First American Payment Systems Review

By 10topmerchantservices April 21, 2026

First American Payment Systems is one of the longer-tenured names in American merchant services, founded in 1990 and headquartered in Fort Worth, Texas. For more than three decades, the company built a sizable business providing credit card processing, POS systems, eCommerce tools, and ACH payment solutions to small and medium-sized businesses across the United States. In June 2021, Deluxe Corporation acquired the company for $960 million, and it now operates as First American by Deluxe, sitting within Deluxe’s broader payments segment. Lets read more about First American Payment Systems Review.

Before it was acquired, First American processed more than $40 billion per year of payments on behalf of over 159,000 merchants located in the Americas and Europe. These figures illustrate that the company was quite large-scale indeed. At the same time, First American had quite a few troubles with regulators during its history. The Federal Trade Commission brought a suit against First American and two of its sales affiliates in July 2022 charging the company with fraudulent practices such as undisclosed charges, deceptive cancellations, and forced bank withdrawals. Although First American agreed to pay $4.9 million to the regulator without admitting guilt, the FTC returned over $2.6 million to small businesses in February 2025.

Company Background and Market Position | First American Payment Systems Review

First American Payment Systems was founded in 1990 by Neil Randel, making it one of the older merchant services companies in the United States. Based in Fort Worth, Texas, the company spent over three decades building a diversified payment technology business before its acquisition by Deluxe Corporation in June 2021 for $960 million, a deal that signaled Deluxe’s strategic push into the merchant services market.

Under the Deluxe umbrella, First American operates as First American by Deluxe, retaining its brand identity while benefiting from Deluxe’s distribution network, which includes thousands of financial institution clients and millions of small business customers. The combined payments segment generates over $600 million in annual recurring revenue, placing the entity among the larger players in US merchant services.

The company has historically operated across multiple business names and affiliates, including FirstPay.net, Secur-Chex, FirstAdvantage, Merrimac Capital, and FirstFund ACH. Its distribution network includes independent sales organizations, independent software vendors, and financial institutions. This multi-channel sales model has been a source of both scale and controversy, as the quality of merchant interactions has varied considerably depending on which sales channel was involved.

From a market positioning standpoint, First American targets a broad range of business types including retail, restaurant, healthcare, hospitality, government, and nonprofit sectors. It does not position itself as a niche or industry-specific processor, instead competing as a full-service merchant account provider with in-store, online, and mobile capabilities across verticals.

Core Payment Processing Capabilities

At its foundation, First American Payment Systems provides full-service electronic payment processing, covering credit card and debit card acceptance across all major card networks, as well as ACH and electronic check processing. These capabilities are available across in-store, online, and mobile environments, making it a broadly functional option for merchants with multi-channel sales operations.

Credit and debit card processing supports standard authorization, clearing, and settlement workflows. The platform connects to major backend processors, giving merchants access to reliable transaction infrastructure. ACH processing, offered through the FirstFund ACH division, enables direct bank-to-bank transfers and is particularly useful for businesses handling recurring charges, invoice-based billing, or higher-value B2B transactions.

Another service provided by First American involves the processing of checks offered by its Secur-Chex unit, which provides another payment type option that is still used by many merchant organizations, especially the B2B segment and older consumers. The variety of payments allows First American to have an operational advantage since it would be able to satisfy all payment preferences of merchants using just one provider.

The remote deposit of checks can also be done online without the necessity of traveling to the bank office. This service may be important to companies that have many checks processed each day. For the majority of businesses, there are no problems with basic services provided by this company, which may indicate its experience in the market for more than three decades.

POS Systems and Hardware

First American offers a range of POS solutions targeted at different business types and environments. The product lineup includes the proprietary 1stPayPOS Pro tablet-based system, as well as integrations with the Clover POS platform, which has become one of the most widely recognized POS solutions in the US market.

The 1stPayPOS Pro is a tablet-based system designed to handle payment acceptance, employee time tracking, inventory management, sales reporting, and customer data management. This combination of functions makes it more than a simple payment terminal. For retail and food service businesses that want operational management tools alongside payment processing, the integration of these functions into a single system has practical value.

Clover POS can be purchased independently within the First American product line. The Clover system is quite reputable, featuring an impressive app ecosystem along with a versatile suite of hardware options that range from simple credit card terminals to comprehensive countertop solutions. But merchants need to be cognizant that Clover systems do not interface with other hardware families, thus opting for Clover limits the merchant to their specific hardware lineup.

The software products offered by First American through their Deluxe partner are interoperable with popular hardware systems such as Ingenico, Dejavoo, and PAX. This ensures merchants have more options when it comes to selecting hardware products rather than being restricted to a single hardware provider. Business owners considering POS offerings by First American are encouraged to ask for transparent costs regarding both hardware and software.

Mobile Payment Solutions

For businesses that operate outside fixed locations, First American offers mobile payment capabilities through its 1stPayMobile product. This solution enables merchants to accept credit and debit card payments through a smartphone or tablet, using a card reader that connects to the device. Functionality includes card swipe authorization, digital signature capture, and email receipt delivery, covering the basic requirements most mobile merchants need.

1stPayMobile is designed for types of business operations conducted out of an in-place checkout, such as service providers, event sellers, tradeshow participants, and field businesses. Having the capacity to process card payments on-site versus invoicing clients afterward creates cash flow benefits for this kind of operation.

Contactless card acceptance capabilities are also built into the platform, since accepting payments from contactless cards is no longer a high-end capability, but a basic expectation from the majority of merchants. This means contactless card payments as well as mobile wallets.

Merchants need to use caution with the mobile transaction pricing model since it can vary. As with other aspects of the First American platform, mobile payment pricing is private and cannot be found on public websites and must be acquired from a First American sales person. Questions merchants should ask include any per-transaction fees for mobile payments, monthly minimums on mobile accounts, and the comparison of pricing between in-store and mobile transaction pricing within the same account.

eCommerce and Online Payment Tools

First American provides a range of online payment capabilities through its FirstPay.net gateway and eCommerce integration tools. These allow merchants to accept payments through websites, generate customizable payment pages, and manage online transactions through a virtual terminal environment.

The eCommerce offering includes shopping cart integration, allowing merchants to connect the payment gateway with their existing online store. A customizable payment page builder gives merchants the ability to create branded checkout experiences without requiring extensive custom development. Virtual terminal functionality supports manual transaction entry, useful for phone and mail order businesses that take payment information outside a standard checkout flow.

Recurring billing can be accessed under the eCommerce capabilities offered by the platform, where the merchant will be able to configure automated charging schedules for products that involve monthly subscriptions or installment payments. This applies to any merchant whose business model involves subscription services, allowing such transactions to occur with minimal hassle on their part.

There are development capabilities available through the platform that can facilitate API integrations in cases where a business wants more control over their payments process. As per the platform itself, it is compatible with APIs, along with documentation, sample code/SDKs, and a sandbox. This gives it the ability to cater to needs in terms of technical integration, albeit not as extensive an ecosystem compared to platforms designed from the get-go as development-focused solutions.

Security and Fraud Prevention

First American packages its security capabilities under the 1stPaySecure product umbrella, which covers a range of standard data protection and fraud prevention measures. The security offering includes encryption, tokenization, breach insurance, and PCI compliance assistance, representing a reasonably comprehensive baseline for merchants who need to protect cardholder data across in-store and online environments.

Tokenization replaces sensitive card data with a non-sensitive token at the point of transaction, meaning actual card numbers are not stored in the merchant’s systems or transmitted in plain text. Encryption protects data in transit, reducing interception risk during payment processing. These two measures together represent industry standard practice for modern payment security.

PCI compliance assistance is included as part of the security offering, which is a practical benefit for smaller merchants who may not have dedicated IT or compliance resources. Navigating PCI DSS requirements can be challenging for businesses without payment security expertise, and having processor-level support for the compliance process reduces that burden.

Breach insurance adds an additional layer of financial protection in the event of a data security incident. This is a less common inclusion in standard processing agreements and represents genuine added value, particularly for smaller businesses for whom the financial consequences of a breach could be disproportionately severe.

Fraud detection tools are integrated into the payment security layer, though the specific technical details of these tools are not extensively documented in public-facing materials. Merchants with elevated fraud risk profiles should ask specifically about the rules and monitoring capabilities available before assuming the included tools will meet their requirements.

Gift Cards and Loyalty Programs

First American offers gift card and loyalty program capabilities through its FirstAdvantage product. This is a feature set primarily designed for small to medium-sized businesses that want to offer customers additional incentives to return and spend, without the complexity of enterprise-grade loyalty platforms.

Gift cards give organizations the ability to offer prepaid value cards which can be redeemed later by consumers in order to make future purchases. Gift cards can be considered an already proven way of making money for retail and food service organizations since they help attract customers to stores, introduce new customers to the store, and save margins during discount periods. The fact that gift cards are processed via the same platform as regular payments makes the process of managing these cards much simpler for business owners.

The loyalty module provided in FirstAdvantage gives merchants an opportunity to create various reward schemes to motivate clients’ purchase behavior. Rewards may include any combinations of points, visits, or spending thresholds required by each individual organization. A properly designed loyalty program can help retain customers in local competition.

It should be emphasized that although quite flexible, the loyalty solution provided by FirstAdvantage is not aimed at big enterprises, but rather at small businesses. Therefore, companies with more complicated loyalty program needs, multi-location operations, or higher loyalty transaction volume should think about whether this platform will be sufficient for them or not.

Pricing Structure and Fees

Pricing is one of the most consequential and, in the case of First American, most complicated aspects of evaluating this provider. The company does not publish its pricing publicly, which is common in the merchant services industry but creates a meaningful barrier to comparison shopping for merchants.

From what is available through merchant feedback and independent reviews, First American appears to use a tiered pricing model. Tiered pricing categorizes transactions into qualified, mid-qualified, and non-qualified tiers, with different rates applied to each. This approach can be straightforward to understand initially, but it often results in higher effective costs than interchange-plus pricing, because the processor controls how transactions are categorized and what rates apply to each tier.

Known fee benchmarks from merchant reports include standard contracts that carry either a $95 annual fee or a $25 monthly minimum, variable monthly statement fees of $20 or more, and various additional charges for technical support, batch processing, and gateway services. A three-year contract term appears to be standard, with an early termination fee historically cited at $495.

Next-day funding is available, though this feature carries additional fees. Monthly fee increases for existing customers have also been reported, meaning the rate a merchant agrees to at sign-up may not remain stable over the life of the contract. Merchants should request a complete written breakdown of all fees before signing any agreement, ask specifically about rate adjustment provisions, and understand whether the tiered pricing structure is negotiable.

Contract Terms and Merchant Agreements

Contract terms are an area where First American has attracted significant and documented criticism, and this section warrants particular attention from any merchant considering the platform. Standard merchant agreements appear to involve a three-year contract term with automatic renewal provisions. The $495 early termination fee has been a consistent point of complaint in merchant feedback, and the FTC’s 2022 lawsuit specifically cited the company’s practice of promising easy cancellation during the sales process while burying three-year obligations and exit fees in fine print that was difficult to locate within the online enrollment system.

The FTC complaint also detailed how First American’s online enrollment system allowed merchants to click accept on contracts without requiring them to first click through to review the actual terms. Key contractual provisions, including the three-year commitment, automatic renewal terms, and cancellation fees, were embedded in densely formatted documents accessible only through separate hyperlinks. For merchants with limited English proficiency, whose sales conversations were conducted in their native language while documentation was available only in English, this created a serious informational imbalance.

As part of the FTC settlement, First American agreed to stop obscuring key contract terms, improve the transparency of its cancellation process, and stop making unauthorized withdrawals from merchant bank accounts. Merchants engaging with First American today should verify that these reforms are reflected in their actual agreement, request all contract documents in advance, review them carefully, and confirm in writing what the cancellation process and associated fees involve before activating service.

The FTC Lawsuit and Settlement: What Merchants Need to Know

The 2022 FTC action against First American Payment Systems is not a footnote in this review. It is a material fact that any merchant evaluating this provider should understand in detail. On July 29, 2022, the FTC filed a lawsuit against First American Payment Systems and two of its sales affiliates, Think Point Financial LLC and Eliot Management Group LLC, alleging violations of Section 5 of the FTC Act and the Restore Online Shoppers’ Confidence Act.

The core allegations covered four distinct practice areas: deceptive pricing pitches that promised low or zero monthly fees while concealing subsequent fee increases; an online enrollment system that hid the three-year contract obligation, automatic renewal terms, and cancellation fees; cancellation practices that imposed the $495 exit fee on merchants who had been verbally promised fee-free cancellation; and unauthorized bank withdrawals from merchant accounts even after merchants had revoked consent, in some cases made under different business names to evade stop-payment orders.

First American settled the lawsuit without admitting liability, paying $4.9 million. Of that total, $2.6 million was distributed directly to affected businesses, with the FTC sending checks to 5,588 merchants in February 2025. The settlement also required operational reforms including transparent disclosure of contract terms, a simplified cancellation mechanism, and a prohibition on unauthorized withdrawals.

The company publicly denied the FTC’s characterization of its practices and stated it settled to avoid the cost of prolonged litigation. Merchants should weigh this history in the context of their own due diligence, recognizing that the reforms required under the settlement create a changed operational environment relative to the period covered by the FTC complaint.

Customer Support

Customer support at First American presents a genuinely mixed picture that reflects the gap between institutional capability and on-the-ground experience for individual merchants. The company operates a US-based customer call center available 24/7/365 and has received industry recognition for its call center performance, including awards from the Association of TeleServices International. That level of infrastructure investment is not trivial and reflects a real commitment to support availability.

However, merchant feedback from independent review platforms and the BBB tells a more complicated story. Common complaints include long wait times for complex issues, difficulty resolving billing disputes, and inconsistent communication around fee changes and contract terms. These issues are particularly acute when the underlying problem involves a contractual dispute or an unauthorized charge, where the resolution process requires escalation beyond front-line support staff.

The BBB profile for First American carries extremely low customer ratings despite an A+ or B-level letter grade, which reflects the distinction between how the BBB scores companies on procedural criteria and how actual customers rate their experiences. The volume of customer complaints touching on similar themes, specifically unexpected fees and difficulty canceling services, suggests systemic patterns rather than isolated incidents.

For merchants with straightforward operational questions, the 24/7 availability and generally responsive front-line support can be adequate. For merchants navigating contract disputes, fee discrepancies, or cancellation issues, the support experience is more likely to be frustrating. Prospective merchants should establish a clear escalation path before they need it.

Reporting and Analytics Tools

First American provides online reporting capabilities through its merchant portal, allowing merchants to view statements, track transaction activity, and generate customized reports. Real-time transaction monitoring is available, giving businesses visibility into sales activity as it occurs rather than relying solely on end-of-day or end-of-month summaries.

Standard reporting features include transaction history, settlement reports, and the ability to generate custom reports based on date ranges, transaction types, and other parameters. For most small and medium-sized businesses, this level of reporting covers the daily reconciliation and financial oversight needs they are most likely to encounter in practice.

The Deluxe Payment Platform, introduced following the acquisition, consolidates data from multiple payment products into a centralized merchant and partner portal with a single sign-on access point. This is a useful improvement for merchants using more than one First American or Deluxe payment product, as it reduces the fragmentation of logging into separate systems for different functions.

Where the reporting falls short of more modern platforms is in the area of advanced analytics and business intelligence. Deeper analysis of customer behavior, transaction trends, or revenue forecasting requires exporting data to external tools rather than running that analysis natively within the platform. This is not an unusual limitation for a traditional merchant services provider, but businesses that rely heavily on payment data for strategic decision-making should assess whether the native reporting meets their needs.

Strengths, Limitations, and Who It’s Best For

First American Payment Systems by Deluxe is a large-scale, broadly functional merchant services provider with genuine operational depth. Its omnichannel coverage across in-store, mobile, and online environments, combined with a wide range of supported payment types, makes it technically capable of serving businesses with diverse transaction needs. The security infrastructure, breach insurance inclusion, and 24/7 support availability represent real investments in merchant service quality.

However, the limitations are significant and well-documented. The FTC lawsuit and settlement represent a serious regulatory finding that cannot be treated as minor. Pricing lacks public transparency, tiered pricing models typically cost more than interchange-plus alternatives, and the three-year contract with an early termination fee creates meaningful commitment risk. Merchant feedback consistently identifies unexpected fees, difficult cancellations, and inconsistent support quality as recurring pain points.

Following the Deluxe acquisition, the company has undertaken platform improvements and made operational commitments under the FTC settlement order. Whether these changes have translated into a materially better merchant experience is something prospective customers should assess through direct conversations, careful contract review, and consultation with current or former users before committing.

The merchants best positioned to work with First American by Deluxe are those who need a full-service provider across multiple payment channels, who have the internal capacity to review contracts carefully, negotiate terms, and monitor their billing statements regularly. Businesses that process higher volumes and have leverage in negotiations may be able to secure more favorable terms. Smaller merchants with limited administrative bandwidth, those in early-stage businesses, or those with limited English proficiency should approach the platform with particular caution and, ideally, seek third-party contract review before signing.

FAQs

Q1. Is First American Payment Systems still operating as an independent company, or has it been fully absorbed into Deluxe?

Following Deluxe Corporation’s $960 million acquisition in June 2021, First American Payment Systems continues to operate as a branded entity within Deluxe’s payments segment, now called First American by Deluxe. The company retains its Fort Worth, Texas headquarters and continues to serve merchants under its own brand.

However, the underlying technology infrastructure, distribution, and product development are increasingly integrated with Deluxe’s broader payments platform, including a centralized merchant portal with single sign-on access across Deluxe payment products. Merchants engaging with First American today are effectively entering a relationship with the Deluxe payments organization, and the direction of product development and service standards will be shaped by Deluxe’s strategic priorities going forward.

Q2. What should a merchant do if they believe First American has charged unauthorized fees or made unauthorized withdrawals from their account?

Merchants who experience unauthorized charges should take several immediate steps. First, document all transactions with dates and amounts, and gather any written communications or agreements that address the fees in question. Second, contact First American’s customer service directly and submit a formal written dispute, requesting a response within a specific timeframe. Third, if the charges involve bank account withdrawals, contact your bank immediately to place a stop payment order and report the unauthorized activity. Fourth, if the issue is not resolved, the FTC remains an appropriate reporting body, and the Consumer Financial Protection Bureau also accepts payment processing complaints.

Given the history of the FTC case and the reforms required under the settlement order, merchants have regulatory recourse available to them beyond the company’s internal dispute process.

Q3. How does First American’s pricing compare to more transparent payment processors, and is it negotiable?

First American uses a tiered pricing model, which is generally considered less transparent and often more expensive than interchange-plus pricing used by many competing providers. Tiered pricing groups transactions into rate categories that the processor controls, which can result in a higher portion of transactions being classified at elevated rates. Monthly fees, statement fees, batch fees, and technical support fees add to the overall cost beyond the headline transaction rate. Pricing is not published publicly, meaning merchants must engage with a sales representative to obtain quotes.

It is negotiable, and merchants processing higher volumes typically have more leverage to negotiate lower rates and reduced fees. Before signing, merchants should request an interchange-plus pricing alternative if available, ask for a detailed breakdown of every fee line, and compare the total estimated cost across multiple providers rather than relying on the quoted transaction rate alone.

Exact Payments Review

By 10topmerchantservices April 14, 2026

Exact Payments has quietly carved out a specific and defensible niche in the crowded payment processing industry. Rather than competing head-to-head with generalist processors like Stripe or Square, the company has focused its energy on a narrower but increasingly valuable problem: helping SaaS businesses embed payments directly into their platforms without the costly, time-consuming process of building payment infrastructure from scratch. Lets read more about Exact Payments Review.

Founded in 1999 and headquartered across Scottsdale, Arizona and Vancouver, Canada, Exact Payments has spent over two decades refining its approach to payment technology. In 2020, private holding company Platform Partners LLC acquired a controlling stake, bringing in payments industry veteran Phil Levy as CEO, a move that signaled a sharper strategic focus on the SaaS and embedded payments market.

Today, the platform processes over one billion transactions and more than $150 billion in gross payment volume annually, serving clients that include Cineplex, Allianz, Levi’s, and Carfax. These are not small, experimental deployments; they represent real-world, high-volume payment operations running on Exact’s infrastructure.

Company Background and Market Position | Exact Payments Review

Exact Payments was founded in 1999, making it one of the longer-standing players in the digital payments space; a fact that tends to get overlooked given how much attention goes to newer fintech entrants. The company operated for over two decades building payment technology before a significant ownership change in late 2020, when Platform Partners LLC, a Houston-based private holding company, acquired a controlling interest.

That acquisition brought meaningful leadership changes. Phil Levy was appointed CEO, bringing over 20 years of payments industry experience from companies including Fiserv/First Data, Elavon, Silicon Valley Bank, and Chase Paymentech. Rahul Gupta, another industry veteran with senior roles at Fiserv and RevSpring, joined as Chairman of the Board. The original founders, Peter Fahlman, Brian Archer, and Gersham Meharg, retained equity and continued contributing to software development, operations, compliance, and security.

This leadership structure reflects a company that blends institutional payments knowledge with the technical depth of its founding team. It’s a combination that matters when evaluating whether a payments platform is built on solid fundamentals or assembled quickly to chase market trends.

In terms of market positioning, Exact Payments occupies a focused lane: payment facilitation technology for SaaS businesses. It is not trying to be everything to everyone. Its processor integrations in the US and Canada, including Elavon, Fiserv, Global Payments/TSYS, Chase Canada, and Moneris, give it strong regional coverage while maintaining the reliability that enterprise clients expect. For businesses operating primarily in North America, this network is a practical strength rather than a limitation.

Core Payment Processing Capabilities

At its foundation, Exact Payments handles the essential mechanics of electronic payment processing: transaction authorization, clearing, and settlement. These are the unglamorous but mission-critical functions that every merchant depends on daily, and getting them right consistently matters far more than headline features.

The platform supports credit and debit card processing across major card networks, giving merchants broad coverage for consumer payment preferences. Beyond card payments, Exact payments also supports ACH transactions, a capability that becomes particularly valuable for SaaS platforms managing subscription billing, invoicing, or B2B payment flows. ACH typically carries lower transaction costs than card payments, making it an attractive option for businesses processing high volumes of recurring charges.

What sets apart Exact’s payment processing services is how simplicity outweighs complexity. It is designed for seamless handling of regular payment processes as opposed to complex features that come with added risk. While such an approach may seem simplistic, it is actually what most SaaS companies want as payment processing should run flawlessly in the background and not be at the forefront of their operations.

Exact also boasts 99.99% uptime and transaction processing time of less than one second, which makes for impressive metrics among software companies that suffer user churn in case of failed payments. Such metrics are made possible by the platform’s present client portfolio, which comprises several big players from the entertainment, insurance, retail, and automotive industries. For firms that consider reliable payments to be the bare minimum requirement, Exact can boast strong core payment processing services.

PayFac-as-a-Service: The Core Differentiator

If there is one area where Exact Payments genuinely stands apart from many of its competitors, it is the PayFac-as-a-Service model. Payment facilitation, or “PayFac”, allows a software platform to act as a master merchant, onboarding sub-merchants under its umbrella and processing payments on their behalf. Historically, becoming a PayFac required significant capital investment, compliance overhead, and technical infrastructure. Exact Payments removes most of that barrier.

Through its PayFac-as-a-Service offering, SaaS companies can offer payment acceptance to their own customers without registering as a full Payment Facilitator themselves. Exact handles the compliance, underwriting, risk management, and processor relationships in the background. The SaaS platform gets the benefits, increased product stickiness, a new revenue stream from payment margins, and a better end-user experience, without taking on the full regulatory burden.

Exact claims this model can increase a customer’s lifetime value by up to five times, which is a significant assertion. The logic is sound: when payments are embedded directly into a software workflow, customers are less likely to churn, and platforms earn revenue on every transaction processed. It transforms payments from a cost center into a profit driver.

The onboarding process for sub-merchants is handled through Exact’s Onboarding API. Platforms submit merchant application data programmatically, automated underwriting evaluates the application in near real-time, and a webhook notification confirms approval, meaning new merchants can be live and processing payments within hours rather than days. For SaaS companies scaling their merchant base quickly, this automation is a genuine operational advantage worth taking seriously.

Supported Business Types and Industries

Exact Payments positions itself primarily as a solution for SaaS companies, but the underlying payment infrastructure supports a broad range of business types and industries. Its client list spans entertainment (Cineplex), insurance (Allianz), retail (Levi’s), and automotive data (Carfax), a cross-section that demonstrates the platform’s versatility across different transaction environments and business models.

For SaaS platforms serving vertical markets, think property management software, healthcare scheduling tools, field service applications, or legal practice management systems, Exact’s embedded payments model is particularly well-suited. These platforms often have captive user bases that would benefit from integrated payment acceptance, but the operators lack the resources or expertise to build payment infrastructure independently.

Merchants who have traditional needs when it comes to money transfer solutions may also take advantage of the solution provided by Exact Payments to process cards and ACH payments. It is only fair to note that the service might not be perfect for some types of companies. Specifically, those involved in industries that may be considered risky, like gaming, adult-related services, specific nutraceuticals or firearm sales, might not benefit from this service because the merchant will go through underwriting procedures.

International payment processing, which involves unique requirements from other countries, might not be an option for merchants on this platform. The fact is that Exact Payments relies on North American processors, meaning that the company only serves businesses within the US and Canada. Again, it is nothing extraordinary considering the size of this provider, but it is something that should be taken into account.

API and Developer Tools

For SaaS companies evaluating Exact Payments, the quality of developer tooling is often the most important deciding factor. A payments platform that is difficult to integrate, poorly documented, or unstable under load creates downstream problems that are expensive to fix. Exact’s approach here reflects a genuine investment in the developer experience, though with some caveats worth noting.

The platform offers a modern REST API architecture that covers the full payments lifecycle, from merchant onboarding and payment acceptance through to funding, reconciliation, and reporting. A single API integration is designed to give SaaS platforms access to the complete infrastructure stack, which reduces the technical complexity of managing multiple vendor relationships.

Exact also offers a sandbox full-stack testing environment, where development teams can perform rigorous testing before going into production. This isn’t just an extra offering – a comprehensive sandbox testing environment will drastically lower the chances of payment problems after a launch and give confidence to engineering teams when making iterations. Add an open developer portal and round-the-clock technical support provided by professional developers to the mix, and Exact’s developer offering can be seen as pretty decent compared to its competitors.

Lastly, Exact offers low-code payment forms for platforms looking to add payment functionality with minimal coding effort. This serves as an option for small-scale SaaS providers or companies operating with limited development capabilities. However, if a business needs highly tailored payment functionality or has any other special cases, extensive development work might still be required. Overall, Exact’s developer offerings are good, yet somewhat limited compared to fully developer-centric solutions such as Stripe.

In-Person and Online Payment Solutions

Exact Payments supports payment acceptance across both physical and digital environments, which matters for SaaS platforms whose end-merchants operate in omnichannel settings. The platform covers the standard range of in-person payment methods, chip cards, contactless payments, and magnetic stripe transactions, ensuring compatibility with modern consumer preferences without requiring merchants to retire older hardware immediately.

For online transactions, the platform offers hosted payment pages, ecommerce checkout integrations, and payment gateway connectivity. These tools allow businesses to accept payments through websites and digital platforms without exposing sensitive cardholder data in the process. Tokenization and encryption handle the security layer, keeping compliance obligations manageable for merchants who may not have dedicated security teams.

A virtual POS feature extends payment acceptance to remote or phone-based transactions, which is useful for service businesses, B2B operations, or any merchant that occasionally needs to process a payment outside a standard checkout environment. Payment buttons and invoice-based payment links further expand the range of collection methods available.

Where Exact’s omnichannel coverage becomes particularly valuable is in SaaS contexts where a software platform’s merchants operate across multiple sales channels. A field service software company, for example, might need its users to accept payments in-person at a job site, online through a customer portal, and via invoiced billing, all through a single integrated system. Exact’s infrastructure can support that combination without requiring separate provider relationships. That said, merchants with highly sophisticated in-store POS requirements, such as full inventory management or advanced retail analytics, may find the hardware and POS feature set more functional than feature-rich.

Onboarding and Merchant Account Management

One of the more practical strengths of the Exact Payments platform is the onboarding experience, particularly for SaaS companies managing large numbers of sub-merchants. Traditional payment processor onboarding is notoriously slow, manual reviews, paper-based documentation, and multi-day approval windows are common complaints in the industry. Exact’s approach addresses this directly.

The Onboarding API allows SaaS platforms to submit merchant application data programmatically. Once submitted, Exact’s automated underwriting system evaluates the application and returns a near real-time decision. Upon approval, a webhook notification delivers account credentials, and the merchant is live and ready to process payments, in many cases within the same business day. For platforms scaling their customer base rapidly, this automation eliminates a significant operational bottleneck.

From the point of view of a sub-merchant manager, there are means for controlling merchant operations, managing account statuses, and addressing compliance issues in a more convenient manner. For PayFac arrangements, platform operators take upon themselves some responsibility in regard to how onboarded merchants act.

One of those cases when merchants need to ensure they do their homework is in connection with automation-based decisions and associated underwriting rules and risks levels. Automation makes merchant onboarding very quick, however, in some cases, standardized criteria may not work well, so businesses or sub-merchants that fall into a gray area should contact Exact’s team rather than use the automated process. On the whole, onboarding is really an asset of this solution and a strong competitive advantage because other platforms tend to follow the conventional process to onboard their customers.

Pricing Structure and Fees

Pricing transparency is one of the most common friction points in the payment processing industry, and Exact Payments is not entirely immune to this criticism. Like many B2B payment platforms, Exact does not publish a standard rate card publicly. Pricing is negotiated based on factors including transaction volume, business type, integration model, and the specific processor relationship involved.

For SaaS platforms using the PayFac-as-a-Service model, the revenue dynamic is somewhat different from traditional merchant processing. The SaaS platform earns a margin on transactions processed through its embedded payments integration, essentially taking a share of the payment revenue generated by its own customers. Exact facilitates this revenue-sharing structure, which can make the economics attractive for platforms with sufficient transaction volume.

For merchants using Exact for standard payment processing, pricing models may include interchange-plus structures or tiered pricing depending on the agreement. Interchange-plus is generally more transparent, merchants pay the actual card network cost plus a fixed processor markup, while tiered pricing can simplify billing but sometimes obscures the true cost of specific transaction types.

Merchants and platform operators should request full fee breakdowns before signing agreements. This includes monthly platform fees, per-transaction charges, gateway fees, chargeback fees, and any compliance-related costs. The absence of a public pricing page means that comparison shopping requires direct outreach, which adds friction to the evaluation process. That is a legitimate limitation worth acknowledging, particularly for smaller businesses that want pricing certainty upfront. Working with a knowledgeable account representative who can walk through the full cost structure is the best way to navigate this.

Contract Terms and Merchant Agreements

Contract terms in the payment processing industry deserve careful attention, and Exact Payments is no exception to this general caution. While the platform offers genuine operational value, the legal and commercial terms of any merchant agreement should be reviewed thoroughly, ideally with input from someone familiar with payments contracts, before committing.

Key areas to scrutinize include contract length, automatic renewal clauses, and early termination fees. Some processors lock merchants into multi-year agreements that automatically renew unless the merchant provides written cancellation within a narrow window. Exit fees for breaking these agreements can be material, particularly for businesses with high transaction volumes. Understanding these terms upfront prevents unpleasant surprises later.

For SaaS platforms operating under a PayFac-as-a-Service arrangement, the contractual relationship is more complex than a standard merchant agreement. The platform operator takes on certain responsibilities around sub-merchant compliance and risk management, and the agreement should clearly define what those obligations are and where Exact’s responsibilities begin and end.

One positive aspect is that Exact’s leadership team has deep industry experience, which typically means a more professionally structured onboarding and contracting process than smaller, less established processors. However, professionalism does not automatically mean favorable terms, merchants should still negotiate where possible, particularly around fee caps, termination provisions, and service level commitments. Startups and early-stage SaaS companies in particular should pay close attention to flexibility provisions, since growth trajectories can shift quickly and being locked into unsuitable terms can create avoidable friction.

Security, Compliance, and Fraud Prevention

Security is a non-negotiable baseline for any payment platform, and Exact Payments meets the industry’s highest certification standard: PCI DSS Level 1 Service Provider status. This is the most stringent level of Payment Card Industry Data Security Standard compliance available, and achieving it requires rigorous independent audits, ongoing monitoring, and demonstrated adherence to comprehensive data security controls. For businesses evaluating payment partners, this certification provides meaningful assurance.

Beyond the certification, Exact employs tokenization and encryption as standard data protection mechanisms. Tokenization replaces sensitive cardholder data with non-sensitive tokens, meaning that even if a system is compromised, actual card details are not exposed. Encryption protects data in transit, reducing interception risk during the transmission of payment information.

The platform also supports 3D Secure 2.0, the authentication protocol used to verify cardholder identity during online transactions. This reduces fraud liability for merchants in online environments and improves the authentication experience compared to the original 3D Secure standard, which was often criticized for friction-heavy checkout flows.

Fraud management tools are available through the platform, though the depth of customization varies. Standard transaction monitoring and risk scoring are included, but merchants with highly specific fraud rule requirements, such as those operating in high-ticket or cross-border environments, should evaluate whether the built-in tooling meets their needs or whether additional fraud solutions are required.

Overall, Exact’s security posture is solid and industry-appropriate. It does not cut corners on foundational compliance, which is ultimately what matters most. Businesses in regulated industries or those handling sensitive customer data will find the platform’s security infrastructure adequate for standard operational requirements.

Reporting, Analytics, and Dashboard Features

For merchants and SaaS platform operators, access to clear and timely financial reporting is essential for day-to-day operations, reconciliation, and strategic decision-making. Exact Payments provides a reporting portal that covers the core data needs most businesses encounter regularly, though it is more operationally focused than analytically sophisticated.

Standard reporting features include transaction summaries, settlement reports, and chargeback tracking. These are the bread-and-butter outputs that finance teams and operations managers rely on for daily reconciliation and month-end close processes. The reporting portal is designed to be accessible to non-technical users, which reduces the operational dependency on developer involvement for routine financial oversight.

For SaaS platforms managing multiple sub-merchants, consolidated reporting becomes particularly important. The ability to view payment activity across an entire merchant portfolio, rather than logging into individual accounts, saves significant time and reduces the risk of overlooked discrepancies. Exact’s platform supports this consolidated view, which is a practical advantage for operators managing high sub-merchant counts.

Where the platform’s reporting capability is more limited is in the area of advanced analytics and business intelligence. Deep cohort analysis, revenue forecasting, or customizable analytics dashboards are not the primary focus of Exact’s reporting tools. Businesses that require sophisticated data analysis will likely need to export transaction data into separate BI tools or data warehouses. This is not an unusual limitation for a payments platform, most processors prioritize operational reporting over analytics depth, but it is worth factoring in for data-driven teams. For standard financial tracking and reconciliation, the reporting tools are functional and reliable.

Customer Support and Technical Assistance

Customer support is often where payment platforms reveal their true character. Marketing promises are easy to make; responsive, knowledgeable support during a live payment issue is far harder to deliver consistently. Exact Payments distinguishes itself here by emphasizing technical support staffed by experienced engineers rather than generalist customer service representatives.

The platform offers 24/7 technical support, which is an important commitment for businesses whose payment operations run around the clock. Payment failures at 2am on a weekend are not hypothetical events, they happen, and having access to technically capable support at that moment can make a meaningful difference to both the merchant and their end customers.

For SaaS platforms implementing Exact’s payment integration, post-sale technical support from engineers with deep product knowledge is particularly valuable. Integration projects inevitably encounter edge cases and unexpected behaviors, and the ability to get precise technical guidance, rather than generic troubleshooting scripts, accelerates resolution.

That said, support quality can vary depending on the scale and nature of the client relationship. Large enterprise clients or SaaS platforms with high transaction volumes are likely to receive more dedicated account management attention. Smaller operators may rely more heavily on general support channels, where response times and issue resolution quality can be less consistent. Prospective clients should ask specifically about support SLAs, escalation paths, and what dedicated account management looks like at their expected transaction volume. Onboarding support, the critical period when integration issues are most likely, is reportedly a strength, with Exact’s team described as highly responsive during implementation phases.

Strengths, Limitations, and Who It’s Best For

Exact Payments is a well-constructed platform for a specific and growing use case: helping SaaS companies embed payments into their products and activate a high-margin revenue stream without the complexity of becoming a full Payment Facilitator independently. In that lane, it performs genuinely well. The PayFac-as-a-Service model is coherent, the technical infrastructure is reliable, and the leadership team has the industry experience to navigate the compliance and processor relationships that underpin the whole operation.

The 99.99% uptime commitment, sub-one-second transaction response times, and PCI DSS Level 1 certification represent a serious operational foundation. These are not marketing embellishments, they reflect real infrastructure investment and are corroborated by the caliber of clients the platform serves.

The limitations are real but contextual. Pricing lacks public transparency, which adds friction to the evaluation process. Contract terms require careful review. The reporting and analytics tools serve operational needs well but are not designed for advanced business intelligence. International coverage is limited to the US and Canadian markets, which will not suit every business. And the platform’s depth of customization, while adequate for most SaaS use cases, falls short of what highly specialized or complex deployments might require.

The ideal customer for Exact Payments is a SaaS company operating in a vertical market, property management, healthcare administration, automotive services, entertainment, or similar, that wants to offer embedded payment acceptance to its customers, unlock payment revenue, and do so without building payment infrastructure in-house. For that profile, Exact Payments is a credible, proven option that deserves serious consideration alongside other embedded payments providers.

FAQs

Q1. Is Exact Payments only for SaaS companies, or can traditional merchants use it too?

Exact Payments is primarily designed and marketed for SaaS companies and software platforms looking to embed payment capabilities into their products through a PayFac-as-a-Service model. However, the underlying payment infrastructure also supports traditional merchants needing standard card and ACH processing.

That said, traditional merchants seeking a simple standalone payment processor may find that Exact’s feature set and pricing model are oriented more toward platform operators than individual business owners. It is worth having a direct conversation with Exact’s sales team to clarify whether their offering is the right fit for a non-SaaS use case before proceeding.

Q2. How long does it take to get onboarded and start accepting payments through Exact Payments?

For SaaS platforms using the PayFac-as-a-Service model, Exact’s automated onboarding process is one of its notable strengths. Sub-merchant applications submitted via the Onboarding API are reviewed through an automated underwriting system that delivers near real-time decisions.

In many cases, a newly onboarded sub-merchant can be live and processing payments within the same business day. For the SaaS platform itself, the initial integration timeline depends on technical complexity, but Exact’s REST API, sandbox environment, and 24/7 engineering support are designed to accelerate the implementation process. Straightforward integrations can often be completed within a few weeks.

Q3. Does Exact Payments support international transactions and multiple currencies?

Exact Payments’ current infrastructure and processor partnerships are concentrated in the United States and Canada, covering integrations with Elavon, Fiserv, Global Payments/TSYS, Chase Canada, and Moneris. This makes it a strong choice for North American businesses, but it is not currently positioned as a global payments platform.

Merchants or SaaS platforms with significant transaction volume outside North America, particularly in Europe, Asia-Pacific, or Latin America, should carefully assess whether Exact’s geographic coverage meets their needs. For businesses that anticipate international expansion as part of their growth strategy, it is worth discussing roadmap plans directly with Exact and evaluating whether supplementary payment providers may be required.

EVO Payments Review

By 10topmerchantservices April 5, 2026

Digital payments have become a fundamental part of how modern businesses operate. Whether it is a retail store accepting card payments at a counter or an online brand processing transactions across countries, payment systems now sit at the centre of business operations. What businesses need today is not just the ability to accept payments, but a reliable system that connects customers, banks, and platforms without friction. This is where payment processors come into the picture. Lets read more about EVO Payments Review.

Among the many players in this space, EVO Payments has built a presence as a global payment technology provider. It positions itself as a partner for businesses that want to accept payments across channels while maintaining security and compliance. However, the payment processing industry is highly competitive, and providers often appear similar on the surface. This makes it important to look beyond basic claims and understand how a platform performs in practical use.

What is EVO Payments? | EVO Payments Review

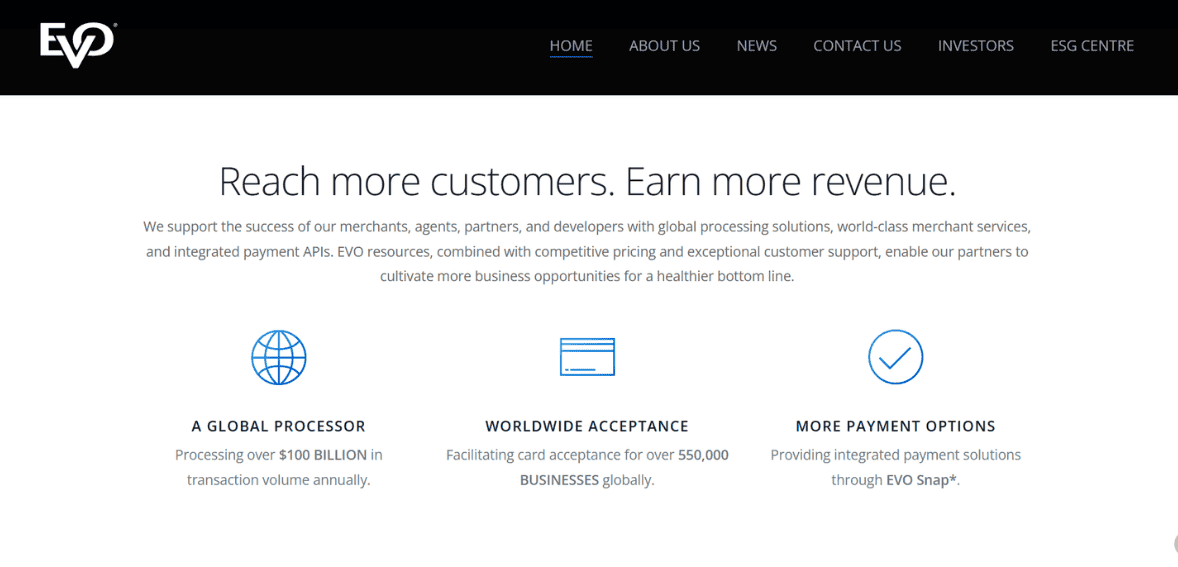

EVO Payments is a payment processing company that provides businesses with the ability to accept and manage electronic transactions. Its services cover a wide range of payment environments, including in-store, online, and mobile channels. At its core, the company connects merchants to financial institutions and card networks, enabling secure and efficient payment processing.

This platform is geared toward catering to companies of various types, ranging from small-time retailers to big organizations that operate across several regions. The platform provides functionality related to accepting payments, managing transactions, reports, and integrating with other applications. Therefore, it serves not only as a means of handling transactions but also in monitoring how businesses receive their income streams.

EVO Payments is a company that acts as an intermediary in the payment system environment. The platform manages communication between the merchant, acquiring banks, and card networks to complete each transaction successfully. This service is important since even the slightest inefficiency in the process of payments will negatively impact customers and businesses.

Even though EVO Payments is described as a solution with scalability and global reach, its true potential is dependent on the above-mentioned capabilities and many others. These aspects should be reviewed to determine the unique features of EVO Payments.

EVO Payments Company Background and Global Presence

EVO Payments has developed its presence over time by focusing on expanding into multiple geographic markets. The company operates across North America and Europe, serving businesses in both developed and emerging payment environments. This international footprint allows it to support merchants that operate across borders and need consistent payment solutions in different regions.

The growth of the company has been influenced by collaborations, mergers, and other expansions within the local market environments. It is worth noting that collaborations with banks and regional payment organizations enable EVO Payments to adjust its services to meet unique regulatory needs and operational considerations. This is crucial since payment processing is not a standard practice across various countries, and local compliance is critical in offering payment processing services.

EVO Payments’ global nature implies that the firm can process payments in different currencies and using multiple payment systems, thus benefiting companies with international clientele. However, its global operations imply that it may face some challenges when delivering its services in some countries due to the complexity associated with cross-border transactions. As such, while EVO Payments aims to serve global companies in terms of payment processing services, businesses should take into account the firm’s ability to deliver services in their local environment.

Key Features of EVO Payments

EVO Payments offers a range of features aimed at covering different aspects of payment processing. These include transaction processing, reporting tools, integration capabilities, and support for multiple payment channels. The platform is designed to handle both simple and complex payment requirements, depending on the size and needs of the business.

Among the most valuable benefits of the platform is the capability of supporting several payment environments within one system. Thus, enterprises can employ the platform not only for in-store payments using POS systems but also for online payments made through payment gateways and even mobile payments. Flexibility in this respect is essential for multi-channel retailers.

The second significant benefit is associated with the reporting and analytical capabilities of the platform. Merchants will be able to analyze their transaction data, measure their performance, and obtain insights relevant for managing finances. Although such features are rather helpful, the level of their development can significantly differ based on certain factors.

It should be also noted that the platform places emphasis on integration. In particular, retailers will be able to integrate with various tools and systems, including e-commerce platforms and accounting software solutions. Nevertheless, some challenges might occur in this regard, depending on the specifics of integration processes.

Payment Processing Capabilities

At its core, EVO Payments is built to handle payment transactions across different channels. It supports card payments, including credit and debit cards, and enables businesses to process transactions both in person and online. This makes it suitable for a wide range of industries, from retail to hospitality and eCommerce.

The ability of the platform to process cross-border payments also proves crucial in supporting companies working with foreign clients. Cross-border payments can be made using several currencies and allow expanding the company’s business to different markets without having to integrate a number of different payment systems. Still, cross-border processing entails certain extra costs.

The speed and effectiveness of transaction processing serve as crucial aspects in choosing the most appropriate payment system for use by the business. Processing delays and failures negatively affect the level of customer satisfaction, and that is why the effectiveness of transactions serves as an important characteristic. However, despite the wide range of functions offered by the platform, the effectiveness of its work might depend on different aspects, including network availability, integration process, and collaboration with local banks.

Supported Payment Methods and Integrations

EVO Payments supports a variety of payment methods to accommodate different customer preferences. These include traditional card payments as well as digital wallets and contactless payment options. As customer expectations continue to evolve, having access to multiple payment methods becomes increasingly important for businesses.

The platform also offers integration with various third-party systems, including eCommerce platforms and business management tools. This allows merchants to connect their payment processing with their existing workflows, reducing manual effort and improving efficiency.

Integration is one of the areas where payment processors can either add value or create friction. A well-integrated system can streamline operations, while a poorly implemented one can lead to delays and errors. EVO Payments provides the tools for integration, but the ease of implementation may vary depending on the technical capabilities of the business.

Businesses should also consider how flexible these integrations are. As operations grow or change, the ability to adapt the payment system becomes important. EVO Payments offers a level of flexibility, but it may require additional configuration or support in more complex setups.

POS Solutions

For businesses that operate in physical locations, POS solutions are an essential part of payment processing. EVO Payments provides POS options that enable merchants to accept card payments at counters or through mobile devices. These solutions are designed to integrate with the overall payment system, allowing transactions to be recorded and managed centrally.

The effectiveness of a POS system depends on its reliability, speed, and ease of use. Staff should be able to process transactions quickly without dealing with technical issues, as delays can affect customer experience. EVO Payments aims to provide stable POS functionality, but the actual performance may depend on the hardware and setup used.

Another important aspect is compatibility with existing business systems. Many businesses rely on inventory management or billing software, and the POS system needs to work seamlessly with these tools. EVO Payments offers integration options, but the level of compatibility can vary. While the POS solutions provided are functional, businesses should evaluate whether they meet their specific operational needs. Factors such as cost, hardware requirements, and support should be considered before making a decision.

eCommerce and Online Payment Solutions

Online payments are a critical component for businesses operating in the digital space. EVO Payments provides payment gateway solutions that allow businesses to accept payments through websites and mobile applications. These solutions are designed to handle different types of transactions, including one-time payments and recurring billing.

The checkout experience plays a significant role in customer satisfaction, and a smooth payment process can reduce cart abandonment rates. EVO Payments aims to provide secure and efficient online transactions, but the overall experience may depend on how well the system is integrated with the business’s website.

Recurring payments are another important feature for subscription-based businesses. EVO Payments supports this functionality, allowing businesses to automate billing processes. This can improve efficiency and reduce manual effort, but it also requires careful setup to avoid errors. While the platform provides the necessary tools for online payments, businesses should assess how user-friendly and reliable the system is in practice. Ease of integration and consistent performance are key factors in determining its effectiveness.

Security, Compliance and Fraud Protection

Security is one of the most critical aspects of payment processing. EVO Payments implements measures such as encryption and compliance with industry standards to protect transaction data. These measures are essential for maintaining trust and ensuring that sensitive information is handled securely.

Compliance with standards such as PCI requirements is a basic expectation in the payments industry. EVO Payments adheres to these standards, which helps reduce the risk of data breaches and fraud. However, compliance alone does not guarantee complete protection, and businesses still need to follow best practices in their own operations.

Fraud prevention tools are also part of the platform’s offering. These tools help identify suspicious transactions and reduce the risk of financial losses. The effectiveness of these tools depends on how they are configured and monitored. While EVO Payments provides a secure environment, businesses should remain proactive in managing their own security practices. Payment processors can reduce risk, but they cannot eliminate it entirely.

Pricing Structure and Fees

Pricing is one of the most important factors when choosing a payment processor. EVO Payments does not always present a fully transparent pricing structure upfront, and costs can vary depending on the business type, transaction volume, and region. This makes it important for businesses to review contracts carefully before committing.

Typical costs may include transaction fees, monthly service charges, and setup fees. Additional charges may apply for features such as cross-border transactions or advanced integrations. Without clear visibility into all costs, businesses may find it difficult to estimate their total expenses.

Another consideration is contract terms. Some payment processors require long-term agreements, which can limit flexibility. Businesses should understand the terms and conditions, including any penalties for early termination. While EVO Payments may offer competitive pricing in some cases, the lack of standardised transparency can be a concern. Businesses should compare it with other providers and ensure they have a clear understanding of all fees involved.

Ease of Use and Onboarding Experience

The onboarding process is an important first step for any payment system. EVO Payments provides support for setting up accounts and integrating its services, but the experience can vary depending on the complexity of the business’s requirements.

For smaller businesses with simpler needs, the setup process may be relatively straightforward. However, larger businesses or those requiring custom integrations may face a more involved onboarding process. This can include technical configuration and coordination with multiple systems.

Ease of use is another key factor. The platform should allow businesses to manage transactions, access reports, and handle operations without excessive effort. While EVO Payments provides the necessary tools, the user interface and overall experience may not always be as intuitive as some newer platforms. Businesses should consider how much time and effort they are willing to invest in setup and ongoing management. A system that is powerful but difficult to use may not deliver the expected benefits.

Customer Support and Service Quality

Customer support plays a crucial role in payment processing, as issues can directly impact business operations. EVO Payments offers support services to assist merchants with technical problems and account-related queries. The quality of support can vary, and response times may depend on the region and type of issue. Some businesses report satisfactory experiences, while others highlight delays or challenges in resolving issues. This inconsistency is something to consider when evaluating the platform.

Availability of support is also important. Businesses operating across different time zones may require assistance outside standard working hours. EVO Payments provides support channels, but the level of accessibility may not always meet expectations. Reliable customer support can make a significant difference in overall experience. Businesses should consider this aspect carefully, especially if they rely heavily on payment systems for daily operations.

Pros and Cons of EVO Payments

EVO Payments offers several advantages, including its global presence, support for multiple payment channels, and ability to handle different transaction types. These features make it a versatile option for businesses that need a comprehensive payment solution.

However, there are also limitations to consider. Pricing transparency is not always clear, and the onboarding process can be complex for some businesses. Customer support experiences can vary, which may affect reliability in critical situations. The platform’s value ultimately depends on how well it aligns with the specific needs of a business. While it provides a broad set of capabilities, it may not be the best fit for every use case.

Who Should Use EVO Payments?

EVO Payments is generally suited for businesses that require multi-channel payment processing and operate across different regions. It can be a good fit for medium to large businesses that need scalable solutions and are comfortable managing more complex systems.

Smaller businesses with simpler needs may find the platform more than they require, especially if they prioritise ease of use and transparent pricing. In such cases, alternative providers with simpler setups may be more suitable. Businesses that value global reach and integration capabilities may benefit from using EVO Payments, provided they are willing to invest time in setup and management.

Final Verdict: Is EVO Payments Worth It?

EVO Payments offers a comprehensive payment processing solution with a strong global presence and a wide range of features. It is capable of handling complex payment requirements and supporting businesses that operate across multiple channels and regions. However, it is not without its challenges. Pricing transparency, onboarding complexity, and varying customer support experiences are factors that businesses should consider carefully. These aspects can influence the overall value of the platform. In conclusion, EVO Payments can be a suitable choice for businesses that need a flexible and scalable payment solution, but it may not be the best option for those looking for simplicity and complete cost clarity. A careful evaluation based on specific business needs is essential before making a decision.

FAQs

Is EVO Payments suitable for small businesses?

EVO Payments can work for small businesses, but it may be more complex than necessary for those with simple payment needs.

What types of payments does EVO Payments support?

It supports card payments, online transactions, mobile payments, and cross-border transactions in multiple currencies.

How does EVO Payments handle security and fraud prevention?

The platform uses encryption, compliance standards, and fraud detection tools to protect transactions, though businesses must also follow their own security practices.

Ecommpay Review

By 10topmerchantservices March 30, 2026

Ecommpay is a global payment service provider that offers businesses a unified platform to manage online transactions, payment processing, and financial operations. As digital commerce continues to expand across regions and industries, payment infrastructure has become a critical component for businesses looking to operate efficiently and scale across markets. Ecommpay positions itself as a solution that simplifies complex payment ecosystems while maintaining flexibility for different business needs. Lets read more about Ecommpay Review.

The platform is designed to support businesses that require multi-currency transactions, diverse payment methods, and seamless customer experiences. It combines payment acceptance, fraud management, and reporting within a single system, which reduces dependency on multiple vendors. This integrated approach can help businesses streamline operations and maintain better visibility over their financial data.

Company Background and Market Position | Ecommpay Review

Ecommpay operates as an international payment solutions provider with a presence across multiple regions, including Europe, Asia, and other global markets. Over time, it has built its position in the fintech ecosystem by focusing on cross-border payment processing and customizable solutions for businesses with complex operational requirements. This approach reflects the increasing demand for payment systems that can handle global transactions efficiently.

The company’s market positioning leans toward mid-sized and enterprise-level businesses rather than very small merchants. Many of its offerings are designed to support higher transaction volumes and more advanced payment workflows, which makes it more suitable for companies that are already operating at scale or planning to expand internationally. This focus allows Ecommpay to provide more tailored solutions, but it can also make the platform feel less straightforward for businesses with simpler needs.

In a competitive market that includes established payment gateways and fintech platforms, Ecommpay differentiates itself through its modular infrastructure and flexibility. Businesses can configure the platform to suit their specific requirements, which is an advantage for those dealing with varied payment scenarios. At the same time, this level of customization requires a certain level of technical understanding, which may not be ideal for every user.

Core Payment Processing Capabilities

At its core, Ecommpay enables businesses to process digital transactions through a centralized and structured system. It manages the entire payment lifecycle, starting from customer checkout to authorization, processing, and final settlement. This end-to-end approach helps businesses maintain consistency in how transactions are handled, reducing the need for multiple disconnected systems.

One of the key strengths of the platform lies in its ability to handle large transaction volumes without compromising performance. For businesses operating in high-demand environments, consistent processing speed and reliability are critical. Ecommpay is built to support such requirements, which makes it suitable for industries where transaction continuity directly impacts revenue and customer satisfaction.

The platform also includes intelligent routing capabilities that aim to improve transaction success rates. By directing payments through the most effective channels based on location, currency, and other factors, businesses can reduce failed transactions and improve overall efficiency. This feature is particularly useful for companies that operate across different regions with varying banking infrastructures.

However, the effectiveness of these capabilities often depends on how well the system is configured. Businesses may need to invest time in optimizing payment flows to fully utilize the platform’s potential. When implemented properly, Ecommpay provides a strong foundation for managing digital payments at scale.

Supported Payment Methods and Global Reach

Ecommpay supports a wide range of payment methods, allowing businesses to cater to diverse customer preferences across different markets. These include major card networks, digital wallets, bank transfers, and a variety of alternative payment methods. This flexibility is essential for businesses that want to provide a smooth checkout experience to customers from different regions.

The platform’s global reach is one of its most significant advantages. It enables businesses to accept payments in multiple currencies and operate across borders without needing separate payment providers for each region. This capability simplifies expansion into new markets and reduces operational complexity for businesses with international customers.

In addition to widely used payment options, Ecommpay also integrates localized payment methods that are specific to certain countries or regions. Offering these options can improve customer trust and increase conversion rates, as users are more likely to complete transactions when familiar payment methods are available.