American Express Payment Solutions Review

14

Dec 2025

No Comments

American Express Payment Solutions Review

American Express Payment Solutions refer to the company’s suite of services that allow businesses to accept American Express cards across physical, online, and mobile payment environments. Unlike many payment processors that act primarily as intermediaries, American Express operates a closed-loop network where it maintains relationships with both cardholders and merchants. This structure influences how payments are authorized, settled, and supported. Lets read more about American Express Payment Solutions Review.

For merchants, American Express payment solutions are not designed to replace an existing processor in most cases but rather to complement it by enabling acceptance of Amex cardholders. These cardholders often represent a different customer segment focused on premium services, business travel, or higher discretionary spending. The platform is typically positioned as a value-driven acceptance option rather than a low-cost payment solution. Fees tend to reflect this positioning, balancing higher transaction costs against potential benefits such as larger average ticket sizes, reputable brand association, and access to cardmember-focused programs.

Core Payment Processing Capabilities | American Express Payment Solutions Review

When businesses process American Express payments, they can accept Amex credit and charge cards for sales, whether customers are shopping in a physical store or online. These transactions actually flow quite differently from typical open-loop networks. The reason is simple: American Express uniquely acts as both the card issuer and the network operator. This setup often simplifies specific parts of the authorization and settlement process, and it helps standardize policies across all merchants.

In physical locations, American Express transactions integrate into existing point-of-sale systems through compatible terminals, provided the merchant is enrolled for acceptance. For online transactions, Amex integrates into payment gateways and digital checkout systems, allowing customers to use their cards similarly to other major brands. Authorization responses are typically fast and consistent, benefiting from the closed-loop model. Merchants also gain access to standardized dispute and chargeback processes, which may differ in structure but are generally well-documented.

However, American Express does not attempt to compete as a full-service processor for all payment types. It does not replace debit processing, alternative payment methods, or local bank transfers. Instead, its core capability remains focused on enabling Amex card usage reliably and securely. For businesses deciding whether to add American Express, the key consideration is not technical functionality, which is generally solid, but whether their customer base includes enough Amex cardholders to justify acceptance.

Types of Businesses Best Suited for American Express

American Express payment solutions tend to align best with businesses that serve customers who value rewards, travel benefits, or premium experiences. This commonly includes businesses in hospitality, dining, travel services, professional consulting, healthcare, and luxury retail. Enterprise-level merchants and B2B service providers also frequently benefit from Amex acceptance due to corporate card usage. Small businesses can also find value, particularly if they operate in urban areas, serve international travelers, or cater to higher-income demographics. In these cases, refusing Amex may unintentionally create friction at checkout or signal limited payment flexibility.

But for businesses with tight margins, very price-sensitive clients, or many small transactions, those associated fees can be hard to swallow. Think about convenience stores, discount retailers, or places that primarily deal in cash; they generally don’t see much benefit from taking Amex. On the flip side, online businesses selling professional services, subscriptions, or high-value items often find a real advantage. The American Express brand, after all, often brings a certain level of trust, especially with international and corporate buyers. Honestly, American Express payment solutions are best seen as a calculated move, not a universal requirement. Businesses that truly understand their customer base, average transaction values, and brand identity are the ones most likely to profit from accepting it.

Merchant Account Structure and Setup Process

Accepting American Express typically requires merchants to establish a direct relationship with the company, separate from their primary payment processor in many cases. This onboarding process involves submitting business documentation, banking details, and compliance information for review. Approval timelines vary depending on business size, risk profile, and geographic location. Established businesses with clear operational histories often move through approval relatively smoothly, while newer or higher-risk businesses may face additional review steps.

Once approved, merchants receive access credentials and guidelines on enabling acceptance across their sales channels. Integration often requires coordination with existing payment processors or gateways to ensure American Express is properly configured at the terminal or checkout level. One benefit of the American Express model is clarity in terms of account ownership. Merchants generally deal directly with Amex for settlement and disputes related to Amex transactions, which can reduce ambiguity in responsibility. However, the separate account structure can also add administrative complexity. Businesses must reconcile American Express settlements independently from other card brands and manage reporting across systems. For companies with limited accounting resources, this is an important consideration during setup.

Transaction Fees and Pricing Model

American Express pricing has traditionally been higher than that of many other card networks, and this remains a central consideration for merchants. Fees are generally structured as a percentage of each transaction, though negotiated rates may apply for larger or enterprise-level businesses. The pricing reflects factors such as cardmember rewards funding, fraud protection infrastructure, and the demographics of Amex cardholders. From a cost perspective, American Express is rarely the lowest-priced option and should not be evaluated purely on transaction fees alone.

If your business enjoys high margins or customers who consistently spend more, those steeper processing costs might not be a big deal. They often get balanced out by bigger sales or simply happier customers. However, for other businesses, especially those selling low-margin items, the expense could easily swallow any upside. Generally, pricing is pretty clear, and most merchants know the fees beforehand. Still, things can change based on the card type, where the transaction happens, and whatever deals were struck. To truly figure out the cost, businesses really ought to look at the overall effect on their revenue, not just the processing fee itself. That key difference usually decides if taking American Express is actually worth it financially.

American Express Cards and Customer Spending Power

One of the primary reasons businesses choose to accept American Express is the spending behavior of its cardholders. Historically, Amex users tend to spend more per transaction and show higher loyalty to merchants that accept their preferred card. Many cardholders use American Express for business expenses, travel, dining, and professional services. This often translates into fewer price-sensitive purchasing decisions and a greater focus on service quality.

For merchants, this can lead to increased average order values and repeat business. In some sectors, Amex acceptance may even influence where customers choose to shop, especially for planned purchases. That said, higher spending power does not guarantee higher profits. Businesses must still account for processing costs and determine whether increased revenue translates into sustainable margins. American Express acceptance works best when aligned with a customer experience strategy rather than as a standalone payment decision. Merchants that understand their audience are more likely to benefit from the cardholder profile Amex attracts.

Point of Sale and Hardware Compatibility

American Express does not require proprietary hardware, which makes it relatively easy for merchants to enable acceptance across existing POS systems. Most modern terminals that support EMV and contactless payments can process Amex cards once properly configured. Merchants must ensure their terminals and software providers are certified to handle American Express transactions. This often involves activating Amex acceptance within the POS system rather than purchasing new equipment.

Mobile payment environments, including tablets and handheld terminals, also support Amex acceptance in most cases, making it suitable for on-the-go businesses or service professionals. From a flexibility standpoint, this hardware-agnostic approach is a strength. Merchants retain freedom of choice when upgrading or switching POS providers. However, setup discrepancies can arise depending on the processor or POS software in use. Businesses should confirm compatibility early to avoid delays or incomplete payment acceptance at launch.

Online Payments and E-Commerce Support

American Express integrates smoothly into most major e-commerce platforms through supported payment gateways. Customers can use their cards at checkout just as they would other credit cards, benefiting from secure authorization and familiar user flows. For subscription billing and recurring payments, Amex generally performs reliably, appealing to SaaS businesses and service providers that bill monthly or annually. Businesses can also support tokenization and secure card storage through compliant gateways.

When you’re a merchant, getting Amex set up really depends on your current technology. Good news: plenty of popular platforms already include Amex support right away. If you’ve got a custom setup, though, you might need a bit more development work. American Express also lets customers pay with mobile wallets and contactless online options, which is great because everyone expects that these days. The features are solid, but here’s a tip: always check your conversion data. You want to make sure Amex actually appeals to your customers, instead of just assuming everyone wants to use it.

Security Standards and Fraud Protection Measures

Security is a core component of American Express payment solutions. Transactions comply with PCI DSS requirements and benefit from encryption, tokenization, and real-time monitoring capabilities. The closed-loop network structure allows American Express to analyze transaction patterns across its entire ecosystem, which can enhance fraud detection accuracy. Merchants also receive support in managing disputes and chargebacks involving Amex cardholders.

Fraud liability depends on transaction type and compliance with security standards, such as EMV or secure e-commerce protocols. Merchants that follow best practices generally experience predictable dispute outcomes. While no system eliminates fraud risk entirely, American Express maintains a reputation for proactive monitoring and cardholder protection. This emphasis can indirectly benefit merchants by reducing fraudulent transaction exposure. For businesses operating in higher-risk environments, security strength may be a meaningful deciding factor in accepting American Express.

Reporting, Insights, and Business Analytics

American Express provides merchants with reporting tools that focus on transaction visibility, settlement tracking, and chargeback management. Reports are typically accessible through merchant portals or integrated dashboards. Transaction-level data allows businesses to monitor Amex-specific performance independently from other card brands. This can be especially useful for analyzing customer behavior, average spend, and repeat usage patterns.

While reporting is clear and reliable, it is not designed as a full analytics or business intelligence platform. Most merchants will still rely on their primary POS or accounting software for holistic financial insights. The value of Amex reporting lies in clarity rather than depth. Businesses gain transparency into payouts, fees, and disputes without unnecessary complexity. For larger merchants, data can be integrated into internal systems to support forecasting and reconciliation processes.

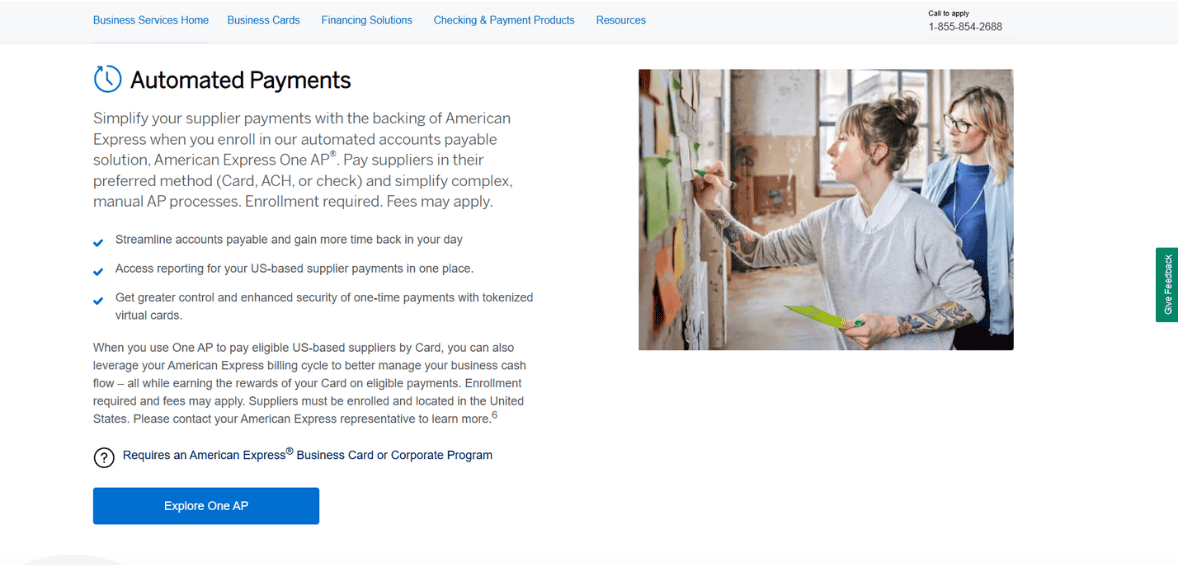

Funding Timelines and Settlement Process

American Express settlement timelines differ slightly from traditional processors due to the direct relationship model. Funds are typically deposited according to defined schedules, which merchants can review during onboarding. While settlement speed is generally reliable, it may not always be as fast as next-day funding offered by some processors. Businesses with tight cash flow cycles should factor this into their decision-making.

Consistency is a huge plus here. Once things are set up, business owners know exactly when their money will hit the bank, making planning a breeze. Of course, keeping Amex separate from other card brands can make things clearer. But, fair warning, it does mean an extra step when you’re balancing the books. Honestly, when your funds arrive usually isn’t the biggest headache. Still, always consider it carefully with your daily cash flow.

Customer Support and Merchant Assistance

American Express offers dedicated merchant support for account management, disputes, and technical questions. Support channels typically include phone, online resources, and documentation portals. Merchant assistance tends to be structured and policy-driven, reflecting the company’s scale and regulatory obligations. While this ensures consistency, it may feel less flexible for smaller businesses. Dispute resolution support is particularly structured, helping merchants understand timelines and documentation requirements clearly. Educational resources are available, though they focus more on compliance and procedures than marketing guidance. Overall, support quality is dependable, though not always personalized in the way smaller processors might offer.

International Acceptance and Global Reach

American Express has strong international recognition, though acceptance varies by region. Businesses operating in tourist-heavy or international markets often benefit from offering Amex as a payment option. Cross-border transactions may involve currency conversion and additional fees, which merchants should review carefully.

For global enterprises, Amex’s consistent policies can simplify international payment acceptance across locations. Smaller businesses should evaluate whether international customers represent a meaningful portion of sales before prioritizing acceptance. Global reach is a strength, but demand depends heavily on customer demographics.

Strengths and Limitations of American Express Payment Solutions

American Express payment solutions offer strong brand recognition, reliable security, and access to a valuable customer segment. For businesses aligned with its cardholder base, acceptance can enhance customer satisfaction and transaction value. However, higher processing costs, separate settlement processes, and administrative complexity may limit appeal for some businesses. The platform works best as a strategic addition rather than a default requirement. Merchants who assess fit carefully are more likely to benefit. American Express is not a universal solution, but in the right context, it remains a meaningful payment option.

FAQs

Is American Express Payment Solutions suitable for small businesses?

It can be suitable if a small business serves customers who actively use Amex cards and has margins that can absorb higher processing costs.

Does accepting American Express increase revenue potential?

In some cases, yes, as Amex cardholders may spend more per transaction, but this depends on customer profile and business type.

How does American Express compare to other payment processors?

American Express focuses on card brand acceptance rather than acting as a full-service processor, making it best used alongside existing payment solutions rather than as a replacement.

Best Product & Services

Recent Posts