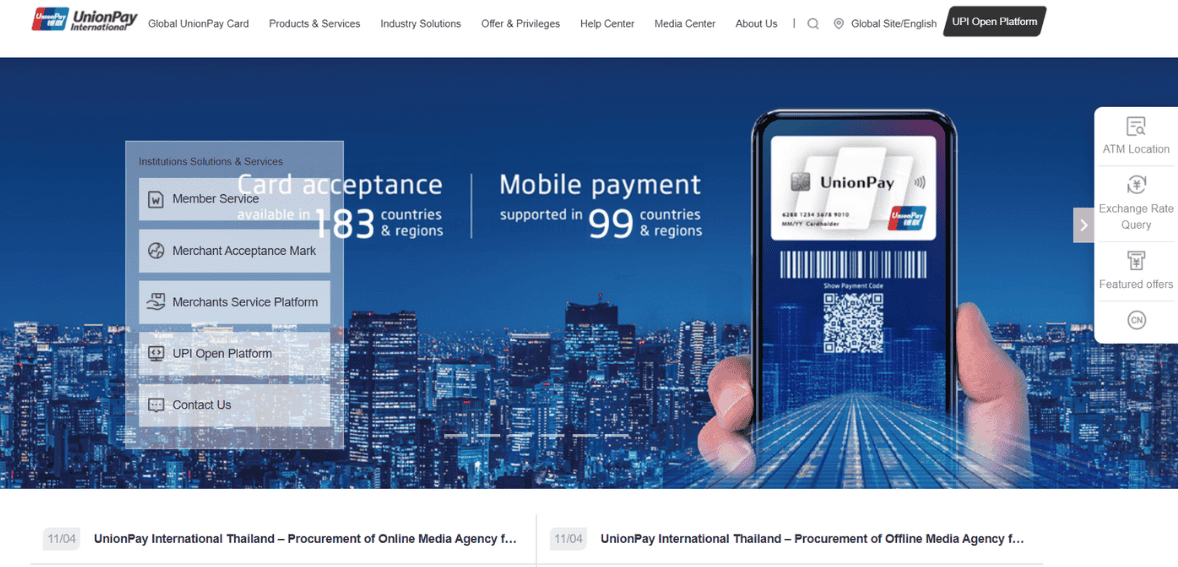

UnionPay’s global expansion has been one of the most impressive in the financial services industry. It’s in over 180 countries and regions, with over 10 billion cards issued worldwide. It’s number one in Asia, especially in China where it’s the default card. In recent years it’s been rapidly expanding in Europe, Africa and the Middle East.

Partnerships with local acquirers and banks have been key to this success. In North America for example, UnionPay cards are accepted at many ATMs and merchants through partnerships with Discover and other networks. In Africa, partnerships with regional banks have enabled UnionPay to grow in markets like Kenya, Nigeria and South Africa. UnionPay International is focusing on building interoperability with global payment systems.

Despite the impressive coverage, UnionPay’s penetration outside of Asia is still limited compared to Visa or Mastercard. Western merchants may not support UnionPay as frequently due to regulatory hurdles or low local demand. But its consistent growth and strategic partnerships show a long term commitment to global inclusion, so it’s definitely one to watch in the international payments space.

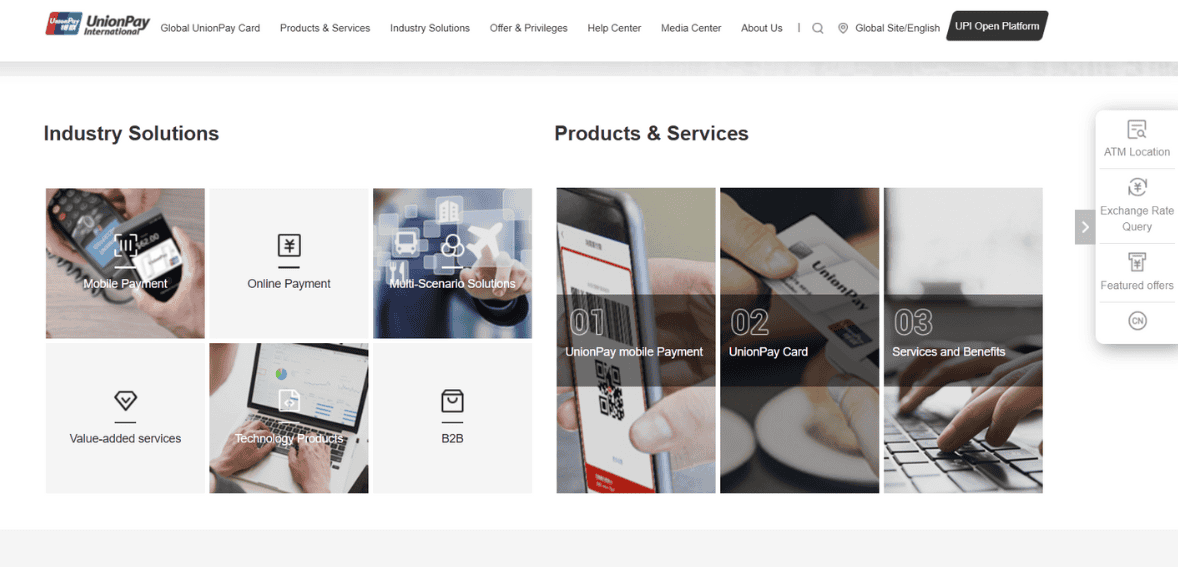

Core Products and Services

UnionPay offers a diverse suite of products designed to serve consumers, merchants, and financial institutions. Its traditional card products; credit, debit, and prepaid; form the foundation of its global network. UnionPay cards can be issued in local currencies or configured for multi-currency use, providing flexibility for international travelers and online shoppers.

In addition to card-based solutions, UnionPay has invested heavily in digital payment technologies. Its QuickPass platform supports contactless payments through NFC-enabled devices, while QR-based payment systems allow users to make purchases directly from smartphones. These innovations make UnionPay accessible to tech-savvy consumers and small businesses that rely on mobile transactions.

It also offers financial institutions white-label solutions for card issuance and transaction management. For merchants, its systems provide secure payment acceptance across in-store, online, and mobile environments. Beyond payments, it supports value-added services like loyalty programs, cross-border settlement, and data analytics. This wide-ranging product ecosystem positions UnionPay as more than a card network; it is an integrated payment infrastructure aiming to meet modern commerce demands.

UnionPay International: Cross-Border Capabilities

UnionPay International is the company’s global business arm and plays a key role in its cross-border strategy. It allows cardholders to pay and withdraw cash in multiple countries with the same card and provides international access. This division also partners with foreign banks, fintech platforms and acquirers to expand UnionPay’s global reach.

One of UnionPay International’s biggest strengths is its cross-currency support. Travelers and online shoppers can pay in local currency and funds will be settled through UnionPay’s secure network. It has become the preferred choice for Chinese tourists and overseas students who want familiarity and cost-effective payment solutions abroad.

To ensure interoperability, UnionPay International complies with international standards such as EMV and ISO protocols. Its partnerships with global payment processors ensure compatibility with existing merchant systems, so it’s easier for merchants to accept UnionPay cards. However in Europe and Americas, brand recognition is still a challenge. But UnionPay International is gaining traction as an alternative to Western networks, offering stability, lower fees and wider coverage.

Mobile and Digital Payment Ecosystem

UnionPay has made significant progress in digital transformation through its QuickPass and mobile QR payment ecosystem. QuickPass enables users to make tap-and-go transactions with smartphones, wearables, or contactless cards. This system mirrors similar technologies from Visa PayWave and Mastercard Contactless but integrates deeply with Asian mobile payment preferences.

In China and other Asian markets, QR code payments have become a cornerstone of everyday commerce. UnionPay’s QR solutions support interoperability with other regional networks, enabling merchants to process payments from multiple wallet providers. The company’s mobile payment infrastructure aligns with the global shift toward cashless and contactless experiences, particularly after the pandemic accelerated digital adoption.

It has also integrated with Apple Pay, Huawei Pay, and Samsung Pay in select regions, allowing seamless tokenized transactions. Its emphasis on real-time authentication and encryption ensures secure digital interactions. While mobile payment adoption remains regionally uneven, UnionPay’s continued investments in fintech collaborations and app integrations show its adaptability to emerging digital commerce trends worldwide.

Security Features and Compliance

UnionPay places a strong emphasis on transaction security, regulatory compliance, and consumer protection. Its systems follow international security frameworks, including PCI DSS and EMV chip technology, ensuring encrypted and tamper-resistant transactions. Every card transaction is monitored through a multilayered risk-control system designed to detect fraud in real time.

The network also implements tokenization for mobile and online payments, which replaces sensitive card data with secure digital tokens. This significantly reduces exposure to potential breaches during digital transactions. Additionally, It collaborates with law enforcement and banking partners to strengthen cybersecurity awareness and prevent card-related crimes.

From a compliance standpoint, UnionPay adheres to global AML and KYC regulations. It maintains close relationships with regulators across markets to meet localized data and privacy requirements. Despite these efforts, regional users occasionally report slower dispute resolutions compared to Western networks. Nonetheless, It’s comprehensive security protocols make it a trusted payment system for both consumers and businesses across multiple jurisdictions.

Merchant and Business Solutions

UnionPay provides merchants with a wide range of tools to accept payments across channels. Its POS systems support chip, magnetic stripe, contactless, and QR transactions, ensuring compatibility with existing retail hardware. Merchants can also integrate UnionPay’s e-commerce gateway for online sales, which supports local currencies and multicountry settlements.

For small and medium-sized enterprises, It offers simplified onboarding and affordable processing fees, helping businesses expand their customer base. Many tourism-dependent markets particularly benefit from UnionPay’s acceptance among Chinese travelers, which drives sales for hotels, retailers, and restaurants.

The company’s business solutions extend beyond payment acceptance. It’s data analytics and customer engagement tools help merchants understand consumer spending patterns. Additionally, loyalty programs and promotional integrations provide marketing value. However, UnionPay’s merchant service availability can vary by country, especially in regions with limited banking partnerships. Even so, as global e-commerce continues to grow, UnionPay’s merchant solutions present a viable path to accessing an increasingly digital, cross-border customer base.

UnionPay Online Payment Platform

UnionPay Online Payment serves as the brand’s digital payment gateway, designed for secure e-commerce and mobile transactions. It allows customers to make purchases using their UnionPay cards without sharing sensitive financial information with merchants. The platform employs advanced encryption and multi-factor authentication to safeguard transactions.

UPOP supports multiple currencies, languages, and settlement models, catering to international merchants and cross-border customers. Its integration capabilities enable developers to embed UnionPay into various websites and apps via APIs and SDKs. This makes it an accessible and flexible solution for businesses looking to expand globally.

From a user perspective, UPOP offers a simple checkout experience similar to other digital wallets, but with a strong emphasis on security and speed. It also supports recurring billing and installment payments, appealing to online retailers and subscription-based businesses. While UPOP may not yet match PayPal or Stripe in terms of global adoption, it represents UnionPay’s strong push into the digital payment ecosystem with reliable infrastructure and continuous enhancements.

Pricing, Fees, and Merchant Costs

UnionPay’s pricing structure varies across regions and merchant categories. In general, the company is known for maintaining competitive interchange rates, particularly in Asian markets. Its lower processing costs make it appealing for merchants targeting travelers from China or other Asia-Pacific countries.

Typical fees include transaction processing charges, cross-border surcharges, and exchange rate margins for currency conversion. Compared to global rivals like Visa or Mastercard, it often provides slightly lower overall costs, especially for domestic transactions within Asia. This advantage has supported its widespread adoption among cost-sensitive merchants and regional acquirers.

However, outside Asia, UnionPay’s fee structures can be influenced by local partners and banking networks. In some regions, setup or maintenance costs may offset its lower interchange benefits. Transparency in pricing also depends on third-party processors. Despite these variations, It’s affordability remains one of its key strengths, particularly for small businesses and global e-commerce platforms looking to diversify payment options without significantly increasing costs.

Customer Experience and Support

UnionPay’s customer experience varies depending on region and service channel. In China and much of Asia, users benefit from localized support centers and 24-hour helplines. The company provides multilingual assistance through phone, email, and online chat options, covering card issues, disputes, and fraud claims.

Feedback on responsiveness is generally positive in core markets, though international users sometimes report slower turnaround times. Dispute resolution processes, especially for cross-border payments, can take longer due to varying intermediary banks and regional policies. UnionPay continues to address this through its expanding network of international offices and customer engagement initiatives.

The overall user experience is enhanced by the brand’s intuitive digital platforms and reliable payment systems. For merchants, it provides onboarding assistance and integration support. While its service quality might not yet equal global leaders, steady improvement in global customer relations reflects UnionPay’s commitment to achieving international service standards that align with its growing footprint.

Integration with Global Fintech and Banking Systems

UnionPay’s success in the international arena is partly due to its collaborations with global fintech firms and financial institutions. By partnering with major acquirers and gateway providers, It ensures that its cards are compatible with most modern POS systems and online platforms. These partnerships simplify merchant onboarding and enhance user accessibility.

The company has also explored synergies with fintechs offering mobile wallets, neobanking services, and cross-border remittances. Integration with digital payment ecosystems like Apple Pay, Huawei Pay, and Samsung Pay demonstrates it’s ability to adapt to global technology trends. Additionally, it invests in blockchain-based experiments to streamline settlement and improve transparency.

In banking, it collaborates with more than 2,500 institutions worldwide for card issuance, transaction processing, and payment innovation. This collaborative model helps maintain flexibility in local markets. While regulatory complexity sometimes slows down deployment in certain countries, UnionPay’s openness to co-innovation positions it well within the rapidly evolving global fintech landscape.

trengths and Competitive Advantages

UnionPay’s greatest strengths lie in its scale, affordability, and technological adaptability. Its unparalleled reach across Asia provides a solid foundation for international expansion. The network’s cost-effective fee structure attracts merchants, while partnerships with local financial institutions ensure regional relevance.

The company’s focus on innovation has kept it competitive in a rapidly evolving payment environment. Its mobile and QR-based payment solutions align with consumer preferences in key markets, and the integration of contactless technology allows it to compete directly with established Western networks. Furthermore, UnionPay’s compliance with international standards enhances trust and credibility.

Another core strength is its government support within China, which ensures financial stability and operational resilience. UnionPay’s continuous investment in global partnerships helps bridge market gaps, creating a sustainable presence outside Asia. Together, these advantages make UnionPay a reliable and forward-looking player in the global payment industry, even as it navigates challenges of market perception and competitive maturity.

Limitations and Areas for Improvement

Despite its impressive growth, It faces several limitations. Its brand recognition remains lower in Western markets, where Visa and Mastercard have long-standing dominance. This restricts consumer demand and merchant prioritization. Some merchants in North America or Europe still view UnionPay as a niche option catering mainly to Chinese travelers.

Technical integration challenges also persist in certain regions where banking systems rely on legacy infrastructure. These barriers can delay onboarding or increase costs for smaller merchants. Moreover, the company’s dispute resolution processes and customer support availability outside Asia could benefit from greater localization and responsiveness.

Another constraint is regulatory compliance in diverse markets, which requires adapting to varying data protection and financial laws. it has made progress here but continues to face scrutiny in specific jurisdictions. Overcoming these challenges will be essential for UnionPay’s goal of achieving parity with Western networks and strengthening its image as a truly global payment brand.

Ideal Users and Final Verdict

UnionPay serves a wide range of users, from individual consumers to multinational merchants. It is particularly advantageous for travelers, international students, and businesses operating in Asia or targeting Chinese customers. Merchants seeking to diversify payment acceptance can benefit from It’s competitive fees and growing global reach. The platform is also suitable for fintech startups and e-commerce ventures that value secure cross-border payments and flexibility in settlement options. For consumers, it offers convenience, reliability, and access to a vast acceptance network.

However, users outside Asia may encounter limited acceptance compared to Visa or Mastercard. In conclusion, It stands as a formidable force in global payments; strong in scale, security, and innovation. Its continued growth beyond Asia depends on sustained investment in merchant expansion, brand awareness, and localized customer support. As the global economy moves further toward digital integration, It’s steady progress positions it as a valuable alternative in the evolving world of electronic payments.

FAQs

Is UnionPay accepted worldwide?

It is accepted in over 180 countries and regions. While coverage in Asia is near universal, availability in North America and Europe continues to expand through partnerships with banks and acquirers.

How does UnionPay compare to Visa or Mastercard in transaction fees?

It generally offers competitive pricing, particularly for domestic and regional transactions in Asia. However, fees can vary depending on acquirers and currency conversion policies in different countries.

Can businesses easily integrate UnionPay into their payment systems?

Yes. it provides APIs and SDKs that allow easy integration for both online and offline merchants. Global payment gateways increasingly include UnionPay as part of their supported methods, simplifying adoption.

TransNational Payments Review

By 10topmerchantservices November 6, 2025

TransNational Payments is an established merchant services provider based in Illinois founded in 1999 with a mission to make payment processing simple for small to mid-sized businesses. Over 20+ years the company has grown from a regional processor to a national processor offering in-store, online and mobile payment solutions. Their approach is human centered with technology that enables fast and secure transactions. TransNational serves many industries from retail and hospitality to healthcare and professional services, each requiring reliable payment infrastructure and transparent billing. Lets read more about TransNational Payments Review.

The company’s reputation was built on responsiveness and flexibility. Unlike many payment processors that cater to large businesses, TransNational focuses on creating adaptable tools for smaller merchants. Their services include credit and debit card processing, ACH payments, e-commerce gateways and custom integrations. This breadth helps business owners manage payments as they scale their business. But the effectiveness of these solutions depends on pricing transparency and customer support consistency, areas where merchant feedback has been mixed over time.

Overall TransNational Payments offers a broad feature rich ecosystem that blends traditional reliability with modern digital innovation making them a strong player in the US payments space.

Core Payment Processing Solutions | TransNational Payments Review

At the end of the day TransNational Payments offers payment processing systems that support credit cards, debit cards, contactless and ACH payments. Businesses can process transactions in-store, online or on the go depending on their business model. We use secure gateways to transmit sensitive payment data, meet industry standards and process fast. Whether you need countertop terminals, mobile readers or virtual terminals we have options to fit your transaction volume and customer needs.

Our credit card processing infrastructure is integrated with major card brands and is always up and running for consistent performance. Merchants like our flexibility; whether using a standalone terminal or connecting through a 3rd party POS system. We also offer recurring billing and invoicing tools for service based businesses. While we offer all these benefits, pricing and interchange plus rates can vary depending on the contract and sales rep. But our core product is robust, reliable and can handle all types of businesses that want one provider to manage all types of payments.

POS System Capabilities

TransNational Payments provides several POS options designed for ease of use, flexibility, and integration. Its POS systems combine hardware and software that can handle multiple payment methods, including EMV, contactless, and mobile wallet transactions. Merchants can customize the setup to meet their industry requirements; whether running a restaurant, boutique, or salon. Features such as inventory tracking, employee management, and customer data storage enhance the system’s business management capabilities.

One of the strengths of TransNational’s POS offerings lies in its scalability. Businesses can start with basic setups and add advanced modules as their operations expand. The systems are designed to integrate with various accounting and CRM tools, helping owners maintain a clear overview of their sales and performance. The user interface is intuitive, minimizing the learning curve for staff. However, some users have reported that hardware leasing contracts and upgrade costs can be restrictive, especially for small merchants. Overall, TransNational’s POS solutions strike a balance between functionality and simplicity, making them an appealing choice for businesses seeking unified control over transactions and back-office operations.

E-Commerce and Online Payment Tools

TransNational Payments helps e-commerce businesses with a range of online payment tools. Our payment gateway allows website owners to take credit and debit card payments securely, hosted payment pages make it easy for non-technical merchants to integrate, and our system is compatible with popular shopping carts and e-commerce platforms for seamless checkout. Developers can also use our APIs to build custom payment solutions for their unique business model.

The platform has fraud detection and tokenization to protect customer data during online transactions. Subscription based businesses can use our recurring billing feature for automated payment cycles. Virtual terminals allow merchants to process manual transactions or phone orders through a web interface. While these tools cover the basics for most online sellers, advanced customization and analytics may not be as extensive as the larger global processors. For small to medium e-commerce stores, TransNational Payments provides an easy, stable and secure way to take payments online without the technical headaches.

Security, Compliance, and Fraud Prevention

Security is central to TransNational Payments’ operations. The company adheres to PCI DSS compliance standards, ensuring that merchants’ and customers’ data are protected throughout the payment cycle. Its systems employ end-to-end encryption and tokenization to minimize exposure to sensitive cardholder information. These technologies safeguard data both in transit and at rest, reducing the likelihood of breaches or unauthorized access.

The company also offers support to help merchants achieve their own PCI compliance certification, an essential step for businesses handling customer payments. In addition, built-in fraud detection tools flag suspicious activity and help reduce chargebacks. While its fraud prevention framework is solid for most small and mid-sized merchants, high-risk industries may find the available monitoring options limited compared to dedicated fraud management providers. Still, TransNational’s emphasis on data protection and compliance reflects a strong understanding of today’s regulatory and cybersecurity challenges, giving businesses confidence in the safety of their payment systems.

Merchant Account Setup and Onboarding Experience

Setting up a merchant account with TransNational Payments is generally straightforward, though experiences vary depending on business size and type. Merchants typically go through an application process that includes business verification, credit checks, and documentation of sales volumes. The approval process can take a few business days, which is fairly standard across the industry. Once approved, merchants receive equipment and access credentials for their processing dashboard.

TransNational’s onboarding team provides assistance through phone or email, helping users integrate terminals or online gateways. The company has received positive feedback for its personalized onboarding support, especially for merchants unfamiliar with payment technology. However, some have reported that contract terms and fees were not always clearly explained upfront, leading to confusion later. Transparency during onboarding could therefore be improved. Overall, the process is efficient for businesses that value human guidance over a fully self-service experience, and the setup ensures merchants can begin accepting payments quickly after approval.

Pricing, Fees, and Contract Structure

TransNational Payments uses a pricing model that depends on merchant size, volume, and processing type. Most accounts are set up under interchange-plus or tiered pricing, though the exact structure is often determined by the sales representative. While interchange-plus pricing is generally more transparent, tiered plans can make it harder to estimate true costs. Standard fees include transaction percentages, monthly service fees, and occasional gateway or statement charges.

Some contracts may also include early termination fees or long-term hardware leases, which have been sources of merchant dissatisfaction in the past. TransNational’s contracts typically run for three years with automatic renewal clauses, though merchants can negotiate terms before signing. The company has improved transparency over time by providing clearer documentation and better access to statements. Still, potential customers should request a full breakdown of rates and fees before committing. In terms of competitiveness, TransNational’s pricing is comparable to similar mid-tier processors but may not always be the most cost-efficient for low-volume merchants.

Customer Service and Technical Support

Customer support plays a major role in TransNational Payments’ reputation. The company provides 24/7 technical support via phone and email, as well as dedicated relationship managers for larger accounts. Merchants often highlight the responsiveness of its support staff, particularly during initial setup or when troubleshooting equipment issues. For small business owners with limited technical resources, this human support can be a significant advantage.

That said, some users have reported inconsistent experiences, noting longer wait times during peak hours or delays in resolving billing discrepancies. The company’s online knowledge base covers basic troubleshooting and account management topics but lacks detailed guides for complex integrations. Overall, TransNational’s support system performs well for everyday issues and hardware assistance but could enhance its digital self-help options for more advanced users. Still, its reputation for accessible service remains a key differentiator compared to larger, less personal processors.

Integrations and Compatibility

TransNational Payments integrates with a variety of business software platforms to create a unified workflow for merchants. Its systems connect with accounting tools such as QuickBooks, allowing automatic reconciliation of transactions. The processor also supports e-commerce platforms and industry-specific POS systems, offering flexibility for businesses that rely on multiple tools. Integration with CRMs and inventory management applications helps centralize data, minimizing manual entry and errors.

API access allows developers to customize payment solutions or embed checkout functionality into their applications. This flexibility appeals to businesses seeking to tailor their payment processes rather than rely on generic options. However, the range of prebuilt integrations is somewhat narrower than that of larger competitors that maintain vast partner ecosystems. For small businesses, the available integrations are adequate to ensure efficiency, while tech-savvy merchants may appreciate the open API approach that encourages further customization.

Mobile Payment Processing and App Features

For businesses that operate on the go, TransNational Payments provides a mobile processing solution that turns smartphones or tablets into secure payment terminals. Its mobile app supports card swipes, EMV chip transactions, and contactless payments like Apple Pay or Google Pay. Merchants can issue receipts, track sales, and view transaction history directly from the app. This functionality makes it ideal for food trucks, market vendors, or service professionals who need to accept payments outside a traditional storefront.

The mobile reader connects easily via Bluetooth, and the interface is intuitive enough for quick training. Reporting features within the app provide real-time sales insights, though advanced analytics still require access through the main dashboard. Some merchants have noted that connectivity can vary depending on device compatibility, but overall, the mobile platform delivers dependable performance. TransNational’s mobile payment tools help level the playing field for small businesses by giving them access to enterprise-grade payment flexibility in portable form.

Reporting, Analytics, and Business Insights

TransNational Payments offers reporting tools that allow merchants to track sales performance, monitor transaction trends, and manage chargebacks. The analytics dashboard provides summaries of total volume, payment methods, and customer behavior over time. These insights help businesses make informed decisions about staffing, inventory, and marketing. Reports can be exported for accounting purposes, ensuring accurate recordkeeping.

The system’s user interface is straightforward, though some merchants may find the reporting capabilities basic compared to more advanced analytics platforms. Still, for small and mid-sized businesses, the available data is sufficient for everyday operations. Having centralized access to transaction history and batch settlements helps streamline reconciliation and compliance tracking. TransNational’s focus on functional simplicity rather than data overload suits business owners who prefer actionable summaries over complex visualizations. While not a full analytics powerhouse, it provides dependable visibility into payment activity and financial health.

Strengths and Competitive Advantages

TransNational Payments’ strengths lie in its balance of technology and customer service. Its wide range of processing options, covering in-person, online, and mobile transactions; makes it a one-stop solution for most merchants. The company’s reputation for personalized support is a key differentiator in an industry where many competitors prioritize automation over human contact. Additionally, its emphasis on PCI compliance and security gives merchants confidence in the integrity of their payment systems.

Another advantage is the flexibility of its product lineup. TransNational’s systems integrate smoothly with popular POS setups and accounting platforms, allowing businesses to manage operations more efficiently. The mobile processing tools also add versatility for merchants with hybrid sales models. While not the most inexpensive option, its reliability and human-centric approach make it appealing for small and mid-sized businesses that value stability and service over rock-bottom fees.

Limitations and Potential Drawbacks

Despite its strengths, TransNational Payments has a few areas where improvement is needed. The first is contract transparency. Some merchants have reported confusion over early termination clauses, monthly minimums, or statement fees that were not clearly explained before signing. These issues underline the importance of reviewing contracts carefully. Additionally, long-term equipment leases can increase total costs, especially for businesses that upgrade hardware frequently.

Another limitation is pricing competitiveness. While TransNational offers fair market rates, it may not always match the low fees of newer fintech processors that leverage automated systems to cut costs. Its reporting tools, while functional, lack the advanced customization that some data-driven businesses prefer. Lastly, international merchants or those requiring multi-currency processing may find its capabilities limited to primarily U.S.-based transactions. Nonetheless, for its target demographic of small and medium domestic businesses, TransNational Payments remains a dependable option with room to refine transparency and digital sophistication.

Verdict: Is TransNational Payments Right for Your Business?

TransNational Payments delivers a solid mix of reliability, service quality, and flexibility for small to medium-sized U.S. businesses. It stands out for its hands-on customer support, diverse payment options, and focus on compliance. For merchants seeking a provider that combines traditional account management with modern payment tools, it can be a strong fit. Retailers, restaurants, healthcare providers, and local service businesses benefit most from its tailored support and multi-channel processing.

However, businesses looking for ultra-low pricing or international capabilities might find better fits elsewhere. Transparency during contract negotiation is essential to avoid unexpected fees. Overall, TransNational Payments suits business owners who value dependable service and a personal relationship with their payment processor over fully self-service platforms. It may not be the most cutting-edge solution on the market, but its longevity and customer-centric model have made it a trusted choice for thousands of merchants nationwide.

FAQs

Q1. What types of businesses benefit most from TransNational Payments?

TransNational Payments is best suited for small and mid-sized businesses that require flexible, all-in-one payment solutions. Retailers, restaurants, healthcare providers, and service professionals often benefit from its mix of in-store, online, and mobile options. Its customizable POS systems and responsive support make it ideal for businesses that prioritize reliability and hands-on service over purely automated systems.

Q2. Does TransNational Payments support international transactions?

Currently, TransNational Payments primarily focuses on domestic U.S. processing. It supports major credit and debit card networks within the country but offers limited options for international or multi-currency transactions. Merchants engaged in cross-border commerce may need a secondary processor with global reach.

Q3. Are there any hidden fees to watch for in TransNational’s pricing?

While TransNational Payments provides clear rate information in most cases, some merchants have encountered unexpected statement or cancellation fees. It’s important to request a complete fee disclosure and clarify contract terms before signing. Understanding early termination clauses and hardware leasing details can help avoid surprises later.

SecurePay Review

By 10topmerchantservices October 31, 2025

SecurePay is an Australian-based payment gateway that provides businesses with secure, reliable, and efficient ways to process online and recurring transactions. Founded in 1999 and owned by Australia Post, SecurePay has built a strong reputation in the financial technology sector by focusing on simplicity and safety. It enables businesses to accept payments online through credit and debit cards, digital wallets, and alternative payment methods. Over the years, it has evolved to become one of the country’s most recognized payment processors, catering to a broad range of enterprises; from startups to large corporations. Lets read more about SecurePay Review.

SecurePay’s mission is rooted in enabling seamless payment experiences for both merchants and customers. The platform offers a complete suite of tools that go beyond just accepting payments; it also covers fraud prevention, reporting, and integrations with e-commerce platforms. Its foundation under Australia Post ensures reliability, compliance, and adherence to local regulatory standards, adding a layer of trust to its operations. For many Australian businesses, SecurePay represents a dependable partner that combines technological capability with the credibility of a long-standing national institution.

Company Background and Evolution | SecurePay Review

SecurePay was founded as a payment service provider under Australia Post to simplify online payments for businesses in the early days of digital commerce. Initially focused on online card processing, the company expanded to include recurring billing, tokenization and advanced fraud management. Being part of Australia Post gives us a unique advantage in terms of regulatory confidence and national reach.

As digital commerce grew in Australia, SecurePay adapted by introducing modern APIs, better integration and improved user experiences. We also built compatibility with major e-commerce platforms, because we’re all about scalability and user convenience. Over the years SecurePay has become a key player in Australia’s digital payments infrastructure, servicing both traditional and digital first businesses.

Our evolution shows how a legacy service can remain relevant in a fast changing fintech landscape. SecurePay balances compliance and innovation, our technology stack is aligned to global payment trends but grounded in Australian market needs. This has positioned us as a trusted option for merchants looking for local expertise and international performance.

Product Overview and Key Offerings

SecurePay’s product lineup caters to a wide variety of business needs, ranging from online payment processing to recurring billing solutions. Its Online Payments feature allows businesses to accept Visa, Mastercard, American Express, and other payment methods securely. Additionally, the Virtual Terminal lets merchants process payments manually, offering flexibility for call centers or remote billing scenarios.

The platform also includes Recurring Billing, a key tool for subscription-based businesses that need automated payment cycles. This feature ensures smooth management of customer renewals and reduces manual intervention. SecurePay’s FraudGuard adds an essential security layer, detecting and preventing suspicious transactions before they impact businesses.

Another noteworthy aspect is its compatibility with third-party tools and plug-ins. SecurePay integrates seamlessly with e-commerce platforms like Magento, WooCommerce, and Shopify, providing businesses with multiple avenues to accept payments without complex setups. For developers, it offers detailed API documentation and sandbox environments to customize integrations.

Overall, SecurePay’s offerings strike a balance between ease of use and robust functionality. Businesses can tailor the platform to their needs, whether managing a small online store or operating a large-scale enterprise system. Its emphasis on flexibility and reliability makes it an all-in-one payment solution for merchants looking for a unified approach to payment management.

SecurePay for Online Businesses

SecurePay is a household name among online retailers in Australia for its seamless integration and reliability. The gateway allows for customisable checkout pages so merchants can design customer experiences that reflect their brand while maintaining high security. With support for major credit cards and alternative payment methods, SecurePay lets businesses cater to all customer types.

For e-commerce platforms, SecurePay has plugins that make integration with Shopify, BigCommerce and WooCommerce a breeze. Merchants get quick setup and automatic sync with their online store. Tokenisation and recurring billing are particularly useful for subscription based models, while FraudGuard ensures safe transactions even during peak sales.

SecurePay also supports payment gateways that handle domestic and international transactions so businesses can expand beyond Australian markets. With real-time reporting and reconciliation tools, merchants can see their sales and track payments. For small to medium sized online businesses the platform is reliable and transparent in its fees. It gives you the core of online payment management without the complexity so you can focus on growth and customer engagement.

SecurePay for In-Person and Hybrid Businesses

While SecurePay is primarily known for its online payment capabilities, it also supports hybrid business models that blend physical and digital sales channels. Through its virtual terminal and integration options, merchants can process payments securely without requiring dedicated hardware. This makes it especially useful for service providers, phone order systems, or mobile-based businesses.

Although SecurePay does not specialize in traditional in-person POS terminals, it complements physical sales through integrations with third-party systems that manage in-store payments. Businesses with both retail and online operations can unify their payment data for better financial tracking and reporting. This integrated approach allows for consistent customer experiences across different touchpoints.

For businesses transitioning to omnichannel operations, SecurePay’s flexibility helps reduce the technical friction of managing multiple systems. It simplifies settlement processes, ensuring that payments from all sources are consolidated efficiently. While not a full-scale in-person POS provider, SecurePay effectively bridges the gap between online and offline payment environments. Its tools enable small retailers and service providers to expand their reach without overhauling their payment infrastructure.

Integration and API Capabilities

SecurePay has a documented API for developers who want control and customisation. The API can be integrated with various systems including e-commerce platforms, CRM tools and billing software. Developers can use SecurePay’s RESTful API to manage payments, refunds and recurring payments while keeping data secure with tokenisation and encryption.

The company has a sandbox environment for testing integrations before going live which is super useful for businesses building custom applications. Their integration libraries are available in common programming languages so you can embed payment functionality into your website or mobile app. In addition to APIs SecurePay has plug-ins for popular platforms like Shopify, Magento and WooCommerce. This reduces the need for technical expertise so it’s accessible to startups and established businesses.

While their API documentation is comprehensive some users note that the system may not have the same level of customisation as global providers. But for most Australian businesses SecurePay’s developer ecosystem has all the tools to build a reliable and compliant payment experience. It’s a developer friendly option that fits with local infrastructure.

Security, Compliance, and Fraud Prevention

Security remains one of SecurePay’s strongest pillars. The platform is fully PCI DSS compliant, ensuring that sensitive customer data is encrypted and protected during every transaction. SecurePay employs SSL encryption, tokenization, and secure authentication mechanisms to prevent unauthorized access and data breaches.

One of its standout security features is FraudGuard, an intelligent fraud management tool that helps merchants detect and block suspicious activities. FraudGuard analyzes transactional patterns in real time, reducing the risk of chargebacks and fraudulent orders. For businesses handling high transaction volumes, this feature provides significant peace of mind.

Because SecurePay operates under Australia Post, it is also governed by strict financial and data protection regulations, further reinforcing its reliability. Regular audits and compliance checks ensure that it meets both national and global standards.

While no payment gateway is entirely immune to risks, SecurePay’s layered security measures and proactive fraud detection systems make it one of the safer choices in the market. It combines national regulatory confidence with advanced technological safeguards, giving businesses and customers alike a sense of trust and assurance.

Pricing and Fees

SecurePay follows a transparent pricing model designed to suit different business sizes. It typically charges a flat transaction fee per processed payment, with variations based on card type and payment volume. There are no hidden costs, which helps businesses forecast expenses accurately. The standard pricing includes a setup fee, transaction fees, and a small monthly account charge for ongoing access.

Businesses that process larger volumes may be eligible for custom pricing, negotiated directly with SecurePay’s sales team. The platform’s fee structure is competitive within the Australian market, especially given the backing of Australia Post and its reputation for stability. While the pricing is straightforward, some users note that SecurePay’s fees for international transactions can be slightly higher than global competitors like Stripe or PayPal. However, the benefit lies in its local customer service, domestic settlement, and compliance with Australian banking systems.

Overall, SecurePay offers a fair balance between cost and value. Its transparent approach ensures there are no unexpected surprises for merchants, making it a trustworthy choice for businesses seeking predictable payment processing expenses.

User Experience and Interface Design

SecurePay’s interface is built with simplicity and clarity in mind. The merchant dashboard provides an organized view of transactions, settlements, and reports, making it easy to track business performance. The layout is clean, functional, and optimized for both desktop and mobile use.

For non-technical users, the intuitive navigation and detailed help resources make daily operations straightforward. Reporting tools allow merchants to filter transactions, monitor chargebacks, and export data seamlessly. SecurePay also supports integration with accounting tools, improving financial visibility for business owners.

From a technical standpoint, the interface facilitates smooth interaction with APIs and plug-ins, allowing developers to configure integrations without complications. Although the design might not be as modern as global competitors, its functional reliability and minimal learning curve make it accessible to all user types.

User feedback often highlights SecurePay’s stability and responsiveness over flashy aesthetics. The platform focuses on performance and dependability rather than visual frills, resulting in a consistent and professional user experience that prioritizes function over form.

Customer Support and Service Reliability

SecurePay’s customer support network is one of its key differentiators. Backed by Australia Post, the company offers local support through phone, email, and online ticketing. Merchants appreciate being able to reach a real person within Australian business hours; a feature often missing from international providers.

The platform’s documentation and online help center provide clear, step-by-step guidance for troubleshooting and integration. Additionally, SecurePay ensures high uptime reliability, with robust systems that minimize transaction delays or outages. While users generally report positive experiences, some note that advanced technical inquiries may take longer to resolve. However, the quality of responses and the personalized support make up for these occasional delays.

In terms of service reliability, SecurePay maintains strong performance consistency. It processes payments efficiently and settles funds promptly, ensuring minimal disruption to business operations. The overall reliability of its infrastructure, combined with dedicated support, reinforces its appeal to Australian businesses that value local accountability.

Pros of Using SecurePay

SecurePay’s major advantages stem from its reliability, compliance, and strong local presence. Being part of Australia Post gives it an inherent layer of trust and credibility. The platform’s transparent pricing, PCI DSS compliance, and fraud prevention systems make it suitable for businesses prioritizing safety and simplicity.

Another key strength is its integration ecosystem. Whether through APIs or plug-ins, SecurePay connects easily with popular e-commerce and accounting systems. Its user-friendly dashboard and real-time reporting tools enhance operational visibility, making it easier for merchants to stay on top of financial performance.

Local support is another standout benefit. Businesses can access quick assistance without dealing with timezone gaps or foreign support centers. Additionally, SecurePay’s ability to manage recurring payments and multi-channel transactions provides flexibility across industries. Overall, the platform is best suited for Australian businesses seeking a dependable and compliant gateway with excellent domestic support. It excels in reliability, transparency, and customer trust; three areas that continue to define its long-standing market position.

Cons and Limitations

Despite its strengths, SecurePay is not without limitations. One of the most common concerns among users is its limited focus outside Australia. For businesses operating internationally, transaction fees and settlement times may not be as competitive as those of global payment giants. The interface, while user-friendly, lacks some of the advanced customization options that modern fintech solutions offer. For instance, merchants seeking detailed analytics or API-level modifications might find SecurePay slightly restrictive.

Additionally, the absence of dedicated in-person payment hardware means businesses must rely on third-party POS systems for offline transactions. This could add an extra layer of complexity for those seeking a single unified solution.

Customer feedback also suggests that while support is prompt and helpful, documentation for complex integrations could be improved. Nonetheless, these drawbacks are relatively minor when weighed against its overall dependability. SecurePay remains a solid choice for businesses prioritizing local service and security over global scalability.

Ideal Business Types for SecurePay

SecurePay is particularly well-suited for small to medium-sized businesses, e-commerce retailers, and service providers that operate primarily within Australia. It’s an excellent choice for organizations that value local customer support and straightforward payment management. Subscription-based businesses benefit from its recurring billing tools, while online stores appreciate its seamless platform integrations.

Nonprofits, educational institutions, and membership-based organizations also find value in SecurePay due to its stable processing, transparent pricing, and reliability in handling recurring donations or payments. Businesses that handle sensitive data, such as healthcare or financial services, can rely on its compliance framework to maintain security and trust.

For larger enterprises, SecurePay’s scalability and API access enable deeper integration with internal systems. However, global brands seeking extensive international payment coverage might find its reach limited compared to multinational gateways. Overall, SecurePay fits businesses that want a dependable, regulation-compliant, and easy-to-use payment solution backed by a trusted national brand.

Final Verdict

SecurePay stands as a dependable and secure payment gateway built for Australian businesses that prioritize trust, compliance, and ease of use. Its backing by Australia Post lends unmatched credibility, and its offerings; from online payments to fraud prevention; cater to a wide range of industries. While it may not compete directly with global players on international coverage or advanced analytics, SecurePay’s local expertise, transparent pricing, and responsive support make it a standout option in its market segment.

Its straightforward integration process and reliable infrastructure allow businesses to operate efficiently with minimal disruption. In 2025, as payment technologies evolve rapidly, SecurePay continues to hold relevance by focusing on what matters most to merchants: safety, reliability, and consistent performance. For businesses operating in or targeting the Australian market, it remains one of the most trustworthy choices available.

FAQs

1. Is SecurePay suitable for international businesses?

It primarily serves Australian businesses, but it does support international payments. However, global transaction fees may be higher than competitors like Stripe or PayPal.

2. Does SecurePay integrate with major accounting or e-commerce platforms?

Yes, it integrates with popular platforms like Shopify, WooCommerce, Magento, and accounting tools like Xero, allowing for smooth payment and reconciliation processes.

3. What makes SecurePay different from other Australian payment gateways?

SecurePay’s key differentiators are its ownership by Australia Post, strong compliance framework, reliable local support, and transparent pricing; all of which make it a trusted choice for Australian merchants.

SecurionPay Review

By 10topmerchantservices October 28, 2025

In the fast-changing world of digital payments, businesses are constantly looking for solutions that are fast, reliable, and secure. SecurionPay is one such platform that has made a name for itself by offering smooth online payment processing backed by European-grade compliance and security. Based in Switzerland, the company has become a trusted partner for online merchants, subscription-based services, and SaaS providers seeking efficient payment systems that reduce friction for customers. Its core appeal lies in balancing user-friendly integration with strong protection and conversion-focused tools. Lets read more about SecurionPay Review.

SecurionPay was built with the idea that payment gateways should not complicate transactions. Instead, they should make digital payments faster, easier, and safer for both businesses and their customers. With a developer-friendly API, global card acceptance, and compliance with international data standards, it supports businesses of all sizes. What sets it apart is its emphasis on providing high conversion rates through optimized checkout flows and security measures that do not compromise user experience. As e-commerce and digital platforms expand globally, SecurionPay’s positioning as a modern, secure, and adaptable solution has helped it maintain steady relevance in the competitive payments industry.

Company Background and Core Philosophy | SecurionPay Review

SecurionPay was founded with a clear vision to create an online payment gateway that puts transparency, reliability and simplicity at its heart. Based in Switzerland, the company benefits from the country’s strict data protection and banking regulations which means merchants can trust us. Our mission is to provide secure and easy online payment solutions that can be tailored to any business model, whether retail, digital content or recurring billing.

The philosophy behind SecurionPay is to reduce the friction between businesses and customers. Many online payment systems complicate integration or have hidden fees that hurt smaller companies. SecurionPay offers predictable pricing, a clean API and a strong compliance framework so businesses can focus on growth not payment headaches. We also focus on conversion optimisation so every transaction has the highest chance of success through design simplicity and fast authorisation.

This balance of user centric design and back-end strength has allowed SecurionPay to carve out a niche among European fintech companies. We compete with global players but are smaller and more agile, we offer flexibility and personal attention to businesses that want reliability over scale. The result is a payment processor that is modern yet grounded in trust and performance.

Key Features and Functional Capabilities

SecurionPay offers a comprehensive suite of tools that make it suitable for diverse online business models. Its core features include card payment processing, one-click checkout, recurring billing, and a highly secure tokenization system. Merchants can accept major credit and debit cards globally, providing customers a smooth and intuitive checkout experience regardless of where they are located.

Another standout feature is SecurionPay’s advanced fraud prevention technology. It uses a combination of machine learning and data-driven analysis to flag suspicious transactions without interfering with genuine customer experiences. The platform’s API structure also allows merchants to design payment flows that match their website or application layout, maintaining brand consistency.

Recurring billing is another valuable feature that supports subscription-based services. Businesses can automate payments, send reminders, and manage failed transactions efficiently. Additionally, SecurionPay supports one-click payments, reducing friction for repeat customers and improving conversion rates. The gateway also offers strong chargeback management and real-time reporting tools, enabling merchants to track performance easily.

Together, these features create a flexible ecosystem that empowers developers and businesses alike. By combining payment efficiency with enhanced customization options, SecurionPay delivers both simplicity and control; two qualities essential for modern digital commerce.

User Experience and Interface Design

SecurionPay’s interface is super simple and easy to use. The dashboard is designed to help you manage transactions, see metrics and configure settings without the usual payment system learning curve. The onboarding process is a breeze, guiding you through setup, verification and integration. From a merchant’s perspective the interface is a balance of functionality and design. The transaction logs are tidy and the reporting tools make it easy to see payment summaries, refunds and customer activity. Developers love the organized API documentation which makes integration and testing much faster.

SecurionPay also offers a seamless experience for end customers. The checkout page is fast and flexible, fits in with websites or mobile apps. The responsive design ensures usability across devices and reduces cart abandonment. You can also customize the checkout form to match your brand which helps to build trust with your customer. Overall the user experience reflects SecurionPay’s philosophy of simplicity and efficiency. Whether you’re a small merchant or a large online retailer the interface is clear and accessible without the complexity.

Payment Options and Supported Currencies

SecurionPay provides merchants with a wide range of payment options, helping businesses serve customers across multiple countries. It supports all major credit and debit cards, including Visa, Mastercard, Maestro, and American Express. The platform also offers local payment methods where applicable, catering to customers who prefer regional or alternative payment systems.

Its global focus extends to multi-currency support, enabling merchants to accept payments in several international currencies. This flexibility is especially valuable for businesses operating in Europe, North America, and other global markets. The platform automatically converts and settles transactions in the merchant’s preferred currency, minimizing the complexity of cross-border payments.

While SecurionPay primarily focuses on card payments, it can be integrated with digital wallets and alternative payment methods through custom development. The inclusion of such flexibility reflects its API-driven nature, allowing developers to build hybrid solutions for niche requirements. For customers, the diverse payment choices improve convenience and confidence during checkout. For merchants, it means broader market reach without managing multiple payment providers. Together, this combination enhances conversion potential and provides a truly global payment experience.

API Integration and Developer Tools

SecurionPay is built for developers, so integration is easy and flexible. The RESTful API and documentation allows you to connect payment processing to your website, mobile app or e-commerce platform in no time. Developers can build custom payment forms, subscription workflows and fraud management systems without sacrificing security or performance.

The company provides SDKs for popular programming languages so implementation is smooth no matter what your team’s technical background is. Sandbox environments allow you to test before going live and identify issues early.