QuickPay Review

26

Oct 2025

No Comments

QuickPay Review

QuickPay is a payment gateway solution designed to simplify online transactions for businesses of all sizes. Based in Denmark, it enables merchants to accept payments via cards, wallets, and alternative methods through a single, unified platform. In an era where digital payments dominate global commerce, QuickPay positions itself as a flexible, developer-friendly system that connects businesses to multiple acquirers and payment methods without the complexity of managing separate integrations. Lets read more about QuickPay Review.

The platform has steadily gained recognition across Europe for its transparent approach, wide integration capabilities, and modern API structure. Whether a merchant operates a small online store or a large SaaS business, QuickPay aims to streamline payment acceptance while offering a balance between reliability, affordability, and usability.

History & Background | QuickPay Review

QuickPay was founded in 2004 in Aarhus, Denmark, when e-commerce in Northern Europe was booming. The founders wanted to create a gateway that would make it easy for small and medium sized businesses to handle online payments securely and efficiently. Over the years QuickPay became a well established player in the Nordic payment landscape, working with major acquirers such as Nets, Klarna and Swedbank.

In 2016 QuickPay merged with Clearhaus, a licensed acquirer, creating a strong ecosystem that allowed the company to offer both gateway and acquiring services. This integration gave customers a seamless setup, combining the technical flexibility of QuickPay with the regulatory stability of Clearhaus. Today QuickPay has more than 30,000 merchants and processes millions of transactions every month in multiple currencies and payment types.

QuickPay has a reputation for transparency, especially within the EU regulatory framework, where it complies with PSD2 and PCI-DSS. Its focus on developer centric design and uptime has made it a popular choice for many Scandinavian businesses looking for a lean and flexible payment solution.

Core Features & Functionalities

QuickPay’s core appeal lies in its wide feature set, designed to meet the needs of online stores, subscription businesses, and marketplaces. It supports major payment types, including Visa, Mastercard, MobilePay, PayPal, Apple Pay, Google Pay, and Klarna. Merchants can also accept bank transfers, invoices, and local payment schemes specific to Nordic markets.

Recurring payments are one of QuickPay’s standout features, allowing businesses to automate billing for subscriptions or memberships without re-entering customer details. The invoicing and refund tools simplify day-to-day financial operations. In addition, QuickPay’s API provides developers with full access to integrate payment functions into custom applications or third-party systems.

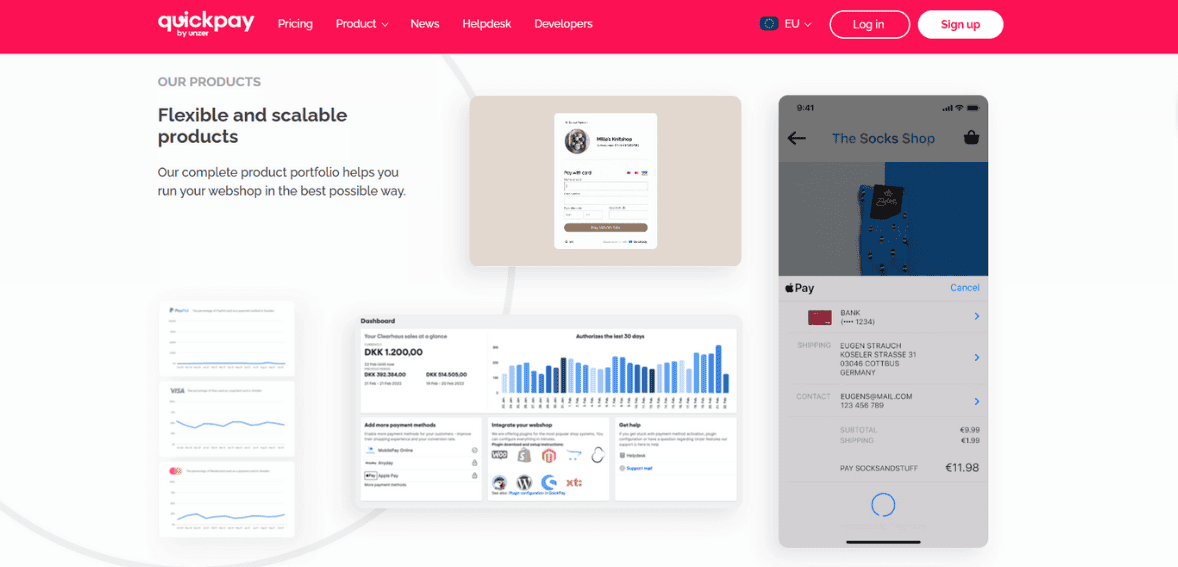

Another major advantage is its wide range of plug-and-play integrations. QuickPay offers ready-made modules for Shopify, WooCommerce, Magento, PrestaShop, and other popular e-commerce platforms. The dashboard provides a unified view of transactions, settlements, and refunds, helping businesses track payment data effortlessly. These features collectively create a robust foundation for managing digital transactions while minimizing operational friction.

Ease of Integration & Onboarding

QuickPay is well known for its developer-friendly environment and clear documentation. The onboarding process is generally smooth, especially for merchants using major e-commerce platforms with existing QuickPay plugins. Most integrations can be completed within hours, thanks to pre-built modules that eliminate the need for complex coding.

For custom integrations, QuickPay’s RESTful API offers extensive flexibility. It supports multiple programming languages, and the documentation provides practical examples that make implementation straightforward even for smaller teams. Testing can be conducted in a sandbox environment before going live, which reduces the likelihood of errors during launch.

New merchants typically appreciate the simplicity of QuickPay’s dashboard setup, where they can configure payment methods, enable recurring billing, and monitor transactions from one interface. However, businesses without technical staff may find the deeper customization options slightly overwhelming. Overall, QuickPay strikes a good balance between simplicity and control, allowing both novice and experienced users to adapt the platform to their needs without extensive training or support.

User Interface & Usability

QuickPay’s user interface is clean, modern, and focused on functionality. The dashboard presents an at-a-glance summary of recent transactions, pending payments, and settlements. Navigation is intuitive, with clear menus for invoices, refunds, and reports. Users can also apply filters to review specific transaction types or export data in common formats for accounting use.

One area where QuickPay excels is its merchant portal, which centralizes multiple operational tasks into a single screen. Users can generate payment links, view analytics, or update payment settings without toggling between modules. For customers, the checkout flow is optimized for clarity and speed, minimizing the number of steps required to complete a payment.

Mobile responsiveness is also strong; although QuickPay doesn’t offer a dedicated app, the web dashboard works well across devices. Some users, however, have expressed a desire for more advanced visual analytics and customizable reports. Despite this, the system’s overall usability makes it efficient for daily operations, providing merchants with the transparency needed to manage payments confidently.

Reliability, Performance & Uptime

Reliability is key in payment processing and QuickPay delivers on that front. The platform has high uptime, over 99.9% with infrastructure in secure data centers with redundant systems. Payments are fast, once customer authentication is verified, most are done in seconds.

It can handle large volumes of transactions, which is important for businesses with seasonal spikes or flash sales. It has real time monitoring to detect and fix issues before they affect users. Downtime is rare and when it does happen it’s usually fixed quickly and updates are posted on QuickPay’s status page.

That being said some users have reported minor delays when reconciling transactions or updating settlement reports especially during high volume periods. Not a major flaw but can be an issue for merchants who need instant updates for bookkeeping. Overall QuickPay’s reliability is one of its strongest suits, giving merchants peace of mind for transaction continuity.

Fees, Pricing & Cost Structure

It operates on a transparent pricing model, separating gateway fees from acquiring fees. The basic plan usually includes a small monthly fee for access to the gateway, plus a per-transaction fee that varies based on payment method and volume. Merchants who process payments through Clearhaus, its partner acquirer, may benefit from bundled pricing that reduces overall cost.

There are no setup fees, and merchants can cancel without long-term contracts, which is appealing for startups. However, additional costs may apply for premium features like recurring billing or advanced fraud filters. While QuickPay’s rates are competitive in the European market, some businesses find it slightly more expensive than newer fintech solutions that operate on flat-rate models.

Overall, QuickPay balances flexibility with transparency; though merchants must read the fine print to fully understand costs related to currency conversion or refunds. Larger merchants can negotiate better rates, but for smaller businesses, the total expense may depend heavily on transaction volume and selected payment methods.

Security, Compliance & Trustworthiness

Security is one of QuickPay’s strengths. The platform is PCI-DSS Level 1 compliant, so payment data is encrypted and tokenized throughout the transaction process. It also supports 3D Secure 2.0 for cardholder authentication, in line with the EU’s PSD2 directive for strong customer authentication. QuickPay uses TLS encryption for data transmission and has fraud monitoring tools to detect suspicious behavior before it becomes a chargeback or loss. Merchants can configure risk management settings to block high risk transactions or set country specific restrictions.

As for reputation, it is generally seen as a trusted and compliant operator within the European Economic Area. The partnership with Clearhaus adds to that, as Clearhaus is regulated by the Danish Financial Supervisory Authority. A few reviews have mentioned limited global regulatory oversight outside the EU, but within Europe QuickPay is seen as a secure and reliable processor.

Customer Support & Service Quality

QuickPay has multiple support channels including email, live chat and a knowledge base. The documentation and FAQs are well organized and often resolve technical issues without human intervention. For more complex issues merchants can contact support directly and typically get a response within 1 business day.

Customer feedback on support is mixed but leans positive. Many users praise the professionalism and patience of the QuickPay team especially during integration or settlement issues. Others have reported slower responses during high volume periods or account specific issues. A big plus is QuickPay’s open communication style; they have an active status page and keep users informed of maintenance schedules or performance issues. This level of transparency has earned trust even when things go wrong. Not perfect but QuickPay’s support is trying to be responsive and clear.

Strengths & Advantages

QuickPay’s biggest strength lies in its balance between flexibility and reliability. It provides a rich set of payment options, strong developer tools, and easy integration with leading e-commerce platforms. For European merchants, especially those operating in Denmark, Sweden, and Germany, it offers local payment compatibility that global providers often lack.

Another significant advantage is its transparent documentation and open API, which give developers full control over the integration process. Its consistent uptime and high transaction success rate make it dependable for businesses with continuous online sales. The partnership with Clearhaus simplifies merchant onboarding and settlements by connecting gateway and acquiring services under one umbrella.

Finally, QuickPay’s pricing model is transparent, and its fraud prevention features are robust. The overall user experience is smooth, with a focus on functionality over flash. These combined strengths make it a solid, dependable payment gateway for growing businesses seeking simplicity without sacrificing control or compliance.

Weaknesses, Limitations & Criticisms

It’s not all good though. One of the biggest criticisms is that QuickPay is not very international. It supports international payments but its infrastructure and acquirer partners are EU based so it’s not ideal for merchants with operations in North America or Asia. Some users also find the reporting tools basic compared to the bigger guys. No mobile app means you can’t monitor in real time on the go. The API is powerful but non technical users will struggle to use it without external help.

Another point of contention is pricing. It is upfront with costs but the combination of gateway and acquirer fees can be confusing for new merchants. A few Trustpilot reviews mention delayed settlements or unclear refund timelines but these seem to be isolated. These aren’t deal breakers but show where the platform could evolve to stay competitive in a rapidly changing payments landscape.

Comparative Landscape & Alternatives

In the global payment gateway market, QuickPay competes with providers like Stripe, Adyen, PayPal, and Mollie. While QuickPay focuses primarily on the European SME segment, competitors such as Stripe and Adyen target broader global audiences with more advanced analytics and enterprise-grade solutions.

QuickPay’s advantage lies in its simplicity and regional optimization; it supports local payment methods like MobilePay and Dankort, which are essential for Scandinavian customers. However, for merchants with multi-regional operations or complex subscription models, platforms like Stripe may offer more scalability.

Mollie serves as QuickPay’s closest competitor in terms of target market and pricing structure, while PayPal remains the easiest entry-level solution for small businesses. Ultimately, QuickPay fills an important niche: it’s not the largest or most feature-heavy, but for businesses focused on reliability, compliance, and ease of setup within Europe, it stands out as a strong contender.

Recommended Use Cases & Ideal Scenarios

QuickPay is best suited for small and medium-sized businesses, particularly those in Europe that require local payment support and straightforward integration. E-commerce stores, subscription platforms, and service providers can benefit from its recurring billing, invoice management, and API customization capabilities.

Startups with limited IT resources can rely on its pre-built modules for quick deployment, while more advanced companies can use the API to develop tailored payment solutions. Merchants that value transparency, uptime, and compliance over elaborate analytics will find QuickPay’s design appealing.

However, it may not be ideal for enterprises needing global reach or deep reporting functionality. In such cases, pairing QuickPay with third-party analytics tools or considering hybrid setups with other processors might deliver better outcomes. For its core audience, though, QuickPay remains an efficient, secure, and cost-effective choice that aligns with practical business realities.

Conclusion & Overall Assessment

QuickPay successfully blends simplicity with technical robustness. It offers an extensive feature set, strong compliance standards, and a developer-friendly environment that makes it easy to adapt to diverse business needs. For European merchants, its integration with local acquirers and support for regional payment methods give it a clear competitive edge.

While it doesn’t match the global scale of giants like Stripe or Adyen, its focused approach delivers reliability and affordability without unnecessary complexity. Its limitations; such as basic analytics and limited global expansion; are outweighed by its consistent performance, transparent pricing, and user-oriented design.

Overall, QuickPay stands as a dependable and well-rounded payment gateway that balances flexibility, security, and value. Businesses seeking a stable, regulation-compliant, and easily deployable solution will find it a practical choice for managing online payments efficiently.

FAQs

Is QuickPay safe to use for processing payments?

Yes. QuickPay adheres to PCI-DSS Level 1 standards, employs encryption and tokenization, and follows PSD2 regulations for strong customer authentication. Its security record is strong, with additional fraud detection tools to safeguard merchants and customers alike.

Who is QuickPay best suited for?

QuickPay works best for small and medium-sized European businesses that need a reliable and compliant payment gateway. It’s ideal for e-commerce retailers, SaaS platforms, and service providers operating in Denmark, Sweden, or neighboring markets.

How does QuickPay’s pricing compare to competitors?

QuickPay’s pricing is competitive for European users but may not always be the cheapest. It separates gateway and acquiring fees, which adds flexibility but can confuse first-time users. Larger merchants often negotiate better rates depending on transaction volumes and payment methods.

Best Product & Services

Recent Posts