BancCard Review

24

Dec 2025

No Comments

BancCard Review

BancCard is a U.S. based merchant services provider that enables businesses to accept credit and debit card payments across multiple sales channels. Its primary function is payment processing rather than full-scale business management software. The company focuses on providing merchant accounts, payment terminals, and backend processing support for businesses that rely on electronic transactions. Lets read more about BancCard Review.

BancCard mainly collaborates with small and medium sized enterprises, but it can also accommodate large merchants based on the type of the industry and the volume of processing. Typical scenarios are retail stores, restaurants, professional service providers, and businesses that accept payments both in, person and remotely. BancCard might also be a source of funds for certain higher risk industries; however, approval terms are generally set by underwriting.

The company is functioning on a traditional merchant account model as opposed to a self, service, flat, rate kind of model. In other words, the pricing, the contract terms, and the feature access can be different from one merchant to another. Although this arrangement offers the possibility of customization, it also puts more merchants in the position of having to fully understand the agreement before signing as they take on the greatest part of the responsibility.

BancCard is a perfect match for businesses which require the support of a dedicated team for payment processing and are willing to go through a more traditional onboarding process. Merchants who are in search of highly standardized pricing or instant online sign up might feel that the process is not as efficient. In general, BancCard is the right choice for businesses that prioritize account, level support and do not mind having upfront discussions about the terms and costs.

BancCard’s Payment Processing Capabilities | BancCard Review

BancCard supports a range of payment processing options designed to cover both card-present and card-not-present transactions. Businesses can accept major credit and debit cards, including Visa, Mastercard, American Express, and Discover. Processing is available for in-store purchases, phone orders, and online transactions, depending on the merchant’s setup.

For brick-and-mortar businesses, BancCard enables traditional swipe, chip, and contactless payments through compatible terminals. Contactless support allows customers to pay using mobile wallets such as Apple Pay and Google Pay, which has become increasingly important for customer convenience and checkout speed.

Card-not-present transactions are supported through virtual terminals and e-commerce integrations. This makes BancCard viable for service-based businesses that take payments over the phone or send invoices, as well as businesses that operate partially or fully online. However, the exact features available may depend on the merchant’s risk profile and processing needs.

One consideration is that BancCard’s processing environment is not positioned as a plug-and-play solution. Merchants may need assistance during setup, particularly when integrating online payment tools or configuring fraud controls. This can be beneficial for businesses that want guidance but less appealing for those seeking instant deployment.

Overall, BancCard’s payment processing capabilities are broad and functional, covering most standard business requirements without attempting to compete with advanced fintech platforms focused on automation or developer-first tools.

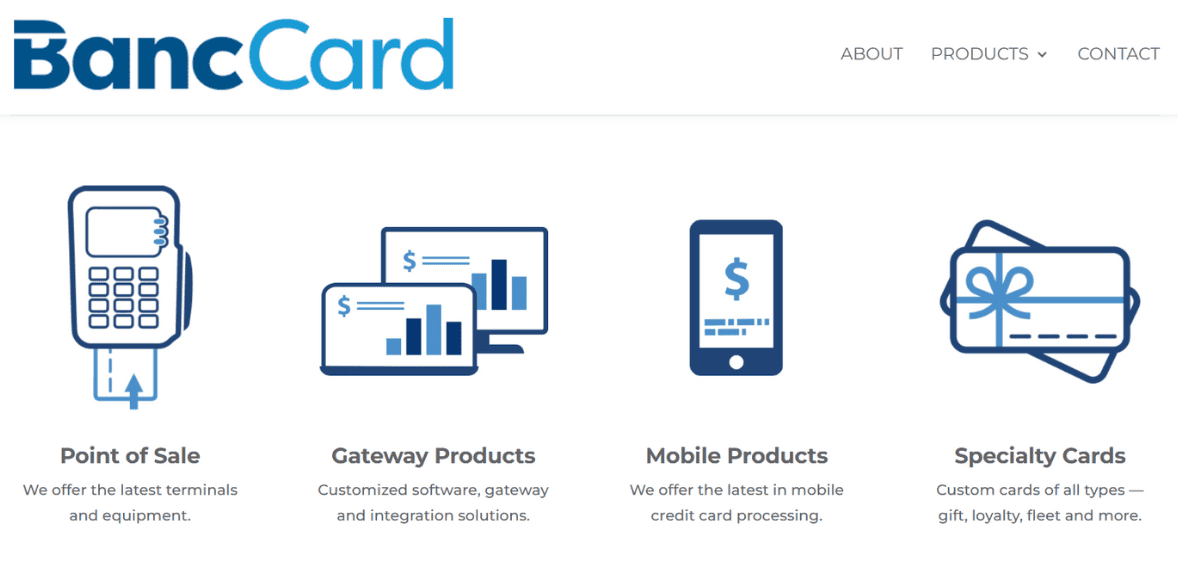

POS Systems and Hardware Options

BancCard presents a selection of point of sale hardware alternatives that can facilitate in-store transactions. Typically, these are countertop terminals, mobile card readers, and wireless devices intended for businesses that require checkout flexibility. The availability of hardware may depend on merchant needs, location, and processing volume.

The terminals made available are to a large extent capable of supporting EMV chip cards, contactless payments, and magnetic stripe transactions. Thus, the company ensures compliance with the latest payment security standards and at the same time, customers are given the opportunity to use the most recent payment methods. There are also some devices that may allow the user to print the receipt, leave a tip, and view simple transaction reports directly from the terminal.

BancCard does not consider itself as a provider of proprietary POS software. Rather, it concentrates on payment acceptance hardware rather than on a fully integrated POS ecosystem that comes with inventory, employee management, or CRM tools. In the case of businesses which are already using a separate POS system, compatibility may be available, however, integration details should be confirmed beforehand.

There is not always a standard of hardware costs and leasing options, which is why merchants should find out whether the equipment is purchased outright, rented, or bundled into a long term agreement. Leasing agreements, in particular, can become costly over time if one is not fully aware of the terms. In summary, BancCard’s hardware offerings are practical and functional, but businesses seeking advanced POS features or deep software integrations may need to supplement BancCard’s tools with third-party solutions.

E-commerce and Virtual Terminal Solutions

BancCard supports e-commerce payments and remote transaction processing through virtual terminals and online payment gateways. These tools allow businesses to accept payments without a physical card reader, making them suitable for service providers, phone-based sales, and online merchants.

A virtual terminal allows a merchant to enter card information manually via a secure online interface. This method is typically used for invoicing, mail orders, or customers paying over the phone. Although a virtual terminal is a viable option, it is often accompanied by higher processing fees because of the increased risk of fraud. Therefore, merchants should take this into account when deciding on their pricing strategy.

For online sales, BancCard is able to integrate with some e-commerce platforms or offer hosted payment pages. The degree of customization and support for integration may change, and businesses with complex online requirements should check compatibility first before making a decision. BancCards e-commerce tools are mostly meant for typical scenarios rather than heavily customized checkout flows.

Security features like encryption and tokenization are usually implemented to secure cardholder data during online transactions. However, merchants must also ensure PCI compliance and take care of customer data according to the rules. In short, BancCards solutions for e-commerce and virtual terminals are enough to facilitate online payments. They may not have the same level of flexibility as developer centric platforms, but they are dependable options for businesses that want a simple way to remotely accept payments.

ricing Structure and Fee Transparency

BancCard does not advertise a single, universal pricing model. Instead, pricing is typically customized based on the merchant’s industry, transaction volume, and risk profile. Merchants may be offered interchange-plus pricing, tiered pricing, or other negotiated rate structures depending on their account setup.

This flexibility can be beneficial for established businesses with predictable volumes, as it may allow for more competitive rates compared to flat-fee processors. However, it also means pricing transparency is not immediate. Merchants must carefully review their rate sheets and fee disclosures to understand the true cost of processing. Common fees may include monthly account fees, PCI compliance fees, statement fees, and transaction-related charges. Some fees may not be obvious during initial discussions, making it important to ask for a full breakdown in writing.

Because pricing is negotiated, different merchants may have very different experiences with BancCard’s cost structure. This makes it difficult to generalize whether BancCard is inexpensive or costly without reviewing a specific agreement. Overall, BancCard’s pricing approach rewards due diligence. Businesses willing to review contracts carefully and ask detailed questions may find reasonable value, while those expecting simple, published pricing may find the process less straightforward.

Contract Lengths, Early Termination, and Hidden Costs

BancCard typically operates under standard merchant services contracts, which often include multi-year terms. Contract lengths may range from one to several years, with auto-renewal clauses that extend the agreement unless canceled within a specific notice period.

Early termination fees are a common concern with traditional processors, and BancCard contracts may include such fees depending on the agreement. These fees can be flat-rate or variable, sometimes tied to remaining months on the contract. Merchants should confirm the exact terms before signing. Other potential costs may include equipment leasing obligations, annual compliance fees, or minimum processing requirements. These charges may not impact every merchant, but they can significantly affect overall cost if overlooked.

Auto-renewal clauses are particularly important to understand, as missing a cancellation window can lock a business into an additional term. Merchants should note deadlines and cancellation procedures clearly. In summary, BancCard’s contract structure reflects traditional merchant service practices. Businesses that value flexibility or short-term commitments should review terms carefully, while those comfortable with longer agreements may find the structure manageable if pricing is competitive.

Security, PCI Compliance, and Fraud Prevention

BancCard provides standard security features designed to protect cardholder data and reduce fraud risk. These typically include encryption of transaction data and support for EMV and contactless payment standards, which help reduce counterfeit card fraud. PCI compliance support is generally offered, though merchants remain responsible for completing required questionnaires and maintaining compliance. BancCard may provide guidance or tools to assist with this process, but failure to comply can result in additional fees.

For online and card-not-present transactions, fraud prevention tools such as address verification and CVV checks may be available. The effectiveness of these tools depends on configuration and merchant usage rather than automation alone. BancCard’s security approach is practical rather than cutting-edge. It focuses on meeting industry standards rather than offering advanced AI-driven fraud detection. This is sufficient for many businesses but may not meet the needs of high-volume e-commerce merchants facing sophisticated fraud risks. Overall, BancCard offers a solid baseline of security and compliance features, but merchants with higher risk exposure may need additional third-party fraud tools.

Funding Speed and Settlement Timelines

BancCard offers standard settlement timelines consistent with traditional processors. Most merchants can expect funds to be deposited within one to two business days, depending on transaction type and bank relationships. Same-day or next-day funding options may be available for qualifying merchants, though these services can come with additional fees or requirements. Funding speed often depends on account history, processing volume, and risk assessment.

Delays can occur in cases of chargebacks, unusual transaction activity, or compliance reviews. Merchants should be aware that reserve requirements may apply in certain situations, temporarily holding a portion of funds. Compared to fintech processors that emphasize instant payouts, BancCard’s funding model is more conservative. This can enhance stability but may not suit businesses that rely on immediate cash flow. In general, funding reliability is more consistent than exceptionally fast. Businesses with predictable cash flow needs may find BancCard’s settlement timelines acceptable.

Customer Support and Account Management

BancCard provides customer support through traditional channels such as phone and email. Some merchants may also receive a dedicated account manager, particularly for higher-volume accounts. The onboarding experience can involve direct communication with support staff, which may help businesses navigate setup and compliance requirements. This hands-on approach can be valuable for merchants unfamiliar with payment processing. However, support quality may vary depending on account size and assigned representatives. Smaller merchants may experience longer response times compared to larger accounts.

BancCard does not emphasize self-service tools or extensive online knowledge bases. Businesses that prefer human assistance may appreciate this, while those seeking instant self-help options may find it limiting. Overall, customer support is functional and relationship-driven, aligning with BancCard’s traditional service model.

Reporting, Analytics, and Merchant Dashboards

BancCard provides merchants with access to transaction reports and account statements through an online portal. These tools allow businesses to track sales activity, settlements, and fees. Reporting capabilities are generally focused on financial reconciliation rather than business analytics. Merchants can review daily batches, monthly statements, and transaction histories, but advanced insights are limited. The dashboard is designed for clarity rather than customization. Businesses seeking detailed performance metrics or visual analytics may need external tools. For many small and mid-sized businesses, the reporting is sufficient for accounting and bookkeeping purposes. Larger businesses may require more robust analytics integrations. Overall, BancCard’s reporting tools are practical but basic, prioritizing accuracy over advanced data insights.

BancCard for High-Risk and Regulated Industries

BancCard may support certain high-risk or regulated industries, though approval is subject to underwriting review. Terms for these merchants often differ from standard accounts. Higher processing fees, rolling reserves, or stricter compliance requirements may apply. Businesses in regulated sectors should expect additional documentation requests. BancCard’s willingness to review higher-risk applications can be beneficial for merchants with limited options, but conditions may be more restrictive. Transparency during underwriting is important, as terms may change based on risk assessment. Overall, BancCard can be an option for some higher-risk businesses, but expectations should be set realistically.

Pros of Using BancCard

BancCard offers customized merchant accounts, broad payment acceptance, and traditional account-level support. It supports both in-store and remote transactions and provides reliable settlement timelines. The availability of human support and negotiable pricing can be advantageous for established businesses.

Cons and Potential Limitations

Lack of published pricing, long-term contracts, and potential termination fees are key drawbacks. Reporting tools are basic, and setup may require more effort. Merchants seeking simplicity or instant onboarding may find limitations.

Is BancCard the Right Payment Processor for Your Business

BancCard is best suited for businesses comfortable with traditional merchant services and negotiated agreements. It may appeal to merchants who value stability and support over automation. Businesses seeking flexibility, short contracts, or transparent flat pricing may want to compare alternatives.

FAQs

Does BancCard require a long-term contract

Many BancCard agreements include multi-year terms, though specifics vary. Merchants should review contract length and cancellation terms carefully.

Can BancCard support both in-store and online payments

Yes, BancCard supports card-present, virtual terminal, and e-commerce transactions depending on account setup.

Is BancCard suitable for small businesses and startups

It can be, but startups should carefully review fees and contract commitments to ensure alignment with early-stage needs.

Best Product & Services

Recent Posts