Bluefin Payment Systems Review

15

Jan 2026

No Comments

Bluefin Payment Systems Review

Bluefin Payment Systems operates at the intersection of payment processing and data security, a space that has become increasingly important as digital transactions grow more complex and regulatory pressure continues to rise. Rather than positioning itself as a traditional merchant acquirer competing on pricing or rapid onboarding, Bluefin has built its reputation around protecting sensitive payment data and reducing merchant exposure to security risks. This focus shapes nearly every aspect of its product design, partner relationships, and ideal customer profile. Lets read more about Bluefin Payment Systems Review.

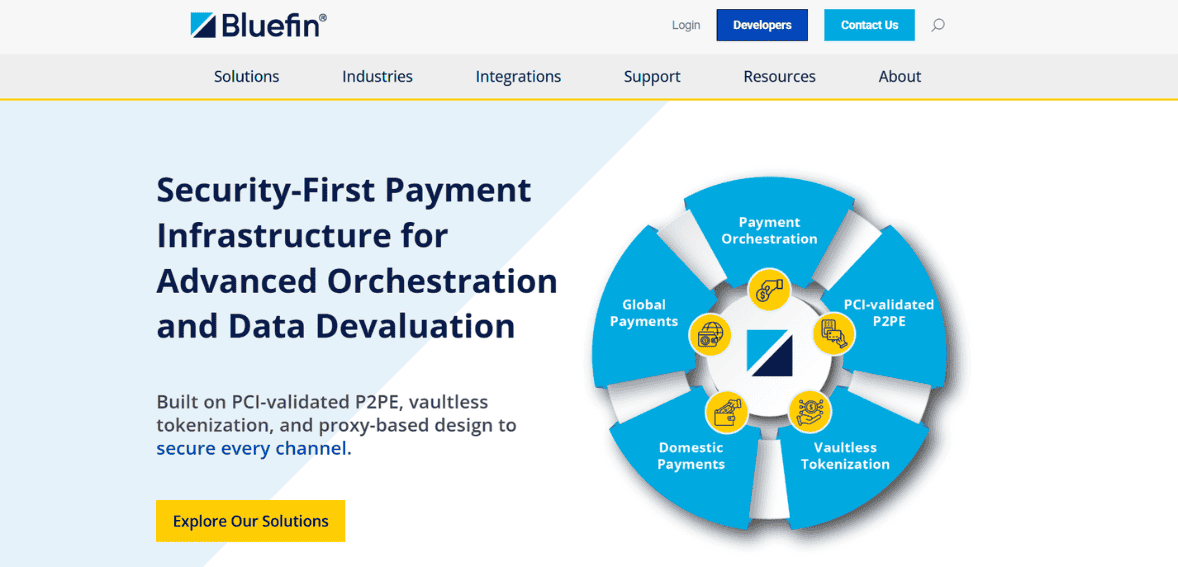

It is most well-recognized as a company that focuses heavily on encryption and tokenization solutions that seek to ensure cardholder data stays completely out of the merchant environment. This resonates well with companies that look to view payments as more than just a transactional service, because if not handled correctly, it could represent a risk to operations. Data breaches, protection of cardholder data, and cybersecurity are rising to more forefronts than they used to, which puts Bluefin Payments into their own niche.

However, the security-first design paradigm is not the only area where Bluefin involves trade-offs. This is especially the case when merchants are considering Bluefin and are forced to weigh the potential increase in the overall cost of implementation due to the specialized hardware. This commentary aims to examine Bluefin from a balanced perspective, considering both the advantages and disadvantages of Bluefin and avoiding the assumption that Bluefin is the right choice for every merchant and organization. In other words, this commentary aims to help the reader understand where Bluefin is useful and where other solutions are simpler.

Core Business Model and Market Focus | Bluefin Payment Systems Review

Bluefin’s business model is built less around volume-based transaction processing and more around enabling secure payment ecosystems for businesses with heightened compliance or data protection requirements. Rather than marketing itself aggressively to micro-merchants or startups, the company tends to align with organizations that already recognize payment security as a strategic priority rather than an afterthought. This includes regulated industries, enterprise merchants, and software platforms that embed payments into larger operational workflows.

One of the essential aspects of Bluefin is the way the company distributes its services. Bluefin tends to collaborate and work together with credit card merchants directly and other merchants, point-of-sale vendors, software companies, and even acquire banks. This way, Bluefin acts as the security component of the payments technology ecosystem, and not as the competitor to the credit card companies due to the brand name. This is advisable for those merchants who want to have the security component built right into their systems.

At the same time, it should be noted that Bluefin could potentially be less visible to smaller merchants looking to acquire a ready-made solution. This is because Bluefin’s product suite is more suited to an entity that either has access to their own in-house IT personnel, as well as technical support teams that could address any integrations necessary. What it comes down to is that Bluefin is more suited to businesses operating at scale because it is a company that places more weight on comprehensive protection as opposed to ease of use.

Payment Processing Capabilities

From a functional standpoint, Bluefin supports standard electronic payment processing requirements without attempting to differentiate itself on novelty features. Core capabilities typically include acceptance of major card brands, support for EMV transactions, and compatibility with both card-present and card-not-present environments. These features align with what most merchants expect from a modern payment processor, ensuring that security enhancements do not come at the expense of basic usability.

Where Bluefin’s processing power differs is in its approach to the underlying structure of transactions. Instead of allowing unsecured card information to be transmitted through the payment system at the business level, the organization is set up so that payments can be encrypted at the earliest point in the payment process. This has a significant impact on everything that has been discussed so far, right through from technology choice through to system integration and reporting requirements.

It should be noted that Bluefin does not market itself as a one-stop ecommerce-enabling solution. The provision of additional functionalities such as customer loyalty programs, marketing analysis tools, or business management dashboards is not what Bluefin does, per se. These requirements may be met by merchants through other ecommerce platforms or software tools that co-exist with Bluefin’s payment infrastructure. Thus, it should be understood that Bluefin’s processing functionality needs to be assessed within an overall environment or context.

Encryption and Tokenization Technologies

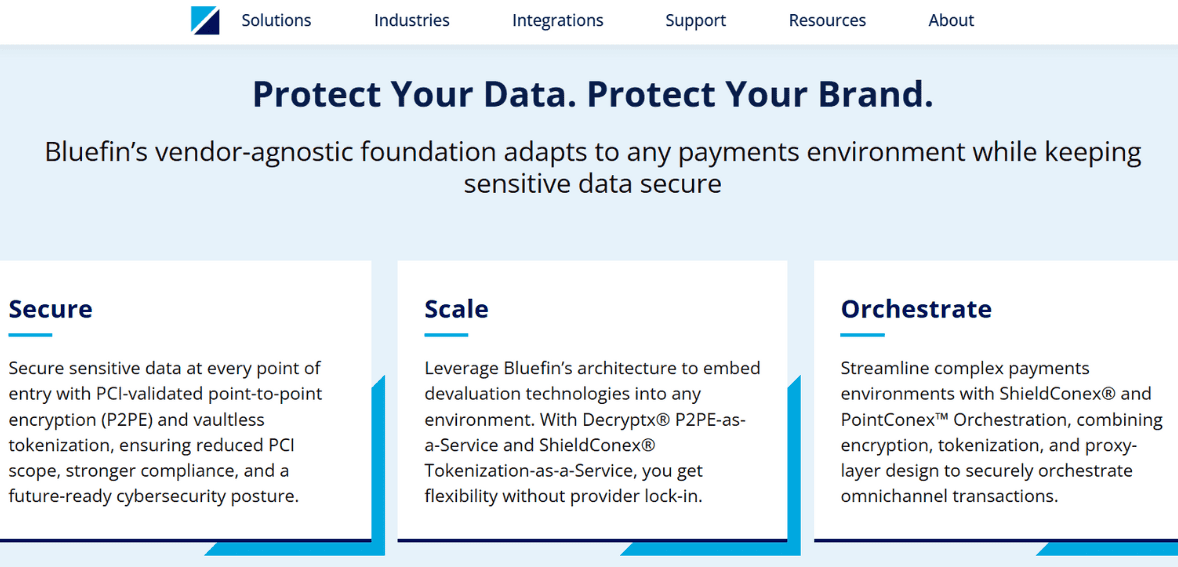

Encryption and tokenization form the foundation of Bluefin’s value proposition. The company places strong emphasis on point-to-point encryption, which ensures that payment data is encrypted at the moment of card interaction and remains unreadable throughout transmission. This approach significantly reduces the number of systems that ever come into contact with sensitive cardholder information, lowering the overall risk surface for merchants.

Tokenization complements this model by replacing actual card data with non-sensitive tokens that can be stored or reused for operational purposes. These tokens allow businesses to perform functions like recurring billing, refunds, or transaction lookups without retaining real payment data. From a security perspective, this reduces the potential impact of a system breach, as stolen tokens have no standalone value outside the authorized environment.

While these technologies are increasingly common in enterprise payment systems, their implementation quality varies widely across providers. Bluefin’s differentiation lies in consistency and scope, particularly in environments where payments occur across multiple channels or devices. However, merchants should also recognize that advanced encryption and tokenization can introduce dependencies on specific hardware, vendors, or workflows. For organizations unprepared to manage these dependencies, the security benefits may come with increased operational complexity.

PCI Compliance and Regulatory Alignment

One of the primary reasons merchants consider Bluefin is its potential to reduce PCI DSS scope. By keeping cardholder data encrypted and tokenized outside merchant systems, Bluefin can significantly simplify compliance requirements, particularly for businesses that would otherwise fall under more demanding PCI categories. This reduction in scope often translates to fewer audit obligations and lower long-term compliance risk.

That said, it is important to clarify that no payment provider fully removes a merchant’s compliance responsibilities. Bluefin’s architecture can streamline PCI assessments, but merchants are still accountable for maintaining secure environments, managing access controls, and following applicable policies. The difference lies in how much of the sensitive data handling is shifted away from internal systems.

Regulatory alignment also extends beyond PCI DSS. Businesses operating in healthcare, education, or government-adjacent sectors often face overlapping compliance frameworks where data protection expectations are high. Bluefin’s security-first positioning makes it attractive in these contexts, though organizations should still conduct due diligence to ensure alignment with specific regulatory requirements relevant to their industry.

Omni-Channel Payment Support

Modern businesses rarely operate within a single payment channel, and Bluefin acknowledges this reality through its support for omni-channel transactions. The company’s security model is designed to function consistently across in-store, online, mobile, and unattended payment environments. This consistency is critical for organizations that want to maintain uniform compliance and risk controls regardless of how or where a payment occurs.

Rather than treating each channel as a separate system, Bluefin emphasizes centralized tokenization and encryption policies. In theory, this allows merchants to manage customer payment data in a unified way while still maintaining strong protections. For multi-location or digitally integrated businesses, this reduces fragmentation and simplifies internal oversight.

However, omni-channel support often depends heavily on integrations with third-party platforms. The quality of the experience can vary depending on the POS system, ecommerce platform, or gateway in use. Merchants evaluating Bluefin should pay close attention to how well its security framework aligns with their existing technology stack, particularly if they rely on niche or highly customized systems.

Hardware and Terminal Compatibility

Bluefin’s focus on encryption places particular importance on hardware selection. Compatible terminals must support secure data capture and encryption at the point of interaction, which can limit device options compared to more open payment processors. While this restriction enhances security, it may also require merchants to replace existing hardware or work within a narrower range of approved devices.

For businesses already planning hardware upgrades, this limitation may be negligible. For others, especially those with large installed terminal bases, compatibility considerations can influence overall project cost and timelines. Bluefin typically works within established hardware ecosystems rather than offering proprietary devices, which provides some flexibility while maintaining security standards. From an operational perspective, hardware decisions are closely tied to deployment planning. Merchants should evaluate not just upfront device costs, but also long-term support, maintenance, and update requirements associated with encrypted terminals.

Software Integrations and API Ecosystem

Bluefin’s integration strategy reflects its role as a security layer rather than a complete business platform. The company offers APIs and integration tools that allow developers and software partners to embed secure payment functionality into broader applications. This approach is well suited for ISVs and enterprises building customized payment workflows.

The effectiveness of these integrations depends heavily on implementation quality and documentation. While Bluefin supports a wide range of integrations, development resources and technical expertise are often required to achieve optimal results. For organizations without in-house development capabilities, reliance on third-party integrators or partners becomes a key consideration.

Pricing Structure and Cost Transparency

Pricing is an area where security-focused providers can appear less transparent, and Bluefin is no exception. Costs are typically influenced by transaction volume, hardware requirements, integration complexity, and ongoing security services. Rather than offering simple flat-rate pricing, Bluefin’s pricing model is more commonly structured through customized agreements. This approach aligns with enterprise purchasing norms but may be less appealing to small businesses seeking predictable monthly costs. Merchants should factor in not only processing fees but also implementation, hardware, and support expenses when evaluating overall value.

Implementation and Onboarding Experience

Implementing Bluefin is rarely a purely plug-and-play process. Onboarding often involves coordination between multiple stakeholders, including acquiring banks, software vendors, and internal IT teams. While this complexity supports stronger security outcomes, it also extends deployment timelines compared to simpler processors. For organizations accustomed to structured IT rollouts, this process may feel familiar. For others, the learning curve can be steep. Clear planning and dedicated resources are critical to avoiding delays and misalignment during implementation.

Scalability for Growing Businesses

Bluefin is generally well suited for businesses anticipating growth in transaction volume, geographic reach, or regulatory scrutiny. Its security architecture scales effectively across locations and channels, making it a strong option for organizations planning long-term expansion. That said, scalability also depends on internal readiness. Businesses without mature operational processes may struggle to fully leverage Bluefin’s capabilities without external support.

Customer Support and Account Management

Support experiences with Bluefin tend to reflect its enterprise orientation. Merchants often interact with account managers or technical support teams rather than self-service portals. This model can be beneficial for complex environments but may feel slower for simple requests. Response quality and availability can vary depending on contract structure and partner involvement, making it important for merchants to clarify support expectations during onboarding.

Strengths and Limitations

Bluefin’s greatest strength lies in its comprehensive approach to payment security. However, this comes at the cost of simplicity, speed, and sometimes transparency. It is not designed to be the fastest or cheapest option, but rather a controlled and compliant one.

Who Should Consider Bluefin Payment Systems

Bluefin is best suited for organizations that view payment security as a core operational requirement rather than a checkbox. Regulated industries, enterprise merchants, and software platforms stand to benefit most, while very small or low-risk businesses may find simpler alternatives more practical.

FAQs

Is Bluefin Payment Systems suitable for small businesses?

It can be, but its security-focused model often aligns better with medium to large organizations that face higher compliance or risk exposure.

Does Bluefin eliminate PCI compliance responsibilities?

No. It reduces scope and complexity, but merchants remain responsible for meeting applicable PCI requirements.

How does Bluefin differ from standard payment processors?

Its primary differentiation is a security-first architecture focused on encryption and tokenization rather than feature breadth or pricing simplicity.

Best Product & Services

Recent Posts