Authorize.Net Review

By 10topmerchantservices April 7, 2025

Authorize.Net has maintained a steady presence in the online payment industry since 1996. Currently owned by Visa, it has established a solid reputation for reliability and safe transaction processing. With compatible POS systems, Authorize.Net enables credit card and eCheck payments through websites, phone orders, and in-person sales for companies of all sizes. Lets read more about Authorize.Net Review.

Because of its robust security and flexible processing capabilities, Authorize.Net is often chosen by service-oriented and eCommerce businesses. The platform, which has more than 430,000 active users, is well-known for its extensive integration capabilities with shopping carts, merchant accounts, and other third-party tools.

One of the gateway’s standout qualities is its flexibility. Unlike newer services that bundle the gateway and merchant account, Authorize.Net allows businesses to bring their own merchant account or opt into its bundled offering; ideal for newer ventures.

Though it lacks flashy branding or modern aesthetics, Authorize.Net’s focus on security, reliability, and broad compatibility keeps it relevant amid a flood of trendy fintech upstarts. It remains a robust and trusted solution for those who value control and performance over visual flair.

Key Features at a Glance

Authorize.Net offers much more than basic transaction processing. It supports a wide range of payment types, including debit and credit cards, eChecks, and digital wallets, usable online, over the phone, or face-to-face.

Notable features include PCI-compliant hosted payment forms, recurring billing, customer data management, and the Advanced Fraud Detection Suite. Service providers and independent contractors can benefit from the email billing and invoicing features.

Custom workflows are made possible by its developer-friendly API, and merchants take advantage of integrated tools for subscription management and comprehensive report generation.

A major strength lies in its third-party integration support. Authorize.Net works with over 140 platforms, including eCommerce carts, CRM systems, and accounting software. While it doesn’t boast the sleekest look, its depth and stability serve complex businesses well.

Ease of Use and User Interface | Authorize.Net Review

In terms of usability, Authorize.Net offers a reliable experience but comes with a learning curve. Those unfamiliar with payment setups may find initial navigation challenging. Compared to newer competitors, its interface appears somewhat dated.

That said, the dashboard is logically organized, giving access to customer data, reports, and transactions. With some familiarity, users typically adjust quickly, though more technical functions may still require support.

With onboarding wizards, comprehensive documentation, and a committed support staff, the setup process has been enhanced. However, it might be less user-friendly for companies looking for plug-and-play solutions like Square or Stripe.

Although SDKs and a mobile app provide mobile support, they are not as polished as their mobile-first rivals. Authorize.Net is primarily focused on functionality, which many companies are willing to give top priority to.

Integration and Compatibility

Authorize.Net shines when it comes to integrations. It supports a range of platforms; both custom-built and popular ones like Shopify, Magento, BigCommerce, and WooCommerce; offering easy plugin options and robust API support.

Connecting more than 140 eCommerce carts and business tools, such as shipping and tax calculators and CRMs, is possible. The majority of companies with current systems find that implementing the platform is not too difficult.

The multilingual SDKs (Java, PHP,.NET, Ruby) are commonly used by developers, and REST and SOAP APIs offer extensive customization possibilities. Workflows, backend data handling, and checkout procedures can all be customized to meet particular requirements.

For retail, Authorize.Net supports various POS systems. While hardware integrations may require third-party support, the open ecosystem ensures flexibility and prevents vendor lock-in.

Payment Processing Options

The platform handles a wide variety of payment types, including credit/debit cards, eChecks, and wallets like Apple Pay, Google Pay, and PayPal, offering a flexible framework for collecting payments.

A standout is the virtual terminal for manually entering payments; ideal for service businesses taking phone or mail orders.

Recurring customers’ data can be safely stored to support subscription services in sectors like fitness and software as a service. There are also tools for automatically charging and managing loyal customers.

If the company is based in the United States, Canada, the United Kingdom, or Australia, international card payments are accepted. Currency compatibility is determined by merchant account settings.

Authorize.Net easily and dependably satisfies the standard processing requirements of numerous businesses, despite not being specifically designed for every international market or niche.

Security and Fraud Prevention Tools

One of Authorize.Net’s primary advantages is security. To guarantee that every transaction is safe and never revealed in plain format, it employs encryption that complies with PCI DSS.

Customizable filters are available in its Advanced Fraud Detection Suite to flag or block suspicious transactions. Location, quantity, velocity, and other triggers can all be used to modify filters.

Tokenization and CVV validation offer additional layers of safety, with tokenized data replacing card details during transactions. This significantly lowers the risk of breaches.

Other tools include IP blocking, velocity monitoring, and alerts for abnormal activity; key features for high-risk industries. While setup can be technical, the security offered is among the best in the industry.

Pricing and Fee Structure

Authorize.Net has two pricing models. The Payment Gateway Only option is $25/month, with $0.10 per transaction and a $0.10 daily batch fee, designed for those with an existing merchant account.

For an all-in-one solution, pricing is 2.9% + $0.30 per transaction with no monthly or setup fees; ideal for small businesses seeking simplicity.

Extra fees may apply for additional services, such as processing eChecks; these fees are usually $0.75 each. Costs may also apply to add-ons like fraud protection, depending on usage.

Considering its capabilities and dependability, this gateway is reasonably priced, despite not being the most affordable one on the market. The advantages of flexibility should be weighed against the slightly more complicated pricing by businesses.

Customer Support and Service Quality

Authorize.Net offers solid support, with 24/7 phone availability, email service, and a thorough knowledge base. The support portal contains guides, how-to articles, and troubleshooting FAQs.

The majority of user feedback is positive, particularly regarding common problems. Slow response times during peak hours have been reported by some, and more technical inquiries might not receive prompt resolution unless they are escalated.

Dedicated account managers may be provided to high-volume merchants, improving their customer service experience. Smaller retailers often turn to documentation or community forums for assistance.

Though not cutting-edge, the support resources cover a wide range of issues, making it a strong but traditional support offering compared to more modern platforms.

Recurring Billing and Subscription Management

Recurring billing is a strong suit for Authorize.Net. The Automated Recurring Billing tool simplifies payments for subscription-based services like gyms, SaaS platforms, and subscription boxes.

Merchants can configure trial periods, amounts, frequency, and start dates. The system handles billing automatically and securely stores customer data through its Customer Information Manager.

Businesses can monitor canceled or unsuccessful payments as well as active subscriptions through reporting. The ability to modify or pause current plans increases flexibility.

The subscription management interface isn’t as slick as more recent solutions like Stripe Billing, but it does the job securely and dependably.

Mobile and In-Person Payment Capabilities

Beyond online sales, Authorize.Net supports in-person payments through its Virtual Point of Sale and mobile solutions. Developers can use SDKs to build mobile integrations, while retailers can use card readers and POS systems.

These tools are ideal for field professionals like contractors or consultants who need to take payments on-site. Brick-and-mortar businesses also benefit from unified backend management.

However, hardware often needs to be sourced from outside sources, and the POS and mobile app features feel less advanced than those of Square or Shopify. However, for companies handling both online and offline transactions, the unified dashboard is a huge benefit.

Reporting and Analytics Tools

Authorize.Net offers a suite of analytics tools to help merchants monitor payments and uncover trends. From daily summaries to detailed transaction breakdowns, reporting is thorough and reliable.

You can generate custom reports on chargebacks, subscriptions, payment failures, and sales. Filters make it easy to isolate specific data sets based on time, method, or customer criteria.

Users can schedule automated email reports and export reports as CSV files. Although useful, the dashboard’s aesthetic isn’t as modern as more recent models.

The API gives data-savvy companies more insight and customization options for advanced analytics by enabling integration with external BI platforms.

Reliability and Uptime

Authorize.Net is known for exceptional reliability, offering nearly 100% uptime and a solid infrastructure that ensures uninterrupted payment processing.

Multiple data centers and redundancies support its system, ensuring performance even during periods of high traffic. Outages are uncommon, and planned maintenance is announced in advance.

Merchants consistently report excellent stability, even during peak shopping seasons or high-volume days. In an industry where downtime means lost revenue, Authorize.Net delivers dependable uptime that businesses can trust.

Who Should Use Authorize.Net?

Authorize.Net is ideal for established small and mid-sized businesses, growing online stores, service providers, and subscription companies. It suits users who prioritize security, flexibility, and robust features over ease-of-use or trendy interfaces.

Businesses with existing merchant accounts, specialized workflows, and custom websites will value the platform’s modularity. It is also appropriate for people who require advanced fraud tools or subscription billing.

However, entrepreneurs or small teams wanting a fast setup and minimal configuration might find Square or PayPal more approachable out of the box.

Pros and Cons Summary

Pros:

Strong security and long-standing reputation

Wide variety of payment methods supported

Excellent fraud prevention tools

Works with external merchant accounts

Extensive customization through API

Cons:

Outdated interface design

Requires technical knowledge for full use

Monthly fees may not suit low-volume sellers

Limited multi-currency options without add-ons

Authorize.Net may not be flashy, but for those seeking performance and security, it’s a trusted, stable partner.

FAQs

Q1: Is Authorize.Net suitable for small businesses or startups?

Yes, if the business expects a steady or high volume of transactions and needs tools like fraud prevention or subscription billing. Otherwise, the monthly fee may outweigh the benefits for very small startups.

Q2: Does Authorize.Net support international transactions?

Yes, it accepts international card payments, but the business must be based in the U.S., Canada, U.K., or Australia. Multi-currency support depends on the merchant account used.

Q3: Can Authorize.Net be used with a third-party merchant account?

Absolutely. One of its major strengths is its ability to integrate with existing merchant accounts. Alternatively, users can choose the bundled gateway + merchant account plan.

Amazon Pay Review

By 10topmerchantservices April 2, 2025

Amazon Pay is a digital payment system that was first introduced in 2007 with the goal of making online purchases easier for both businesses and customers. It enables customers to make purchases using the payment methods that are already connected to their Amazon accounts and is based on Amazon’s incredibly reliable e-commerce infrastructure. The technology offers a smooth checkout process for customers and lowers cart abandonment for retailers by doing away with the need to manually enter billing information or create new user accounts. Lets read more about Amazon Pay Review

Over time, Amazon Pay has transformed into more than a simple checkout option. It now includes features like voice-based payments via Alexa and easy integrations with popular ecommerce platforms, offering both security and speed. Backed by Amazon’s technical capabilities and reputation, it ensures frictionless transactions, making it appealing for online retailers aiming to optimize user experience.

That said, Amazon Pay competes with well-known names like PayPal, Google Pay, and Apple Pay. What gives it an edge is its integration with Amazon’s ecosystem, millions of shoppers already trust the brand and have stored payment information, which can significantly improve merchant conversion rates.

How Amazon Pay Works | Amazon Pay Review

Amazon Pay acts as a payment gateway that enables customers to use their Amazon credentials to make purchases on third-party websites. The checkout process is simplified, users log in with their Amazon accounts and confirm payments without re-entering details.

A user is taken to a secure page hosted by Amazon to select payment options and confirm their order when they choose Amazon Pay at checkout. They are returned to the merchant site after confirmation. Because of Amazon’s reliable infrastructure, this stands out while mirroring the ease of digital wallets.

For businesses, Amazon Pay integrates via APIs or plugins with platforms such as WooCommerce, Shopify, and Magento. It supports both one-time and recurring payments, making it ideal for retail, subscription, and digital service businesses.

Voice commerce is also part of the offering. Through Alexa-enabled devices, customers can manage subscriptions and place orders, a valuable edge in the fast-evolving commerce landscape.

Transactions are managed securely through Amazon’s backend. A comprehensive merchant dashboard provides access to order tracking, refunds, and performance metrics. The setup is relatively simple, even for businesses without in-house developers.

Key Features and Services

Amazon Pay brings a rich set of features to both consumers and businesses:

One-click checkout: By using stored Amazon data, customers bypass manual entry of billing/shipping info.

Alexa payments: Customers can transact via voice using Alexa-enabled devices.

Recurring billing: Businesses offering subscriptions or memberships benefit from built-in recurring payments.

Mobile optimization: The interface is responsive and functions smoothly across mobile browsers and apps.

Brand trust: The Amazon name boosts buyer confidence, especially on lesser-known websites.

Additional features include:

Multi-currency support

Buyer protection programs

Developer-friendly APIs and SDKs

Support for refunds and partial captures

But there are disadvantages. There are no built-in invoicing features in Amazon Pay, and developers may need to be involved in order to customize the checkout process. However, its wide range of products makes it appropriate for companies trying to increase customer convenience and foster trust.

Merchant Experience and Onboarding

Signing up with Amazon Pay is a relatively simple process. Merchants need to provide business credentials, complete identity verification, and integrate the service into their website.

The platform supports both custom integrations and pre-built plugins for Shopify, BigCommerce, WooCommerce, and others, accommodating both tech-savvy teams and those without coding knowledge.

The merchant dashboard, while basic, covers core needs like viewing transaction history, issuing refunds, and downloading reports. It may not offer as many customizable insights as other platforms, but it’s intuitive and functional.

During onboarding, documentation and ticket-based support are accessible. But according to some users, support response times are slower than those of competitors who provide live chat or dedicated account managers.

Additionally, Amazon Pay isn’t available for all business categories. High-risk industries or those with ambiguous product offerings may experience approval delays or outright rejections.

For most standard ecommerce businesses, the onboarding is smooth, and Amazon Pay’s brand appeal can improve buyer trust right from the start.

Customer Experience

Amazon Pay excels at making the checkout experience fast, safe, and intuitive for end users. Shoppers can quickly complete purchases using saved Amazon credentials, minimizing data entry and reducing checkout time.

This one-click experience is especially helpful on mobile devices, where cumbersome forms often lead to cart abandonment. Real-time notifications and confirmation emails further enhance transparency and user confidence.

Brand familiarity is important. Even when they are shopping on unknown merchant websites, customers are more likely to trust a payment method that carries the Amazon name. Businesses frequently see an increase in conversions as a result of this trust.

Alexa-powered payments are another user-focused feature. While adoption is still limited, the integration allows for voice-activated purchasing, particularly useful for repeat orders and subscriptions.

A downside: users who don’t have an Amazon account must sign up to use the service, potentially introducing friction. Additionally, Amazon Pay doesn’t support every local payment option, which can limit its appeal in certain international markets.

Fees and Pricing Structure

Amazon Pay’s pricing is competitive and easy to understand. For U.S. transactions, merchants are charged 2.9% + $0.30 per domestic transaction. International payments incur a slightly higher fee of 3.9% + $0.30, similar to rates from Stripe and PayPal.

There are no setup fees, monthly subscriptions, or cancellation charges, making it suitable for startups and small businesses looking to avoid fixed costs.

As is usual in the industry, refunds are permitted, but the fixed $0.30 portion of the transaction fee is not. Chargebacks cost about $20, which is again in line with industry standards.

Amazon also offers seller protection in the case of fraudulent or unauthorized transactions, although merchants are advised to read the terms carefully.

The pricing is transparent and straightforward, which helps with financial planning. However, high-volume merchants may find more competitive rates with providers offering custom pricing structures.

Supported Countries and Currencies

Amazon Pay supports a limited but growing list of countries, including the U.S., UK, Germany, France, Italy, Spain, Japan, and India. While this covers many major ecommerce markets, it falls short of the global coverage offered by PayPal or Stripe.

Customers can pay in their local currency thanks to multi-currency support, which lowers cart abandonment. However, Amazon’s exchange rates might not always be ideal, and there is no real-time currency conversion available.

Cross-border payments are possible, but both buyer and seller must be based in supported regions. Additionally, certain products and industries may be subject to restrictions depending on the country.

Merchants should verify whether Amazon Pay is available for their business type and region before onboarding.

Security and Fraud Protection

Security is one of Amazon Pay’s strongest assets. Built on Amazon’s infrastructure, it is PCI DSS compliant and employs SSL encryption and layered security measures. Customer credentials are protected via two-factor authentication and are never shared with merchants.

Fraud prevention is built-in, with algorithms monitoring for suspicious behavior. Amazon’s A-to-Z Guarantee adds a layer of protection for buyers and helps resolve disputes.

Nonetheless, merchants have limited access to fraud management tools. The majority of fraud detection is handled internally by Amazon Pay, with little transparency or seller customization, in contrast with Stripe Radar or PayPal’s comprehensive fraud dashboards.

Still, the system is effective for most use cases, and merchants benefit from Amazon’s secure environment without needing to manage sensitive data themselves.

Integration Options

Amazon Pay provides flexible integration paths suitable for both developers and non-tech-savvy users. For advanced teams, the API allows custom checkout workflows, recurring billing setups, and mobile app payments.

Pre-built plugins are available for platforms including:

Shopify

WooCommerce

Magento

BigCommerce

PrestaShop

These allow for plug-and-play integration, making the setup simple for most ecommerce businesses. Developers also get access to a sandbox environment and thorough documentation.

The user interface’s lack of extensive customization is one obvious drawback. The Amazon Pay interface may be restrictive for merchants seeking a fully branded checkout experience. Developer involvement might be necessary for complex flows or multi-step, custom forms.

That said, the platform supports both simple and advanced use cases and can be scaled according to business needs.

Performance and Reliability

Amazon Pay operates on Amazon’s global cloud network, ensuring near-instant transaction processing, high uptime, and robust reliability. Even during high-traffic events like Black Friday, the platform delivers consistent performance.

Merchants benefit from low latency and minimal checkout interruptions, leading to fewer abandoned carts and improved user satisfaction.

Real-time updates are provided by the merchant dashboard, which also makes reporting tools easily accessible. However, unlike competitors, Amazon does not provide real-time incident reports or public system status dashboards.

Customer support during technical outages is also limited, with no live assistance. Businesses requiring immediate support may find the ticket-based system insufficient.

Despite this, the overall performance is stellar, with minimal disruptions reported even during major shopping periods.

Mobile and Voice Commerce Capabilities

Amazon Pay shines in mobile and voice commerce. The service is fully responsive and performs well on mobile browsers and apps, providing a smooth user experience across devices.

Developers can enable in-app payments through the API, ensuring checkout is seamless within mobile apps. The platform’s lightweight design means quicker load times and better conversion rates.

What really sets Amazon Pay apart is its voice commerce integration. Alexa-compatible devices allow customers to place orders, reorder items, and manage subscriptions using simple voice commands.

For repeat purchases, this is particularly useful, a customer can say, “Alexa, reorder my vitamins,” and the transaction completes with stored payment and delivery preferences.

Nevertheless, the majority of these voice characteristics are exclusive to the Amazon ecosystem. This feature might not be important to users or companies that are not Alexa investors, and some users still have privacy and data tracking concerns.

Still, for future-facing ecommerce brands, Amazon Pay’s voice and mobile capabilities offer significant potential.

Use Cases: Ideal Business Types

Amazon Pay is an excellent fit for consumer-facing ecommerce businesses that prioritize user trust and ease of checkout. It works especially well for:

Online retailers

Subscription-based services

Digital goods providers

Donation platforms

Small and medium businesses benefit from the low barrier to entry, lack of monthly fees, and ease of setup. The platform’s design also appeals to companies with limited technical resources.

However, companies with complicated invoicing requirements (like B2B services) or those in high-risk industries might find Amazon Pay restrictive. Additionally, it is not the best option for retailers who deal in goods that are listed as prohibited categories by Amazon or who operate in nations that are not supported.

Customer Support and Resources

Amazon Pay’s customer support is its most polarizing aspect. While integration resources and developer documentation are robust, merchant support is mostly ticket-based, with no live chat or phone options for standard users.

Response times vary, and some merchants report delays, particularly during holidays or peak periods. For businesses handling urgent technical or transaction-related issues, this can be a drawback.

Amazon does offer:

A knowledge base

Integration documentation

Developer forums

Although these self-service options are extensive, they may not be enough for everyone. Enterprise clients with negotiated agreements may be eligible for dedicated support.

In general, Amazon Pay is best suited for merchants who can operate with minimal hand-holding or who already have experience with self-managed platforms.

Pros and Cons

Pros:

Widely trusted brand recognition

Seamless checkout with stored Amazon credentials

Quick integration with major ecommerce platforms

Voice and mobile commerce ready

Strong security and fraud protection

No setup or monthly fees

Cons:

Limited global availability

No real-time support (chat or phone)

Limited fraud tools for merchant-side control

Amazon account required for customers

Not suited for high-risk or B2B invoicing needs

Amazon Pay does a great job of balancing performance, trust, and ease of use. It can simplify checkout and increase conversion rates for the suitable business model. Others, however, might find it difficult due to restrictions in customer service and worldwide support.

FAQs

Is Amazon Pay only for Amazon sellers?

No, Amazon Pay is open to all online merchants. You don’t need to sell on Amazon’s marketplace, it can be integrated directly into your own website.

Does Amazon Pay store or share customer data with merchants?

Amazon Pay uses stored information from the customer’s Amazon account but doesn’t share full data with merchants. This keeps user data secure while enabling easy transactions.

How long do Amazon Pay payouts take?

Payouts generally take 3–5 business days to reach a merchant’s bank account. New merchants may experience slightly longer delays during verification.

Alipay Review

By 10topmerchantservices March 31, 2025

Alipay, introduced in 2004 by the Alibaba Group, has grown from a basic payment facilitator into one of the world’s leading mobile and online financial ecosystems. Originally created to facilitate transactions on Taobao, Alibaba’s e-commerce platform, it used escrow services to ensure trust between buyers and sellers. Since then, it has become a central offering under Ant Group (formerly Ant Financial), Alibaba’s fintech division. Lets read more about Alipay Review.

In China, Alipay is deeply woven into the fabric of everyday life; far more than digital wallets like PayPal, Apple Pay, or even WeChat Pay. With over a billion users globally, it supports everything from online shopping and in-store purchases to utility bills, healthcare, and commuting.

Alipay’s tremendous success is primarily attributed to China’s swift digital transformation and the government’s effort to decrease dependence on cash. What started as a payments application has transformed into a “super app” providing credit, wealth management, insurance, and a lifestyle platform for countless users.

While its origins are distinctly Chinese, Alipay has been broadening its presence worldwide. It has aimed at Chinese tourists internationally and developed merchant collaborations globally. With its Alipay+ approach, it currently facilitates cross-border compatibility with local wallets.

In spite of regulatory resistance, increasing global rivalry, and data privacy issues, It continues to be a leading player due to its convenience, integrated ecosystem strategy, and large user community.

How Alipay Works | Alipay Review

Alipay operates as a mobile-first wallet, allowing users to link their bank accounts, cards, or store value within the app to make fast and secure transactions. It works seamlessly across physical retail environments and online marketplaces, supporting payments via QR codes or digital transfers.

Getting started is simple: users download the app, register with their phone number, verify their identity, and link a bank account. Once set up, they can scan a merchant’s QR code or let the merchant scan theirs to complete payments; an approach that’s intuitive and widely adopted in China.

Transactions are processed in real-time, instantly debiting the user’s balance or bank account and crediting the merchant. Escrow services are available for online purchases, giving users the confidence to confirm delivery before payment is finalized.

Additional features include peer-to-peer transfers, bill splitting, and recurring payments. It also supports currency conversion automatically for international users, allowing them to pay in local currencies without relying on foreign cards.

The platform is secure and user-friendly. With facial recognition, biometric logins, and real-time alerts, users are kept safe and informed. While some services are tailored to Chinese regulations, most core features are now being extended to international audiences.

Alipay for Consumers

For consumers, it goes far beyond being a simple wallet. It’s an all-in-one platform that supports daily life functions such as paying bills, booking medical visits, or hailing rides. Its super app functionality makes it an indispensable tool for millions in China.

The key advantage is convenience. Users can shop online, pay rent, top up mobile data, buy insurance, and even invest; all from within the app. In urban China, Alipay usage is often more prevalent than cash or cards.

Users can customize the dashboard with commonly utilized services, enhancing personalization. The application additionally provides cashbacks, loyalty points, and discount vouchers according to user engagement; rewarding regular usage.

Notifications for transactions in real-time and monthly summaries offer clear financial monitoring. Budgeting applications and expenditure regulations assist in handling finances, allowing parents to establish restrictions for their children through the app.

Travelers gain advantages as well. In approved locations, it enables Chinese travelers to pay in yuan, while merchants receive their local currency. This cross-currency feature has turned it into a favored travel partner.

Nonetheless, beyond China, the experience could seem restricted because of a smaller number of supported merchants, language barriers, or regional limitations. The worldwide Alipay+ initiative is gradually tackling these issues.

Alipay for Merchants

Merchants, especially those catering to Chinese customers, stand to gain significantly from accepting Alipay. The platform’s infrastructure-light model allows even small shops to start accepting payments by displaying a QR code.

In China, it integrates smoothly with POS systems, providing features like customer data analysis, loyalty programs, and sales tracking. Internationally, it collaborates with local partners to ensure compliance with local regulations and smooth onboarding.

A standout benefit is Alipay’s in-app marketing. Businesses can create digital loyalty cards, promotional offers, and personalized ads, all within the Alipay ecosystem. These tools help maintain engagement with Chinese users.

Currency conversion and local settlements make it easier for cross-border merchants to receive payments quickly. This makes it ideal for businesses in tourist zones, especially those aiming to serve Chinese travelers.

Some challenges exist: integration can be complex for small merchants outside China, and regional support varies. Advanced tools may require technical help or API integration.

Still, Alipay’s blend of affordability, digital marketing, and real-time settlement makes it an attractive option for modern businesses.

Key Features of Alipay

Alipay’s value lies in its range of features that transform it from a simple payment tool into a daily utility hub. As a super app, it brings financial services, shopping tools, and life management together.

Its primary feature is mobile payments, supporting merchant payments, fund transfers, and recurring billing. Users can also pay transit fares and manage utilities within the app.

Financial services are deeply integrated. Through Ant Group, It offers mutual fund investments, BNPL services like Huabei, and access to micro-insurance. These are designed to enhance financial inclusion.

Security is a core strength. The app uses encryption, biometric authentication, and real-time fraud monitoring. Users can apply transaction limits and get alerts for any unusual activity.

Alipay introduces gamified experiences like “Ant Forest,” where eco-friendly behavior earns credits that fund tree-planting projects. This adds a social and environmental angle to user engagement.

While many of these services are China-centric, the Alipay+ initiative is gradually making them available in other regions. However, credit scoring and wealth tools may remain restricted in some countries due to regulations.

Ultimately, Alipay functions as a digital command center for its users, combining convenience with powerful functionality.

Global Reach and Expansion

Alipay’s global growth strategy began with serving Chinese tourists abroad, enabling seamless payments in local stores. Retailers in destinations like Japan, Korea, and Europe began accepting Alipay to attract these visitors without needing a major payment infrastructure overhaul.

Recently, Alipay+ has broadened its reach. This initiative enables global merchants to receive payments from various Asian wallets such as GCash, Kakao Pay, and Touch ‘n Go, via a single integrated platform. It’s a step towards expanded digital payment compatibility in Asia and elsewhere.

Thousands of merchants worldwide have integrated Alipay, ranging from airports and shopping centers to online marketplaces. The firm has additionally teamed up with banks and payment processors to guarantee adherence and easier integration.

Nonetheless, regulatory hurdles persist particularly in Western nations such as the U.S. where worries about data privacy and external access to financial systems have hampered advancements.

Nonetheless, Alipay’s flexibility and robust regional partnerships provide it with a hopeful avenue for ongoing global expansion as digital payments gain wider acceptance.

Cross-Border Payments and Currency Support

Cross-border functionality is a major strength for Alipay. For Chinese users traveling abroad, it automatically converts RMB into the merchant’s local currency using real-time exchange rates, simplifying payments and avoiding the need for cash or foreign cards.

Merchants benefit from quick settlements in their own currency, sparing them the burden of manual conversions or additional fees. This ease is especially useful for retailers in tourist hubs and e-commerce platforms selling to Chinese consumers.

It partners with global payment platforms and logistics services, facilitating online cross-border trade. Transparent pricing, buyer protections, and efficient refunds boost consumer trust.

Alipay+ extends these benefits to other e-wallets, making it easier for merchants to accept diverse regional payment apps via a single integration.

That said, currency conversion fees can vary by financial partner. Some regions may also face delays or limitations due to strict money transfer laws or anti-money laundering regulations.

Even so, Alipay’s real-time cross-border payment capabilities offer convenience and security, setting a high bar in the mobile wallet space.

Integration with E-Commerce and Retail

Alipay was originally developed to support Alibaba platforms like Taobao and Tmall. Its e-commerce roots are evident in its smooth transaction handling, buyer protection, and refund systems; all of which increase trust and improve user experience.

Buyers enjoy the added protection of escrow services, where payment is held until the product is received and approved. This feature has been widely emulated across other platforms.

Alipay’s API and SDK offerings make it simple for retailers to integrate the payment system into their websites. Platforms like Shopify and WooCommerce already support Alipay through plugins.

Brick-and-mortar retailers benefit as well. Whether using POS terminals or QR codes, they can issue e-receipts, loyalty rewards, and personalized discounts; all powered by user data and AI-driven targeting.

Challenges include language barriers, integration expenses, and a learning curve when targeting Chinese consumers. Accessing some features may require working with third-party vendors or local consultants.

Nevertheless, Alipay’s tight integration with retail and e-commerce ecosystems gives businesses a powerful tool for engaging a mobile-first audience.

Fees and Pricing Structure

Alipay is competitive in pricing, especially in its domestic Chinese market. Local users enjoy free or low-cost services, while merchants typically pay a small fee ranging from 0.5% to 1% per transaction.

Cross-border merchants may face slightly higher costs due to currency conversion and intermediary charges. Still, it tends to offer more favorable rates than global credit card processors.

The model is highly scalable, minor vendors utilizing QR codes encounter low fees, whereas major corporations employing POS integrations can arrange tailored terms. Numerous international services are managed via local partners, with pricing potentially differing.

Typically, consumers appreciate complimentary services, although premium offerings such as wealth management might include clear service fees.

Although typically economical, companies are advised to examine contracts thoroughly, as concealed charges could emerge based on the local processing partners. Models for pricing based on volume might also be relevant.

Overall, Alipay’s fee system is transparent and adaptable, making it a cost-effective option for companies looking to provide mobile payment solutions.

Security and Compliance

Security is a cornerstone of Alipay’s service. The app incorporates advanced encryption, AI-based fraud detection, and biometric verification including facial recognition and fingerprint scanning.

Real-time alerts and transaction logs let users stay on top of account activity. Users can also freeze their accounts, block cards, or impose spending limits directly from the app.

Alipay complies with strict regulations in China through the People’s Bank of China and follows global standards like PCI-DSS and ISO in international markets. Anti-money laundering (AML) and Know Your Customer (KYC) protocols are enforced through its global partnerships.

Western scrutiny especially regarding data handling and state access has limited its expansion in some regions. However, it continues to evolve its compliance framework to meet international expectations.

Despite geopolitical challenges, Alipay is widely regarded as a secure and compliant platform for both users and merchants.

Limitations and Challenges

Alipay’s primary drawback is its heavy regional skew. Most advanced features such as wealth management, insurance, and credit are confined to users in China. International versions often feel stripped down.

Language remains a barrier. While some sections of the app support English, many merchant interfaces are still optimized for Chinese users. This complicates onboarding and usage for non-Chinese speakers.

Geopolitical concerns and foreign ownership limitations have stifled Alipay’s growth in countries like the U.S. and India. Its ability to compete with domestic wallets in these markets remains constrained.

Integration can also be challenging, especially for small merchants needing third-party help to access Alipay’s full toolkit.

Finally, users without Chinese bank accounts may face limitations in top-ups or certain services, reducing the platform’s appeal outside its home market.

Comparison with Other Mobile Wallets

Alipay competes in a saturated market, standing out through its super-app ecosystem. Compared to WeChat Pay, it offers more financial tools and retail support, while WeChat excels in social features.

Against PayPal, Alipay is more integrated into users’ daily lives, although PayPal enjoys wider global usage and regulatory compatibility.

Apple Pay and Google Pay are strong in contactless and card-based payments, particularly in Western markets, but they lack Alipay’s broader lifestyle services and financial product integrations.

One of Alipay’s unique features is QR-based payments, which don’t require internet access, beneficial for low-connectivity areas and smaller merchants.

Still, Alipay may feel overwhelming or unfamiliar to users outside China, especially where local wallets are more intuitive or accessible.

Customer Support and Dispute Resolution

Alipay provides in-app help centers, AI-driven chatbots, and live agent options for resolving transaction or account issues.

Chinese users typically experience quick and effective support. However, international users may encounter delays, especially when language barriers or complex disputes arise.

Its escrow system ensures secure e-commerce transactions by holding funds until delivery is confirmed. Disputes can be raised with supporting documentation and are typically resolved quickly.

For merchants, technical assistance is available through documentation, developer portals, and onboarding partners.

Still, English resources and personalized international support need improvement. Better localization will be essential as Alipay scales globally.

Who Should Use Alipay?

Alipay is perfect for Chinese users and visitors, providing extensive integration with daily services, travel assistance, and financial resources. It is particularly beneficial in urban settings in China and in popular tourist destinations overseas.

Merchants aiming at Chinese consumers, whether online or in-person, ought to think about accepting Alipay to facilitate transactions and utilize its built-in marketing features.

Regional companies throughout Asia can utilize Alipay+ to accept multiple local wallets with one integration.

Outside of Asia, however, Alipay’s attractiveness might be restricted. Companies might discover options such as PayPal or Apple Pay to be better aligned with their local audience.

FAQs

Can Non-Chinese users and businesses use Alipay?

Yes, Alipay+ allows non-Chinese users and merchants to participate in cross-border transactions, though feature availability may vary.

What currencies does Alipay support for cross-border transactions?

It automatically converts user payments into the local currency of the merchant, supporting a wide range of currencies globally.

Is Alipay safe for storing money and making payments?

Yes. It uses top-tier security, including encryption, biometric authentication, and fraud detection, to ensure secure transactions.

Allied Wallet Review

By 10topmerchantservices March 29, 2025

Allied Wallet is a globally recognized payment processor offering a wide suite of financial tools, including credit card processing, digital wallets, and merchant account services. Geared toward businesses of all sizes, it positions itself as a comprehensive e-commerce solution. What differentiates Allied Wallet from competitors is its strong emphasis on transaction security, worldwide coverage, and support for a diverse set of payment methods. Lets read more about Allied Wallet Review.

Founded by Dr. Andy Khawaja, the company was built with the intention of delivering scalable, secure, and flexible transaction solutions—especially for the fast-growing online business sector. With a presence in more than 196 countries and over 100 million users, Allied Wallet promotes itself as a robust platform for secure and dependable payments on a global scale.

Small-to-medium-sized retailers looking for safe international payment options as well as enterprise-level companies growing abroad often use the platform. Allied Wallet provides a flexible infrastructure that can be tailored to different business models, whether you’re selling digital services, software subscriptions, or tangible goods.

Feedback is mixed despite its extensive offerings. While many users praise the support for cross-border transactions and the ease of integration, others voice concerns about inconsistent support and hidden fees. It’s not always the best choice, like many payment processors, but in the correct business environment, it could be a strong contender.

Company Background and Global Reach | Allied Wallet Review

Founded in 2002 by Dr. Andy Khawaja, Allied Wallet was created to simplify global commerce for merchants and consumers alike. Headquartered in Los Angeles, the company has expanded rapidly and now caters to clients in over 196 countries. Its growth over the years has solidified its reputation as a major player in international payment processing, particularly within the e-commerce sector.

The company’s global presence is one of its best selling points. Allied Wallet makes it simpler for companies to cater to a wide range of international clients by supporting transactions in over 100 currencies and providing localized payment options. For online businesses looking to expand outside of their domestic markets, this global focus is especially beneficial.

In order to provide services like credit card processing, fraud prevention, and recurring billing, the company has also formed strategic alliances with banks and payment networks worldwide. Everything from small startups searching for scalable solutions to high-volume enterprise operations is supported by its infrastructure.

That said, Allied Wallet has encountered regulatory challenges in certain regions, which have affected its public image. Still, the company maintains active operations and claims compliance with major global financial regulations, continuing to serve a wide variety of business verticals.

Core Services and Solutions Offered

Allied Wallet delivers a broad portfolio of services tailored for both digital and physical businesses. Central to its offering is payment processing—enabling merchants to accept major credit cards, debit cards, and an extensive range of alternative payment options. Its primary product, the merchant account, is bundled with tools like real-time analytics, fraud protection, and custom checkout pages.

For online retailers, Allied Wallet provides APIs and plug-ins for popular platforms such as Shopify, WooCommerce, and Magento. These features allow businesses to get started with minimal technical effort. Subscription billing and digital wallet capabilities are included, which is a big plus for SaaS providers and recurring payment models.

The PCI-compliant NextGen Payment Gateway, which offers features like tokenization, multi-currency support, and 3D Secure, is a noteworthy offering. These tools are useful for companies operating in high-risk markets because they are crucial for reducing chargebacks and preventing fraud.

Businesses can also explore Allied Wallet’s white-label services, which enable payment gateways and e-wallets with unique branding. For digital platforms or fintech startups wishing to provide smooth, branded payment experiences, this is perfect.

Some of the more advanced tools though, might be more expensive. Before making a commitment, businesses should thoroughly consider service tiers and any potential hidden fees.

User Interface and Dashboard Experience

Allied Wallet’s interface is practical but lacks modern design appeal. Once logged in, users are presented with a centralized dashboard showing transaction summaries, account balances, chargebacks, and performance analytics. While the platform provides all essential tools, the look and feel may seem dated compared to newer fintech services.

The layout is simple and functional, offering quick access to key areas such as reports, customer data, and transaction logs. For users who prioritize utility over aesthetics, the platform meets basic needs effectively. However, managing complex configurations or multiple business lines might require more navigation than ideal.

Real-time transaction tracking, which enables merchants to identify patterns or suspicious activity and generate personalized reports with multiple filters, is one of the benefits. These analytics tools provide useful information for day-to-day operations management.

That said, personalization options are minimal. The dashboard lacks customizable widgets and has limited responsiveness on mobile devices. For businesses that value sleek interfaces and user-friendly customization, this might be a drawback.

Overall, the dashboard is serviceable and functional—best suited for users who prioritize functionality over design flair.

Ease of Integration for Developers

Developers will find Allied Wallet reasonably accommodating when it comes to integration. It provides a range of SDKs and APIs compatible with popular programming languages like PHP, Java, and .NET, allowing for custom payment solutions on both web and mobile platforms.

For less technical users, the platform also supports prebuilt plug-ins for e-commerce systems like PrestaShop, Magento, and WooCommerce. These tools are helpful for a quick launch, although the most flexibility is offered through direct API integration, which allows for tailored experiences and advanced features.

The platform’s developer documentation is detailed but could benefit from a more intuitive structure. Experienced developers should be able to navigate it without issue, though beginners may require assistance. Allied Wallet does offer technical support for integration, but response times vary depending on account tier and location.

One useful feature for testing before going live is the presence of a sandbox environment. Final-stage testing may become more difficult, though, as some developers point out that the sandbox environment doesn’t always mirror real-time behaviors in the live system.

In short, developers with moderate to advanced skills will find enough tools to complete integrations efficiently. While not the most developer-friendly platform on the market, Allied Wallet provides sufficient infrastructure for most payment-related builds.

Payment Methods Supported

Allied Wallet excels in payment method diversity, which makes it attractive for businesses serving a global clientele. It supports all major credit and debit cards, including Visa, MasterCard, American Express, and Discover, as well as more than 100 alternative payment options.

These include e-wallets like Alipay and WeChat Pay, SEPA bank transfers, and regional mobile payment solutions. This versatility helps businesses convert international customers who prefer local payment options—often leading to better cart conversion rates.

The platform also supports recurring billing and subscription payments, which are key for membership-based services and SaaS companies. Allied Wallet’s multi-currency features and dynamic currency conversion allow users to pay in their native currency—improving overall customer satisfaction.

Although the variety of available payment methods is impressive, retailers should verify which features are enabled by default. Some might need manual setup or premium packages. Additionally, while support for cryptocurrencies is mentioned from time to time, it is not a core offering and seems to be limited.

For merchants targeting diverse global markets, Allied Wallet offers a flexible suite of payment choices—but always clarify what’s included in your service plan.

Security Features and Compliance

Security is a priority for Allied Wallet, and the company meets industry standards by being PCI DSS Level 1 compliant—the highest level of certification for payment processors. This ensures all transaction data is securely encrypted and stored using advanced protocols.

Allied Wallet’s use of tokenization and end-to-end encryption is one of its main advantages. These technologies lower the risk of breaches by substituting secure tokens for sensitive data. In order to decrease chargebacks, the platform also uses 3D Secure for extra security during cardholder authentication. Its fraud detection engine provides an additional line of defense. It employs machine learning to evaluate transactions in real time, identifying possible fraud and notifying merchants for review, though it is not as comprehensive as those provided by leading fintechs.

The company also adheres to major compliance protocols, including Anti-Money Laundering and KYC regulations. These help ensure businesses stay within legal boundaries, especially in tightly regulated regions.

However, Allied Wallet’s past legal issues around compliance enforcement warrant caution. Merchants should request the latest compliance certifications and maintain regular communication with the compliance team during onboarding.

Customer Support and Responsiveness

Customer service at Allied Wallet is a hit-or-miss experience. While the company advertises 24/7 availability via phone, email, and chat, actual user experiences range from excellent to frustrating. During onboarding, some merchants report helpful and responsive account managers. However, once the account is active, others mention slow replies and unhelpful resolutions—particularly for technical or fund-related queries.

Basic questions are usually addressed within a day, and the live chat can help resolve minor issues. For more complicated concerns like integration or chargebacks, merchants often rely on email chains or scheduled calls, which can be slow.

Although there is a searchable knowledge base, it is rather outdated and in need of frequent updates. The documentation may not be thorough enough for self-service users to troubleshoot complex issues. Growing unresolved problems are a common source of frustration. It often takes several follow-ups to reach higher-level support, which can be particularly annoying when there are delays or account freezes.

In short, Allied Wallet’s customer support is functional but inconsistent. Businesses with high support needs may want to clarify expectations in advance or opt for premium support if available.

Pricing Structure and Fees

Allied Wallet’s pricing structure is not publicly disclosed, which makes cost comparisons difficult for merchants. Instead of a standard rate card, the company provides custom quotes based on business type, industry, and risk level. General processing fees range between 2.7% and 3.9% per transaction, plus a flat fee. High-risk businesses may face steeper rates. Additional costs may include account setup, monthly fees, chargeback handling, and international transaction charges—all of which can add up.

The rolling reserve, which holds some of your money for a while to cover possible chargebacks, is one controversial issue. Despite being common in the sector, Allied Wallet has come under fire for its opaque policies. Smaller companies or those with tighter budgets may be concerned about the lack of transparent, up-front pricing. To prevent unforeseen costs, it is essential to review all contract terms and ask thorough questions during the sales process.

While potentially cost-effective for high-volume, global merchants, smaller companies may find more transparency and value with alternatives like PayPal, Stripe, or Square.

Mobile Experience and App Usability

Allied Wallet provides a mobile app and a responsive website, but these tools are not its strongest asset. The app—available on Android and iOS—lets users track transactions, view account balances, and receive alerts. The design is clean but basic. It covers essentials like daily revenue and customer data but lacks advanced features like report customization or settings control. Any deeper configuration still needs to be done through the desktop version.

Users appreciate the convenience of real-time updates, though some mention occasional app performance issues and slow notification delivery. The app interface also appears somewhat outdated compared to modern fintech solutions.

The app is more of a companion tool than a fully functional platform due to its limited functionality and infrequent updates. Nevertheless, it satisfies the demands of entrepreneurs who wish to quickly check their status while on the go. Power users won’t be impressed by the mobile experience, but it’s adequate for light monitoring and speedy transaction tracking.

Merchant Onboarding Process

Allied Wallet’s onboarding process is more thorough than many competitors, emphasizing due diligence and regulatory compliance. While this is beneficial from a risk-management standpoint, it can be time-consuming for new merchants.

The application needs detailed business data, such as ownership records, website addresses, financial statements, and identification documents. Client contracts or product samples may also be requested, depending on your industry. Timelines for approval vary. In high-risk categories, merchants report waiting one to two weeks, while others are approved in a matter of days. The compliance team might ask for more information, which would cause the delay to increase.

On the positive side, Allied Wallet provides onboarding support via account managers who guide applicants through documentation and setup. Still, communication gaps can occur, particularly when paperwork is missing or ambiguous.

Once approved, integration is typically smooth, with guides and plug-ins for popular e-commerce platforms. Developers also have access to technical support during the setup phase.

Settlement Times and Fund Accessibility

Allied Wallet’s fund settlement timeline depends on account type, business risk, and transaction volume. On average, payouts are processed weekly, with merchants receiving funds 3 to 7 business days after the transaction date. Lower-risk accounts may enjoy faster settlements, while high-risk businesses are more likely to face rolling reserves or extended hold times. Reserve policies, while industry standard, can be a source of frustration if not clearly communicated upfront.

Allied Wallet supports more than 100 currencies, but fees and exchange rates may affect final payouts. Feedback varies: some merchants report consistent, timely payouts, while others note delays and difficulty accessing held funds. Moreover, cross-border merchants may experience delays because of intermediary banking, currency conversion, or compliance checks. Reserve policy clarity is particularly important for avoiding cash flow issues.

Merchants should confirm all payout terms during onboarding and ensure those terms are documented in writing.

Pros and Cons of Allied Wallet

Pros:

Operates in 190+ countries and supports 100+ currencies.

Accepts a wide array of payment methods including alternative options.

Strong security via tokenization, PCI DSS, and fraud tools.

Developer support through APIs, sandbox, and plug-ins.

White-label solutions available for scalable infrastructure.

Cons:

No clear pricing on the website; may involve hidden charges.

Customer service experiences vary by case.

Onboarding can be lengthy and documentation-heavy.

Reserve and fund hold policies are not always transparent.

Platform and app design feels dated.

Who Should Consider Using Allied Wallet?

Allied Wallet is best suited for global merchants, especially those offering digital goods, educational platforms, and subscription-based services. Its broad payment method support and global infrastructure make it an excellent fit for businesses aiming to expand into international markets.

Additionally, platforms looking for white-label or custom-branded payment solutions, fintech startups, and enterprise clients find it appealing. However, Allied Wallet’s support variability, ambiguous pricing, and onboarding requirements might be burdensome for small or startup businesses. For people who value cost transparency and ease of use, platforms like Square, Stripe, or PayPal might be more appropriate.

High-risk merchants are accepted but should proceed cautiously. Understanding and documenting reserve requirements and support timelines is essential before committing.

FAQs

Is Allied Wallet suitable for small businesses and startups?

It depends. Startups with global customers or tech teams may find value in Allied Wallet’s international tools. However, small businesses looking for predictable pricing and simple onboarding may prefer platforms like Stripe or Square. If transparency and support are a priority, consider comparing options first.

How long does it take to receive payments via Allied Wallet?

Typically, funds are settled 3 to 7 business days post-transaction. Higher-risk accounts may experience longer delays or rolling reserves. International payments may take more time due to conversions or intermediary banks. Get clarity on your specific payout terms during onboarding.

Does Allied Wallet support cryptocurrency payments?

Not as a core service. While mentioned occasionally in its marketing, crypto support is limited and may require special arrangements. If cryptocurrency is a major part of your business, consider dedicated crypto processors like BitPay or CoinPayments instead.

AffiniPay Review

By 10topmerchantservices March 25, 2025

AffiniPay is a payment processing platform built specifically for professionals, with a strong emphasis on the legal sector. Unlike general-purpose solutions like Stripe or Square, It is uniquely structured to ensure compliance with trust accounting standards, making it a standout choice for law firms managing client funds. Its primary product, LawPay, is well-regarded for simplifying legal payment workflows while adhering to IOLTA (Interest on Lawyers’ Trust Accounts) compliance. Lets read more about AffiniPay Review.

The features, cost, usability, integrations, security, customer support, and general appropriateness for professional services of AffiniPay will all be covered in this thorough review. For legal and other professional firms, we want to know if AffiniPay is really the best option or if there is a more affordable option.

Even though AffiniPay offers many great features, such as secure processing, robust legal software integrations, and personalized payment links, it might not be the best option for all businesses. It may not be as adaptable for wider use due to its emphasis on legal professionals, and not everyone will find its fee structure appealing.

By the end, you’ll understand whether AffiniPay aligns with your needs or whether exploring other options could be more advantageous. This analysis will remain factual, neutral, and free from promotional influence.

Company Overview | AffiniPay Review

AffiniPay is a niche payment processor that tailors its services to law firms and other professional service providers. Unlike traditional processors aimed at mass markets, It prioritizes legal compliance and secure financial transactions for regulated industries.

History and Background

Since its founding in 2005, AffiniPay has expanded to provide services to thousands of professional practices and law firms. Its flagship product, LawPay, is designed to assist lawyers in managing client money while adhering strictly to IOLTA compliance and trust accounting regulations. It has grown over time to serve other regulated professions, including accountants and architects.

Mission and Key Offerings

AffiniPay’s mission is to deliver secure, easy-to-use, and compliant payment solutions tailored for professionals. Its offerings include:

Processing for major credit and debit cards

ACH and eCheck payment capabilities

Custom payment link generation and online invoicing

Integrations with platforms like Clio, QuickBooks, and MyCase

Industries Served

While AffiniPay supports various professionals, including architects and accountants, it’s most effective in legal environments. Businesses outside regulated industries may not benefit as much from its specialized features and could find more generic platforms more appropriate.

How AffiniPay Works

While adhering to stringent industry regulations, professionals can accept payments with AffiniPay. Its system is made for ease of use, legal compliance, and safe financial management, all of which are crucial for lawyers who oversee client retainers.

Payment Processing Workflow

The workflow is streamlined. Clients receive invoices with secure links, payments are processed through AffiniPay, and funds are routed to either trust or operating accounts based on the transaction. This separation is essential for law firms to meet ethical and legal obligations.

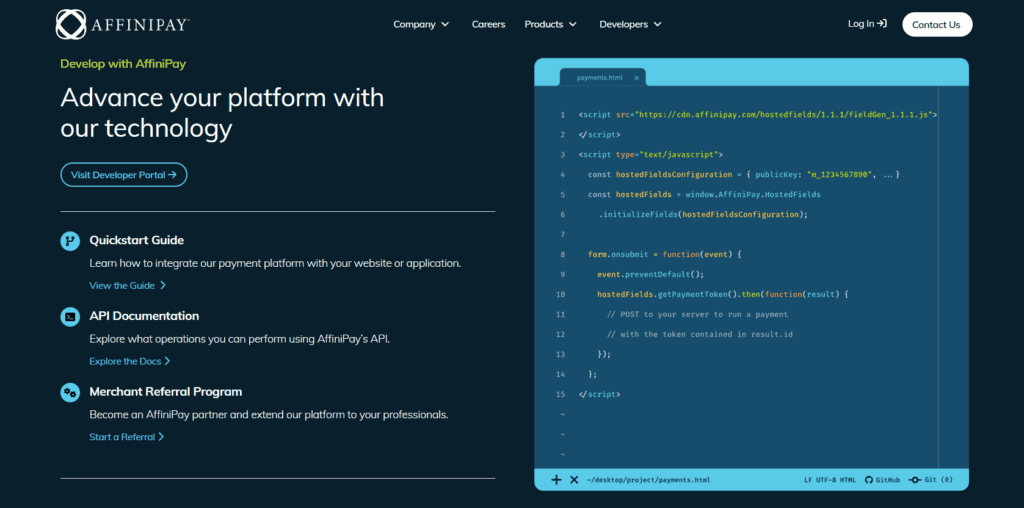

Integration with Professional Software

AffiniPay integrates easily with legal and accounting tools including Clio, PracticePanther, MyCase, QuickBooks, and Xero. These integrations automate tasks like invoice creation, payment tracking, and reconciliation, reducing manual effort and improving accuracy.

How Funds Are Handled (IOLTA Compliance for Law Firms)

Maintaining the separation of trust accounts is a must for law firms. By ensuring that customer funds are kept separate from business accounts, AffiniPay promotes IOLTA compliance and lowers the possibility of ethical violations.

Key Features of AffiniPay

It distinguishes itself through features specifically crafted for legal and professional service needs. These features ensure compliance, improve payment efficiency, and strengthen security.

Payment Processing Capabilities

AffiniPay supports Visa, Mastercard, American Express, Discover, and ACH payments. It offers a secure gateway that ensures fast and compliant processing of transactions.

Trust Accounting Compliance (IOLTA & ABA Rules)

By ensuring that client funds are automatically deposited into the right accounts and strictly adhering to IOLTA and ABA standards, the platform lowers the possibility of accounting errors.

Integration with Legal and Professional Software

Seamless integrations with software like Clio, MyCase, and QuickBooks streamline payment collection, automate reconciliations, and simplify invoice generation—all within the tools professionals already use.

Security & PCI Compliance

As a PCI Level 1 compliant provider, It uses advanced encryption, tokenized payments, and fraud detection to protect sensitive financial data and reduce chargebacks.

Custom Payment Links & Online Invoicing

Professionals can generate unique payment links, shareable via email or text, that enable clients to pay directly—no login needed. This makes the payment experience smoother for both parties.

Recurring Payments & Installment Plans

With AffiniPay’s automated recurring billing and installment options, businesses can effectively manage subscription-based services and ongoing retainers.

Because of these characteristics, It is a great choice for professionals under regulation who require safe, efficient, and legally compliant payment methods.

Pricing & Fees

AffiniPay’s pricing reflects its specialized nature. While generally comparable to other premium processors, some businesses may find it less cost-effective if they don’t need compliance features.

Breakdown of Processing Fees

There are no setup or monthly fees. The primary charges include:

Credit/Debit Card Transactions: 2.95% + $0.20 per transaction

ACH/eCheck Payments: Flat $2 per transaction

Chargebacks: A dispute fee may apply depending on the case

Monthly or Hidden Fees

Without monthly maintenance, PCI compliance, or contract cancellation fees, It offers a transparent fee structure. However, there may be additional fees for advanced integrations or unique features.

How AffiniPay Compares on Pricing

Stripe: 2.9% + $0.30 per transaction; lacks legal compliance tools

Square: 2.6% + $0.10; focuses on retail, not legal services

PayPal: 3.49% + $0.49; higher cost, limited legal integrations

Is AffiniPay Worth the Cost?

It provides excellent value for those in the legal industry and those who require trust compliance. However, when weighed against more flexible options, its higher fees might not be worth it for typical businesses.

Ease of Use & User Experience

AffiniPay is thoughtfully built for non-tech-savvy professionals. Despite offering advanced compliance tools, the platform remains intuitive and easy to navigate.

Platform Interface and Dashboard

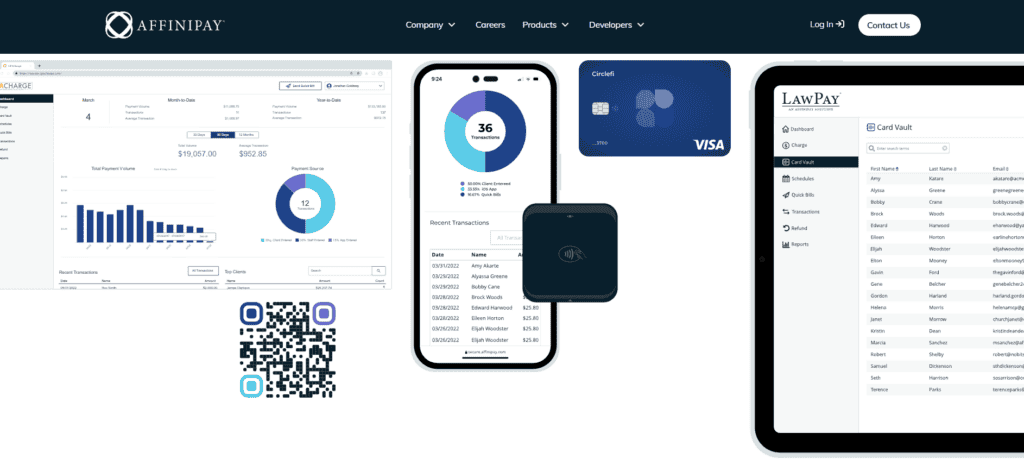

The dashboard presents real-time data, payment statuses, and client information in a clean layout. Professionals can easily create links, manage accounts, and track payments without getting overwhelmed.

Accessibility (Desktop & Mobile)

Being cloud-based, AffiniPay works well on desktop and mobile browsers. While mobile functionality is decent, it lacks a dedicated mobile app like Square or Stripe, which may be a limitation for some users.

Onboarding & Setup Process

Signing up involves submitting business details, linking bank accounts, and verification. AffiniPay also assists with onboarding, especially for law firms configuring trust accounts.

Learning Curve

The majority of users find the platform easy to use. Additional assistance may be needed by those who are not familiar with IOLTA regulations, but AffiniPay’s onboarding materials facilitate the process.

Overall User Experience

Although it could improve mobile support to match competitors’ convenience, AffiniPay strikes a balance between professional-grade tools and ease of use.

Security & Compliance

Security and legal compliance are central to AffiniPay’s value, making it an ideal platform for firms managing confidential financial data.

PCI Compliance & Data Encryption

AffiniPay is PCI Level 1 certified. It ensures every transaction is encrypted and tokenized, preventing data exposure and minimizing the risk of fraud.

Fraud Prevention & Risk Management

Key features include tokenized payments, AI-driven fraud detection, and mechanisms for resolving disputes, giving professionals peace of mind in financial matters.

Trust Accounting Compliance

The automatic fund segregation feature of AffiniPay complies with IOLTA and ABA regulations. This feature guards against legal violations and guarantees ethical management of customer funds.

Professional circles greatly trust AffiniPay as a payment processor because of its security and compliance measures.

Customer Support & Service

AffiniPay offers tailored customer support via phone, email, and an online help center. The team specializes in legal and trust accounting queries, adding substantial value for law firms.

Support is offered during regular business hours in the United States. Users often report knowledgeable and responsive assistance during operating hours, though the lack of 24/7 help can be a drawback. The help center provides self-service training webinars, comprehensive articles, and how-to manuals.

Overall, the support quality is well-regarded, though response times can be slower for less urgent issues, particularly over email.

Pros and Cons of AffiniPay

Pros

Tailored for professional services, especially legal firms

Strong trust accounting and IOLTA compliance

Integrates with legal and accounting platforms

High security with PCI Level 1 compliance and fraud tools

No long-term contracts or hidden fees

Easy-to-use interface and dashboard

Cons

Limited to U.S. professionals; no international support

Slightly higher processing fees than mainstream providers

No mobile app for on-the-go management

Not suitable for e-commerce or retail businesses

Lacks round-the-clock customer support

While powerful for compliance-heavy industries, AffiniPay’s niche focus may not suit businesses needing broader functionality.

How AffiniPay Compares to Competitors

AffiniPay stands apart for its legal focus but competes with popular processors offering different strengths.

AffiniPay vs. Stripe

Stripe offers flexible APIs, global payments, and reporting tools for digital businesses. It lacks trust accounting, making AffiniPay the better choice for law firms, while Stripe is ideal for global e-commerce and SaaS platforms.

AffiniPay vs. Square

Square is excellent for retail and point-of-sale, but it lacks compliance tools and legal software integrations. It is more advantageous for physical businesses, but AffiniPay is still the best option for legal professionals.

AffiniPay vs. PayPal

PayPal supports international transactions and peer payments but charges higher fees and lacks legal compliance. It is more secure and specialized for domestic professional use.

Who Should Use AffiniPay?

AffiniPay is best for firms needing compliant, secure payment solutions.

Best-Suited Industries

Law Firms – Ensure IOLTA compliance and secure client fund handling

Accounting & Finance – Ideal for consultants needing secure invoicing and ACH payments

Consultants – Benefit from automated billing and secure transaction flows

Healthcare Providers – Use HIPAA-compliant payment tools and recurring billing

Who May Not Benefit?

E-commerce & Retail – Platforms like Square and Stripe offer more retail-oriented features

High-Risk Businesses – AffiniPay doesn’t support industries with high chargeback rates

Global Businesses – Limited to U.S. operations with no international support

Final Verdict: Is AffiniPay Worth It?

For legal and professional service providers, It is a robust, compliance-focused payment processor. For professionals who require trust fund management and legal compliance, its specialized features make it well worth the cost, even though it is more expensive than some alternatives. Broader, less costly options might be advantageous for other businesses.

FAQs

Does AffiniPay support international transactions?

No, AffiniPay is limited to U.S.-based professionals and doesn’t offer international payment support. For global businesses, Stripe or PayPal may be more suitable.

Is there a contract or early termination fee?

AffiniPay has no long-term contract requirements and doesn’t charge early termination fees, allowing businesses flexibility with no binding commitments.

Can I use AffiniPay for a non-legal business?

Yes, It can be used by professionals like accountants and consultants, but it’s most beneficial for those requiring strict compliance. Retail or high-risk businesses should explore alternatives like Square or PayPal.

Adyen Review

By 10topmerchantservices March 22, 2025

Adyen is a premier global payment processor renowned for its advanced infrastructure, sophisticated fraud prevention mechanisms, and seamless omnichannel payment solutions. Established in 2006 in the Netherlands, It has evolved into a top-tier choice for businesses seeking a unified platform that supports various payment methods, including credit and debit cards, digital wallets, and local payment systems. Lets read more about Adyen Review.

Adyen addresses these requirements by providing a comprehensive platform that manages payment processing, risk management, and data analytics, removing the necessity for third-party intermediaries. In contrast to traditional processors, It links directly with card networks and local payment providers, reducing transaction expenses and improving reliability. This capability to avoid intermediaries also guarantees quicker settlements and a smoother payment experience for both merchants and customers.

Company Background and Global Reach | Adyen Review

As businesses continue to expand their digital presence and embrace cross-border commerce, having a payment processor that seamlessly handles multiple payment methods is crucial. Adyen’s commitment to providing a streamlined, scalable infrastructure allows businesses to process transactions in different currencies without friction. This makes it particularly beneficial for e-commerce companies, hospitality brands, and multinational enterprises looking for a robust and flexible payment solution.

Origins and Evolution

Founded in Amsterdam by payment industry veterans Pieter van der Does and Arnout Schuijff, Adyen was built to modernize the outdated financial infrastructure. The name “Adyen,” meaning “Start Over” in Surinamese, reflects its mission to revolutionize payment processing by eliminating inefficiencies and dependencies on legacy banking systems.